Answered step by step

Verified Expert Solution

Question

1 Approved Answer

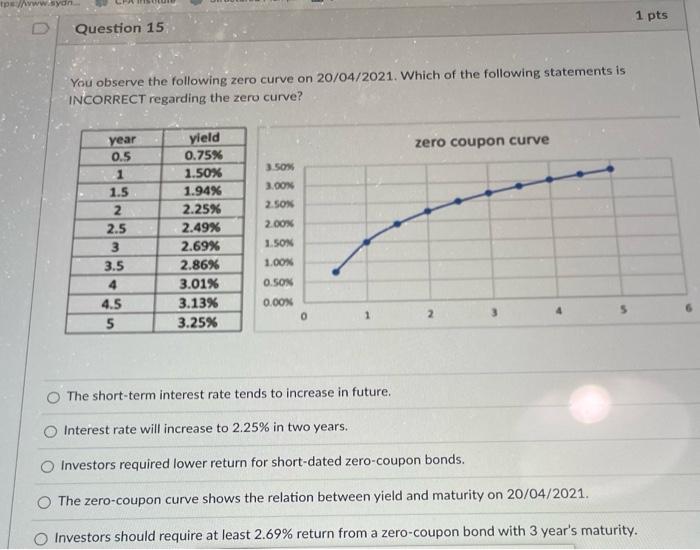

s15 pe/www.sydn 1 pts Question 15 You observe the following zero curve on 20/04/2021. Which of the following statements is INCORRECT regarding the zero curve?

s15

pe/www.sydn 1 pts Question 15 You observe the following zero curve on 20/04/2021. Which of the following statements is INCORRECT regarding the zero curve? zero coupon curve 3.50 3.00 2.SON 2.00% year 0.5 1 1.5 2 2.5 3 3.5 4 4.5 5 yield 0.75% 1.50% 1.94% 2.25% 2.49% 2.69% 2.86% 3.01% 3.13% 3.25% 1.SON 1.00 0.50% 0.00% 0 1 2 3 The short-term interest rate tends to increase in future. Interest rate will increase to 2.25% in two years. Investors required lower return for short-dated zero-coupon bonds. The zero-coupon curve shows the relation between yield and maturity on 20/04/2021. Investors should require at least 2.69% return from a zero-coupon bond with 3 year's maturity Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Legal Environment Today Summarized Case Edition

Authors: Roger LeRoy Miller

8th Edition

130526276X, 978-1305279407, 1305279409, 978-1305704930, 1305704932, 978-1305262768