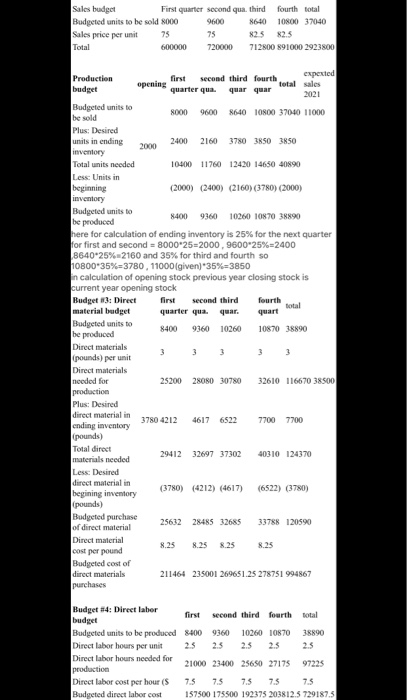

Sales budget First quarter second qua third fourth total Budgeted units to be sold 8000 9600 8640 10800 37040 Sales price per unit 75 75 825 82.5 Total 600000 720000 712800 891000 2923800 Production first second third fourth experted budget opening quarter 44 4. quar quar total sales 2021 Budgeted units to 8000 be sold 9600 8640 10800 37040 11000 Plus: Desired units in ending 2000 2400 2160 3780 3850 3850 inventory Total units needed 10400 11760 12420 14650 40890 Less: Units in beginning (2000) (2400) (2160)(3780) (2000) inventory Budgeted units to 8400 9360 10260 10870 38890 be produced here for calculation of ending inventory is 25% for the next quarter for first and second = 8000'25=2000, 9600-25%=2400 8640-25% 2160 and 35% for third and fourth so 10800-35%=3780, 11000 (given)*35%=3850 in calculation of opening stock previous year closing stock is current year opening stock Budget #3: Direct first second third fourth material budget quarter quaquar. quart Budgeted units to 8400 he produced 9360 10260 10870 38890 Direct materials (pounds) per unit Direct materials needed for 25200 28080 30780 32610 116670 38500 production Plus: Desired direct material in 3780 4212 4617 6522 cnding inventory 7700 7700 (pounds) Total direct materials needed 2941232697 37302 40310 124370 Less: Desired direct material in (3780) (4212) (4617) begining inventory (6522) (3780) pounds) Budgeted purchase 25632 28485 32685 of direct material 33788 120590 Direct material 8.25 8.25 8.25 8.25 cost per pound Budgeted cost of direct materials 211464 235001 269651.25 278751 994867 purchases Budget #4: Direct laber first second third fourth total budget Budgeted units to be produced 8400 9360 10260 10870 38890 Direct labor hours per unit 25 2.5 2.5 2.5 Direct labor hours needed for 21000 23400 25650 27175 production 97225 Direct labor cost per hour (S 7.5 7.5 7.5 7.5 7.5 Budgeted direct labor cost 157500 175500 192375 203812.5 729187.5 Sales budget First quarter second qua third fourth total Budgeted units to be sold 8000 9600 8640 10800 37040 Sales price per unit 75 75 825 82.5 Total 600000 720000 712800 891000 2923800 Production first second third fourth experted budget opening quarter 44 4. quar quar total sales 2021 Budgeted units to 8000 be sold 9600 8640 10800 37040 11000 Plus: Desired units in ending 2000 2400 2160 3780 3850 3850 inventory Total units needed 10400 11760 12420 14650 40890 Less: Units in beginning (2000) (2400) (2160)(3780) (2000) inventory Budgeted units to 8400 9360 10260 10870 38890 be produced here for calculation of ending inventory is 25% for the next quarter for first and second = 8000'25=2000, 9600-25%=2400 8640-25% 2160 and 35% for third and fourth so 10800-35%=3780, 11000 (given)*35%=3850 in calculation of opening stock previous year closing stock is current year opening stock Budget #3: Direct first second third fourth material budget quarter quaquar. quart Budgeted units to 8400 he produced 9360 10260 10870 38890 Direct materials (pounds) per unit Direct materials needed for 25200 28080 30780 32610 116670 38500 production Plus: Desired direct material in 3780 4212 4617 6522 cnding inventory 7700 7700 (pounds) Total direct materials needed 2941232697 37302 40310 124370 Less: Desired direct material in (3780) (4212) (4617) begining inventory (6522) (3780) pounds) Budgeted purchase 25632 28485 32685 of direct material 33788 120590 Direct material 8.25 8.25 8.25 8.25 cost per pound Budgeted cost of direct materials 211464 235001 269651.25 278751 994867 purchases Budget #4: Direct laber first second third fourth total budget Budgeted units to be produced 8400 9360 10260 10870 38890 Direct labor hours per unit 25 2.5 2.5 2.5 Direct labor hours needed for 21000 23400 25650 27175 production 97225 Direct labor cost per hour (S 7.5 7.5 7.5 7.5 7.5 Budgeted direct labor cost 157500 175500 192375 203812.5 729187.5