Answered step by step

Verified Expert Solution

Question

1 Approved Answer

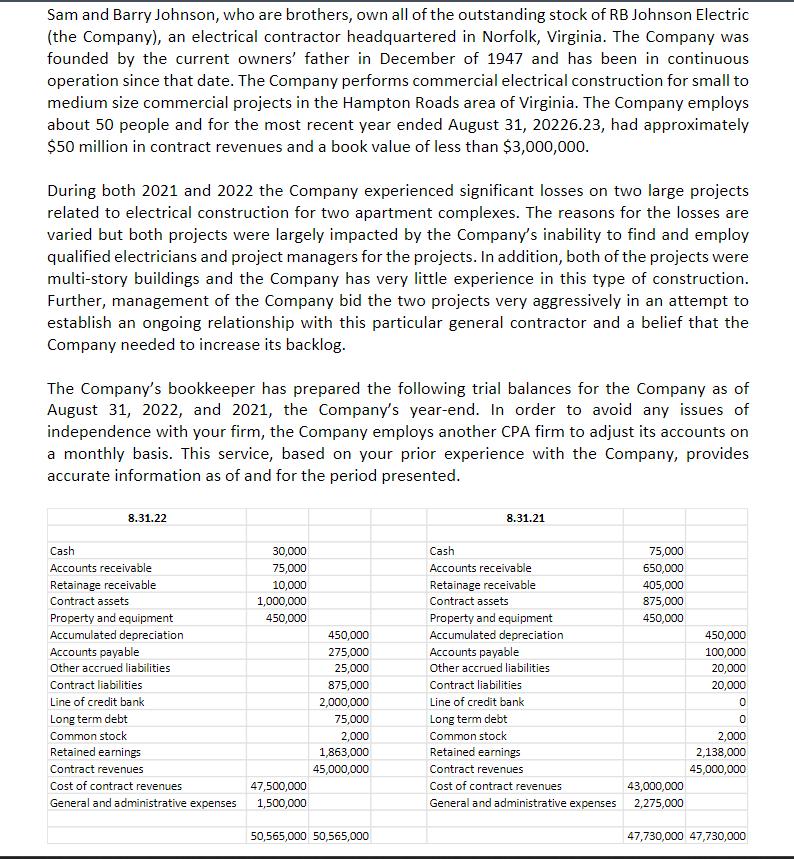

Sam and Barry Johnson, who are brothers, own all of the outstanding stock of RB Johnson Electric (the Company), an electrical contractor headquartered in

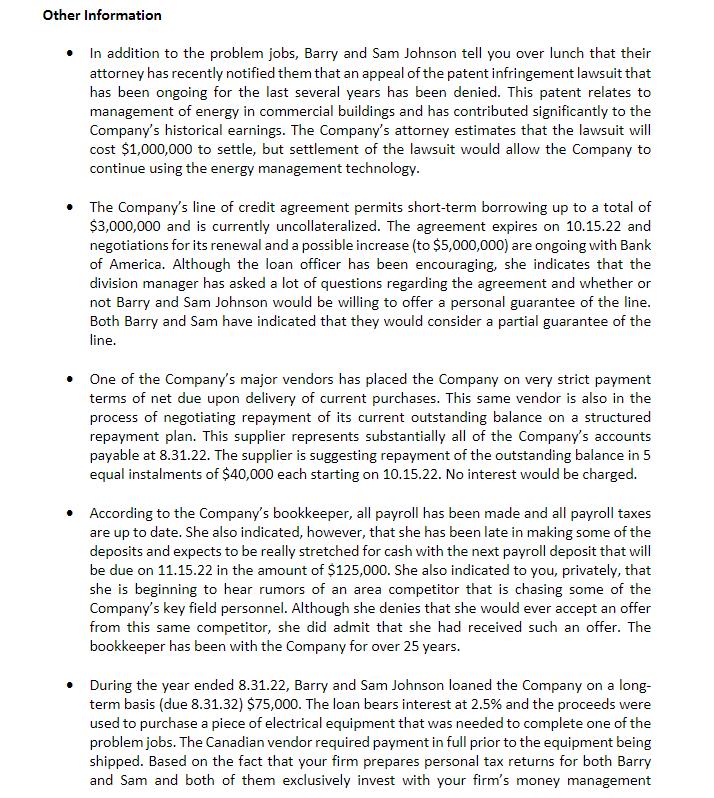

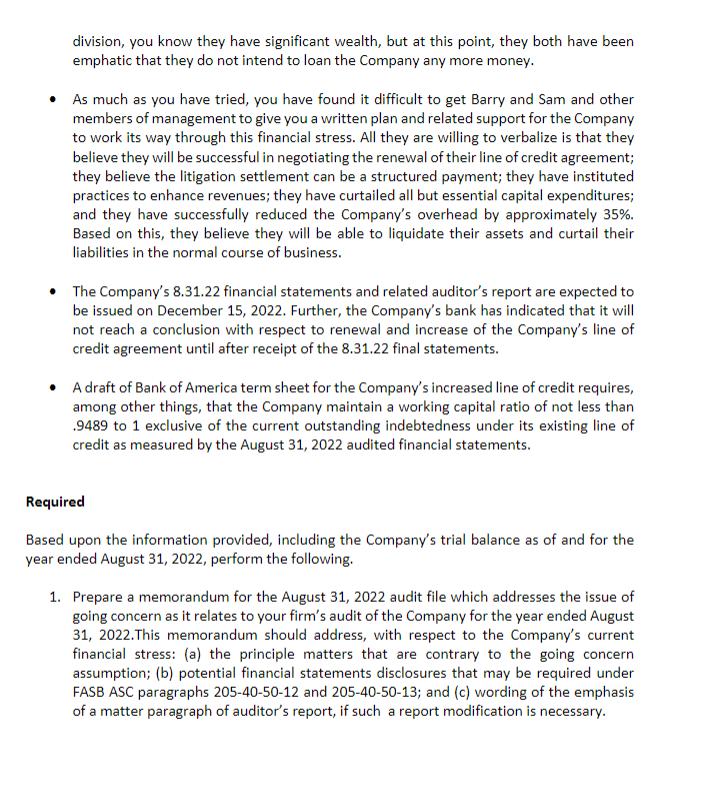

Sam and Barry Johnson, who are brothers, own all of the outstanding stock of RB Johnson Electric (the Company), an electrical contractor headquartered in Norfolk, Virginia. The Company was founded by the current owners' father in December of 1947 and has been in continuous operation since that date. The Company performs commercial electrical construction for small to medium size commercial projects in the Hampton Roads area of Virginia. The Company employs about 50 people and for the most recent year ended August 31, 20226.23, had approximately $50 million in contract revenues and a book value of less than $3,000,000. During both 2021 and 2022 the Company experienced significant losses on two large projects related to electrical construction for two apartment complexes. The reasons for the losses are varied but both projects were largely impacted by the Company's inability to find and employ qualified electricians and project managers for the projects. In addition, both of the projects were multi-story buildings and the Company has very little experience in this type of construction. Further, management of the Company bid the two projects very aggressively in an attempt to establish an ongoing relationship with this particular general contractor and a belief that the Company needed to increase its backlog. The Company's bookkeeper has prepared the following trial balances for the Company as of August 31, 2022, and 2021, the Company's year-end. In order to avoid any issues of independence with your firm, the Company employs another CPA firm to adjust its accounts on a monthly basis. This service, based on your prior experience with the Company, provides accurate information as of and for the period presented. 8.31.22 Cash Accounts receivable Retainage receivable Contract assets Property and equipment Accumulated depreciation Accounts payable Other accrued liabilities Contract liabilities Line of credit bank Long term debt Common stock Retained earnings Contract revenues Cost of contract revenues General and administrative expenses 30,000 75,000 10,000 1,000,000 450,000 47,500,000 1,500,000 450,000 275,000 25,000 875,000 2,000,000 75,000 2,000 1,863,000 45,000,000 50,565,000 50,565,000 8.31.21 Cash Accounts receivable Retainage receivable Contract assets Property and equipment Accumulated depreciation Accounts payable Other accrued liabilities Contract liabilities Line of credit bank Long term debt Common stock Retained earnings Contract revenues Cost of contract revenues General and administrative expenses 75,000 650,000 405,000 875,000 450,000 43,000,000 2,275,000 450,000 100,000 20,000 20,000 0 0 2,000 2,138,000 45,000,000 47,730,000 47,730,000 Other Information In addition to the problem jobs, Barry and Sam Johnson tell you over lunch that their attorney has recently notified them that an appeal of the patent infringement lawsuit that has been ongoing for the last several years has been denied. This patent relates to management of energy in commercial buildings and has contributed significantly to the Company's historical earnings. The Company's attorney estimates that the lawsuit will cost $1,000,000 to settle, but settlement of the lawsuit would allow the Company to continue using the energy management technology. The Company's line of credit agreement permits short-term borrowing up to a total of $3,000,000 and is currently uncollateralized. The agreement expires on 10.15.22 and negotiations for its renewal and a possible increase (to $5,000,000) are ongoing with Bank of America. Although the loan officer has been encouraging, she indicates that the division manager has asked a lot of questions regarding the agreement and whether or not Barry and Sam Johnson would be willing to offer a personal guarantee of the line. Both Barry and Sam have indicated that they would consider a partial guarantee of the line. One of the Company's major vendors has placed the Company on very strict payment terms of net due upon delivery of current purchases. This same vendor is also in the process of negotiating repayment of its current outstanding balance on a structured repayment plan. This supplier represents substantially all of the Company's accounts payable at 8.31.22. The supplier is suggesting repayment of the outstanding balance in 5 equal instalments of $40,000 each starting on 10.15.22. No interest would be charged. According to the Company's bookkeeper, all payroll has been made and all payroll taxes are up to date. She also indicated, however, that she has been late in making some of the deposits and expects to be really stretched for cash with the next payroll deposit that will be due on 11.15.22 in the amount of $125,000. She also indicated to you, privately, that she is beginning to hear rumors of an area competitor that is chasing some of the Company's key field personnel. Although she denies that she would ever accept an offer from this same competitor, she did admit that she had received such an offer. The bookkeeper has been with the Company for over 25 years. During the year ended 8.31.22, Barry and Sam Johnson loaned the Company on a long- term basis (due 8.31.32) $75,000. The loan bears interest at 2.5% and the proceeds were used to purchase a piece of electrical equipment that was needed to complete one of the problem jobs. The Canadian vendor required payment in full prior to the equipment being shipped. Based on the fact that your firm prepares personal tax returns for both Barry and Sam and both of them exclusively invest with your firm's money management division, you know they have significant wealth, but at this point, they both have been emphatic that they do not intend to loan the Company any more money. As much as you have tried, you have found it difficult to get Barry and Sam and other members of management to give you a written plan and related support for the Company to work its way through this financial stress. All they are willing to verbalize is that they believe they will be successful in negotiating the renewal of their line of credit agreement; they believe the litigation settlement can be a structured payment; they have instituted practices to enhance revenues; they have curtailed all but essential capital expenditures; and they have successfully reduced the Company's overhead by approximately 35%. Based on this, they believe they will be able to liquidate their assets and curtail their liabilities in the normal course of business. The Company's 8.31.22 financial statements and related auditor's report are expected to be issued on December 15, 2022. Further, the Company's bank has indicated that it will not reach a conclusion with respect to renewal and increase of the Company's line of credit agreement until after receipt of the 8.31.22 final statements. A draft of Bank of America term sheet for the Company's increased line of credit requires, among other things, that the Company maintain a working capital ratio of not less than .9489 to 1 exclusive of the current outstanding indebtedness under its existing line of credit as measured by the August 31, 2022 audited financial statements. Required Based upon the information provided, including the Company's trial balance as of and for the year ended August 31, 2022, perform the following. 1. Prepare a memorandum for the August 31, 2022 audit file which addresses the issue of going concern as it relates to your firm's audit of the Company for the year ended August 31, 2022. This memorandum should address, with respect to the Company's current financial stress: (a) the principle matters that are contrary to the going concern assumption; (b) potential financial statements disclosures that may be required under FASB ASC paragraphs 205-40-50-12 and 205-40-50-13; and (c) wording of the emphasis of a matter paragraph of auditor's report, if such a report modification is necessary.

Step by Step Solution

★★★★★

3.38 Rating (145 Votes )

There are 3 Steps involved in it

Step: 1

Memorandum Date Insert Date To Audit File From Your Name Subject Going Concern Assessment for RB Johnson Electric the Company I have conducted an assessment of the going concern assumption for RB John...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles Of Taxation For Business And Investment Planning 2016 Edition

Authors: Sally Jones, Shelley Rhoades Catanach

19th Edition

1259549259, 978-1259618536, 1259618536, 978-1259549250