Answered step by step

Verified Expert Solution

Question

1 Approved Answer

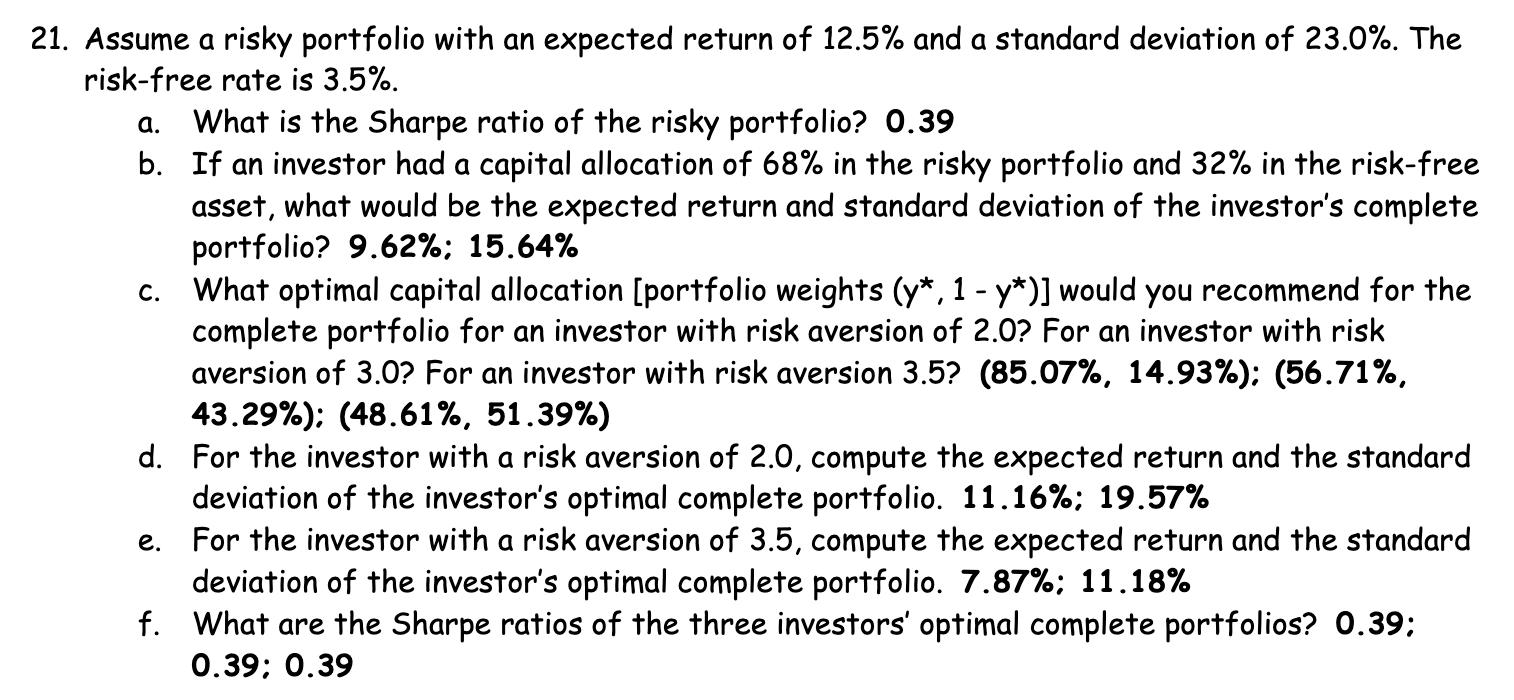

21. Assume a risky portfolio with an expected return of 12.5% and a standard deviation of 23.0%. The risk-free rate is 3.5%. a. What

21. Assume a risky portfolio with an expected return of 12.5% and a standard deviation of 23.0%. The risk-free rate is 3.5%. a. What is the Sharpe ratio of the risky portfolio? 0.39 b. If an investor had a capital allocation of 68% in the risky portfolio and 32% in the risk-free asset, what would be the expected return and standard deviation of the investor's complete portfolio? 9.62%; 15.64% What optimal capital allocation [portfolio weights (y*, 1 - y*)] would you recommend for the complete portfolio for an investor with risk aversion of 2.0? For an investor with risk aversion of 3.0? For an investor with risk aversion 3.5? (85.07%, 14.93%); (56.71%, 43.29%); (48.61%, 51.39%) d. For the investor with a risk aversion of 2.0, compute the expected return and the standard deviation of the investor's optimal complete portfolio. 11.16%; 19.57% e. For the investor with a risk aversion of 3.5, compute the expected return and the standard deviation of the investor's optimal complete portfolio. 7.87%; 11.18% f. What are the Sharpe ratios of the three investors' optimal complete portfolios? 0.39; 0.39; 0.39 C.

Step by Step Solution

★★★★★

3.46 Rating (159 Votes )

There are 3 Steps involved in it

Step: 1

A risky portfolio is a combination of risky assets in their respective proportions a Shar...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Andersons Business Law and the Legal Environment

Authors: David p. twomey, Marianne moody Jennings

21st Edition

1111400547, 324786662, 978-1111400545, 978-0324786668