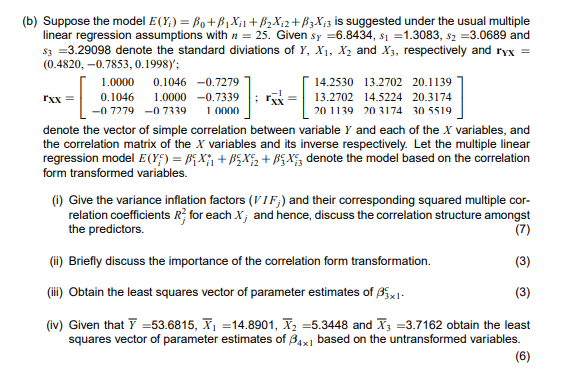

rxx = (b) Suppose the model E(Y) = Bo+B,X1 +B2X2+B3X:3 is suggested under the usual multiple linear regression assumptions with n = 25. Given sy =6.8434, s =1.3083, $2 =3.0689 and $3 =3.29098 denote the standard diviations of Y, X1, X, and X3, respectively and ryx = (0.4820, -0.7853, 0.1998): 1.0000 0.1046 -0.7279 14.2530 13.2702 20.1139 0.1046 1.0000 -0.7339 13.2702 14.5224 20.3174 -0 7279 -0 7339 1 0000 20.1139 203174 30 5519 denote the vector of simple correlation between variable Y and each of the X variables, and the correlation matrix of the X variables and its inverse respectively. Let the multiple linear regression model E(Y) = BFX: +BX$ + BEX denote the model based on the correlation form transformed variables. ) Give the variance inflation factors (VIF;) and their corresponding squared multiple cor- relation coefficients for each X; and hence, discuss the correlation structure amongst the predictors. (7) (i) Briefly discuss the importance of the correlation form transformation. (3) (ii) obtain the least squares vector of parameter estimates of Bixi- (3) (iv) Given that 7 =53.6815, 71 = 14.8901, X2=5.3448 and X3 = 3.7162 obtain the least squares vector of parameter estimates of B4x1 based on the untransformed variables. (6) rxx = (b) Suppose the model E(Y) = Bo+B,X1 +B2X2+B3X:3 is suggested under the usual multiple linear regression assumptions with n = 25. Given sy =6.8434, s =1.3083, $2 =3.0689 and $3 =3.29098 denote the standard diviations of Y, X1, X, and X3, respectively and ryx = (0.4820, -0.7853, 0.1998): 1.0000 0.1046 -0.7279 14.2530 13.2702 20.1139 0.1046 1.0000 -0.7339 13.2702 14.5224 20.3174 -0 7279 -0 7339 1 0000 20.1139 203174 30 5519 denote the vector of simple correlation between variable Y and each of the X variables, and the correlation matrix of the X variables and its inverse respectively. Let the multiple linear regression model E(Y) = BFX: +BX$ + BEX denote the model based on the correlation form transformed variables. ) Give the variance inflation factors (VIF;) and their corresponding squared multiple cor- relation coefficients for each X; and hence, discuss the correlation structure amongst the predictors. (7) (i) Briefly discuss the importance of the correlation form transformation. (3) (ii) obtain the least squares vector of parameter estimates of Bixi- (3) (iv) Given that 7 =53.6815, 71 = 14.8901, X2=5.3448 and X3 = 3.7162 obtain the least squares vector of parameter estimates of B4x1 based on the untransformed variables. (6)