Answered step by step

Verified Expert Solution

Question

1 Approved Answer

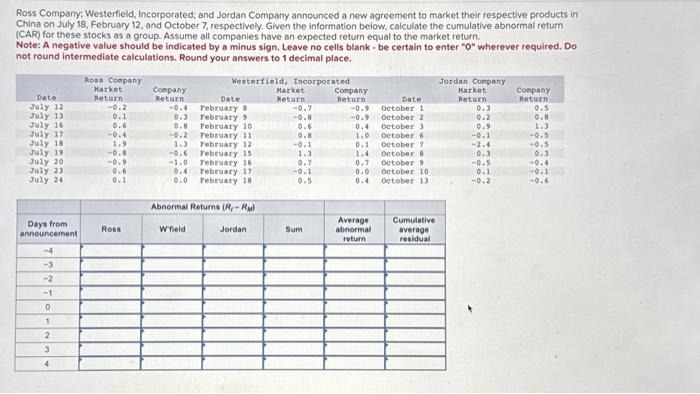

Ross Company, Westerfield, Incorporated; and Jordan Company announced a new agreement to market their respective products in China on July 1 8 , February 1

Ross Company, Westerfield, Incorporated; and Jordan Company announced a new agreement to market their respective products in China on July February and October respectively. Given the information below, calculate the cumulative abnormal return CAR for these stocks as a group. Assume all companies have an expected return equal to the market return. Note: A negative value should be indicated by a minus sign. Leave no cells blank be certain to enter wherever required. Do not round intermediate calculations. Round your answers to decimal place. Westerfield, Incorporated Date July July July July July July July July July Days from announcement Ross Company Market Return Ross Company Return Date February February February rebruary February February February February rebruary Abnormal Returns RRM Jordan W'field Market Return Sum Company Return Average abnormal return Date October October October October October October October October October Cumulative average residual Jordan Company Market Return Company Return

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Finance Discussion Papers The Information Content Of High Frequency Data For Estimating Equity Return Models And Forecasting Risk

Authors: United States Federal Reserve Board, Dobrislav P. Dobrev, Pawel J. Szerszen

1st Edition

1288724810, 9781288724819