Question

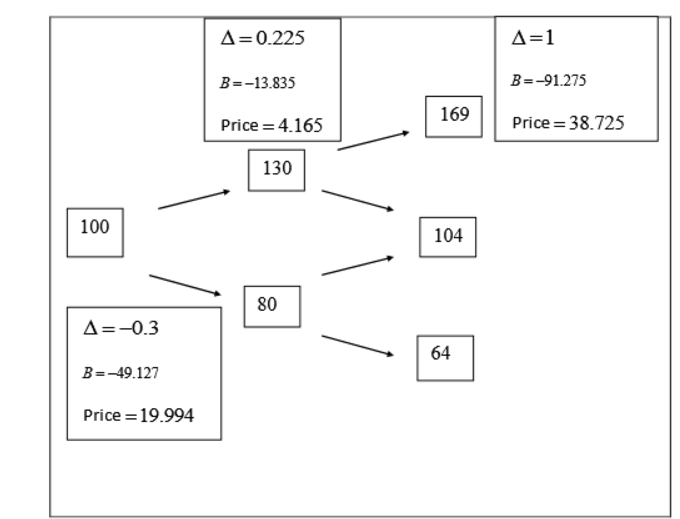

S=$100, K=$95, Standard deviation=30%, r=8%, T=1, Dividen yield=0, u=1.3, d=0.8 and n=2 Construct the binomial tree for a call option. At each node provide the

S=$100, K=$95, Standard deviation=30%, r=8%, T=1, Dividen yield=0, u=1.3, d=0.8 and n=2

Construct the binomial tree for a call option. At each node provide the premium, Delta and B.

(I calculated the rest but unbale to get the Delta= -03, B= -49.127 and price=19.994)

Please give me a full step by step working for Delta= -0.3, B= -49.127 and price=19.994

The tree has the answers, but i need detailed workings with formuals.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Analysis for Financial Management

Authors: Robert Higgins

11th edition

77861787, 978-0077861780