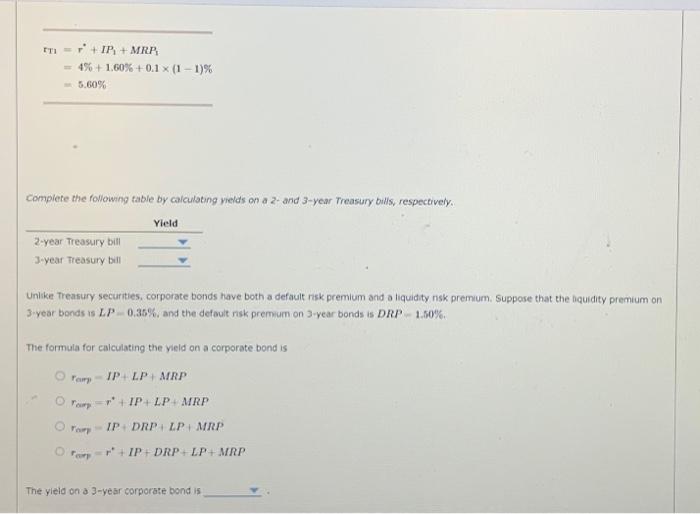

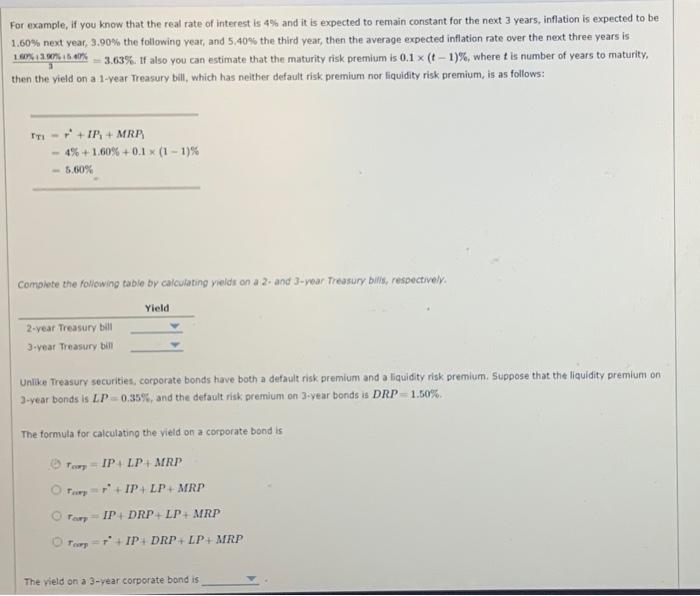

rT1=r+MP1+MRP1=4%+1.60%+0.1(11)%=5.60% Complete the following table by calculating yelds on a 2-and 3-year Treasury bulls, respectively. Unike Treasury securities, corporate bonds have both a default nsk premium and a liquidity nsk premum. Suppose that the hquidity premium on 3 year bonds is L.P=0.35%, and the defoult nsk premum on 3 -year bonds is DRP1.50%. The formula for calculating the vield on a corporate bond is ramp=IP+LP+MRPrain=r+IP+LP+MRProur=IP+DRP+LP+MRProur=r+IP+DRP+LP+MRP The yield on a 3-year corporate bond is rT1=r+MP1+MRP1=4%+1.60%+0.1(11)%=5.60% Complete the following table by calculating yelds on a 2-and 3-year Treasury bulls, respectively. Unike Treasury securities, corporate bonds have both a default nsk premium and a liquidity nsk premum. Suppose that the hquidity premium on 3 year bonds is L.P=0.35%, and the defoult nsk premum on 3 -year bonds is DRP1.50%. The formula for calculating the vield on a corporate bond is ramp=IP+LP+MRPrain=r+IP+LP+MRProur=IP+DRP+LP+MRProur=r+IP+DRP+LP+MRP The yield on a 3-year corporate bond is For example, if you know that the real rate of interest is 4% and it is expected to remain constant for the next 3 years, inflation is expected to be 1.60% next vear, 3.90% the following vear, and 5.40% the third year, then the average expected inflation nate over the next three years is 31.0513.90.5.40=3.63%. If also you can estimate that the maturity risk premium is 0.1(t1)%, where t is number of years to maturity, then the yield on a 1-vear Treasury bill, which has neither default risk premium nor liquidity risk premium, is as follows: rTI=r+IP1+MRP=4%+1.60%+0.1(11)%=5.60% Complete the following table by calculating vields on a 2- and 3-yoar Treasury bulis, respectively. Unlike Treasury securities, corporate bonds have both a default risk premium and a liquidity risk premium. Suppose that the liquidity premium on 3-year bonds is LP=0.35%, and the default risk premium on 3 -year bonds is DRP=1.50%. The formula for calculating the vield on a corporate bond is ron=IP+LP+MRPron=r+IP+LP+MRProry=IP+DRP+LP+MRPror=r+IP+DRP+LP+MRP The vield on a 3 -vear corporate bond is rT1=r+MP1+MRP1=4%+1.60%+0.1(11)%=5.60% Complete the following table by calculating yelds on a 2-and 3-year Treasury bulls, respectively. Unike Treasury securities, corporate bonds have both a default nsk premium and a liquidity nsk premum. Suppose that the hquidity premium on 3 year bonds is L.P=0.35%, and the defoult nsk premum on 3 -year bonds is DRP1.50%. The formula for calculating the vield on a corporate bond is ramp=IP+LP+MRPrain=r+IP+LP+MRProur=IP+DRP+LP+MRProur=r+IP+DRP+LP+MRP The yield on a 3-year corporate bond is rT1=r+MP1+MRP1=4%+1.60%+0.1(11)%=5.60% Complete the following table by calculating yelds on a 2-and 3-year Treasury bulls, respectively. Unike Treasury securities, corporate bonds have both a default nsk premium and a liquidity nsk premum. Suppose that the hquidity premium on 3 year bonds is L.P=0.35%, and the defoult nsk premum on 3 -year bonds is DRP1.50%. The formula for calculating the vield on a corporate bond is ramp=IP+LP+MRPrain=r+IP+LP+MRProur=IP+DRP+LP+MRProur=r+IP+DRP+LP+MRP The yield on a 3-year corporate bond is For example, if you know that the real rate of interest is 4% and it is expected to remain constant for the next 3 years, inflation is expected to be 1.60% next vear, 3.90% the following vear, and 5.40% the third year, then the average expected inflation nate over the next three years is 31.0513.90.5.40=3.63%. If also you can estimate that the maturity risk premium is 0.1(t1)%, where t is number of years to maturity, then the yield on a 1-vear Treasury bill, which has neither default risk premium nor liquidity risk premium, is as follows: rTI=r+IP1+MRP=4%+1.60%+0.1(11)%=5.60% Complete the following table by calculating vields on a 2- and 3-yoar Treasury bulis, respectively. Unlike Treasury securities, corporate bonds have both a default risk premium and a liquidity risk premium. Suppose that the liquidity premium on 3-year bonds is LP=0.35%, and the default risk premium on 3 -year bonds is DRP=1.50%. The formula for calculating the vield on a corporate bond is ron=IP+LP+MRPron=r+IP+LP+MRProry=IP+DRP+LP+MRPror=r+IP+DRP+LP+MRP The vield on a 3 -vear corporate bond is