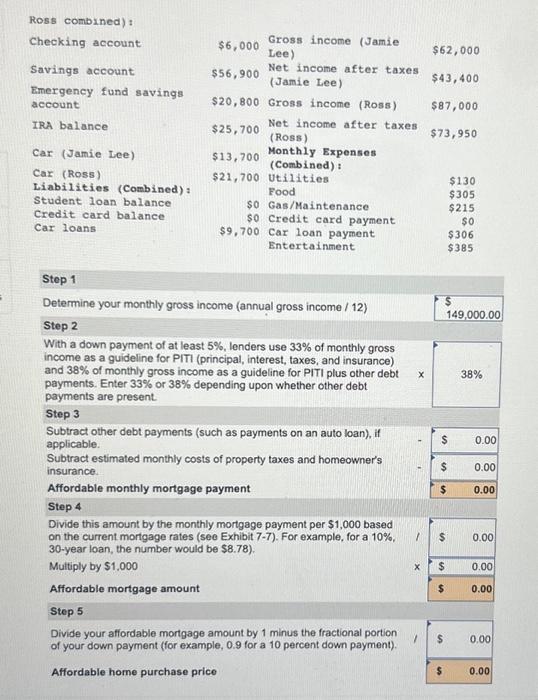

Ross combined) : Checking account Savings account Emergency fund savings account Car (Jamie Lee) Car (Ross) Liabilities (Combined) : Student loan balance Credit card balance Car loans $6,000Grossincome(JamieLee)62,000 $56,900Netincomeaftertaxes$43,400(JamieLee) $20,800 Gross income (Ross) $87,000 $25,700Netincomeaftertaxes$73,950(Ross) $13,700 Monthly Expenses (Combined): $21,700$0$0$9,700UtilitiesFoodGas/MaintenanceCreditcardpaymentCarloanpaymentEntertainment$130$305$215$0$306$385 Step 1 Determine your monthly gross income (annual gross income / 12) Step 2 With a down payment of at least 5%, lenders use 33% of monthly gross income as a guideline for PITI (principal, interest, taxes, and insurance) and 38% of monthly gross income as a guideline for PITI plus other debt payments. Enter 33% or 38% depending upon whether other debt payments are present. Step 3 Subtract other debt payments (such as payments on an auto loan), if applicable. Subtract estimated monthly costs of property taxes and homeowner's insurance. Affordable monthly mortgage payment Step 4 Divide this amount by the monthly mortgage payment per $1,000 based on the current mortgage rates (see Exhibit 7-7). For example, for a 10%, 30 -year loan, the number would be $8.78 ). Multiply by $1,000 Affordable mortgage amount Step 5 Divide your affordable mortgage amount by 1 minus the fractional portion of your down payment (for example, 0.9 for a 10 percent down payment). Affordable home purchase price Ross combined) : Checking account Savings account Emergency fund savings account Car (Jamie Lee) Car (Ross) Liabilities (Combined) : Student loan balance Credit card balance Car loans $6,000Grossincome(JamieLee)62,000 $56,900Netincomeaftertaxes$43,400(JamieLee) $20,800 Gross income (Ross) $87,000 $25,700Netincomeaftertaxes$73,950(Ross) $13,700 Monthly Expenses (Combined): $21,700$0$0$9,700UtilitiesFoodGas/MaintenanceCreditcardpaymentCarloanpaymentEntertainment$130$305$215$0$306$385 Step 1 Determine your monthly gross income (annual gross income / 12) Step 2 With a down payment of at least 5%, lenders use 33% of monthly gross income as a guideline for PITI (principal, interest, taxes, and insurance) and 38% of monthly gross income as a guideline for PITI plus other debt payments. Enter 33% or 38% depending upon whether other debt payments are present. Step 3 Subtract other debt payments (such as payments on an auto loan), if applicable. Subtract estimated monthly costs of property taxes and homeowner's insurance. Affordable monthly mortgage payment Step 4 Divide this amount by the monthly mortgage payment per $1,000 based on the current mortgage rates (see Exhibit 7-7). For example, for a 10%, 30 -year loan, the number would be $8.78 ). Multiply by $1,000 Affordable mortgage amount Step 5 Divide your affordable mortgage amount by 1 minus the fractional portion of your down payment (for example, 0.9 for a 10 percent down payment). Affordable home purchase price