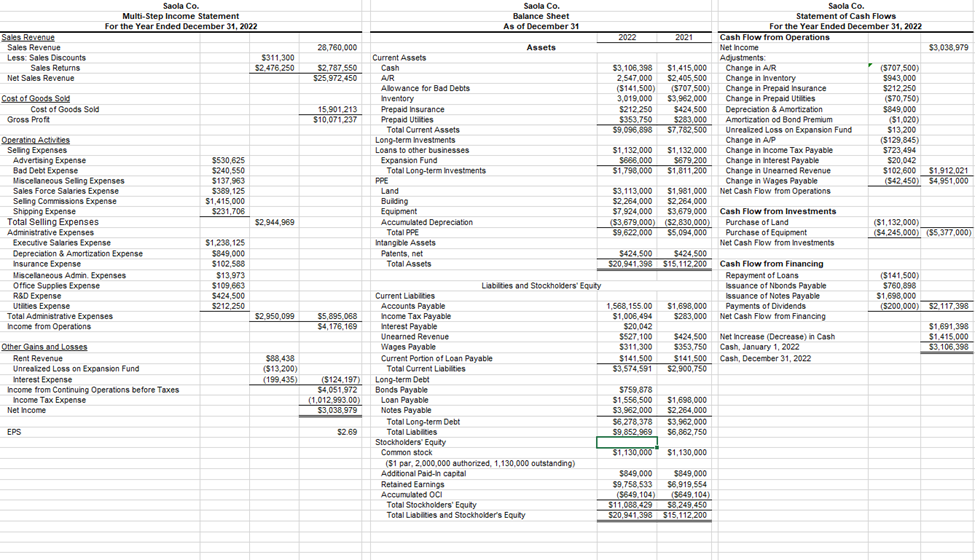

Question

Saola has traditionally purchased all of its manufacturing equipment. However, in 2022 they were unable to find a vendor willing to sell them a new

Saola has traditionally purchased all of its manufacturing equipment. However, in 2022 they were unable to find a vendor willing to sell them a new $12,426,000 machine. After some careful negotiations, however, they were able to lease the needed equipment for 5 years. At the end of the lease Saola will have the option to purchase the equipment for $994,000, the estimated fair value at the end of the lease. They currently plan to exercise the option and keep the equipment at the end of the lease, but that could change if they find a better option.

The machine has an estimated economic life of 7 years with no salvage value. The payments on the lease will be $2,412,148. Saola does not know the implicit interest rate used by the vendor, but their incremental interest rate is 6.0%. The lease period began on May 1, 2022 and the first payment was made that day. Subsequent payments will be made each year and should be paid one day before the start date to ensure that no late penalties are accrued. In addition to the first payment, Saola paid $18,000 in legal and other lease origination fees on May 1, 2022.

Saola has decided to keep all of its accumulated depreciation in one account rather than createA separate account for leased assets.

Saola's management would like to know the effect of your adjustment on the following ratios:

Profit Margin

Debt-to-Equity

ROA

Calculations

1. Make the appropriate journal entries, if any, to account for the lease (including any necessary changes to income tax expense)

2. Make any necessary changes to the financial statements. Please see the hints about the special adjustment to the Statement of Cash Flows.

Critical Thinking

3. Calculate each of the required ratios using the original values (before any changes) and the updated values (after your changes).

4. How does this new lease affect Saola's risk? Defend your answer using your ratios and key numbers in the updated financial statements. Give your answer, do think the lease was a good idea or should the company have found a way to purchase the equipment outright? Defend your answer.

5. Management has asked the accounting department to ensure that the new lease be structured as an operating lease, even changing the contract if necessary to keep the cost of the lease in rent expense instead of adding to interest expense and depreciation. Saola's controller feels that the company should get the most appropriate contract for their needs, then worry about the accounting classification. Provide two (2) arguments that the controller could use to convince the management team that her plan is the most appropriate

Hints:

1.Don't forget to check to see how this lease should be classified by Saola.

2.While you will need to add a new 'ROU asset' account to Saola's Balance Sheet, Saola's management wants ALL of the accumulated depreciation and amortization on PPE (including leased assets) to be combined in one account on the balance sheet.

3. Technically, a Lease Liability should be broken into current and long-term portions on Saola's Balance Sheet based on when the payment will be made. However, for the sake of simplicity, classify the entire amount as long-term for this Saola. Remember that the lease liability balance will also include any accrued, but unpaid interest as of December 31st

4.You will need to make three adjustments to your Statement of Cash Flows. The first will be for the actual cash paid ON THE LEASE, and it will be a new line item in the Financing Activities section. The second will be for the actual cash paid FOR THE INITIAL COSTS, and it will be an increase to the Cash Paid for Equipment. The third is a special adjustment to the Operating Activities section for the interest expense accrued. Normally when you record interest expense, the other account is interest payable, which automatically updates with the equations in Operating Activities section. However, for this entry, you put the interest directly into the lease payable account. So, net income has dropped, but no payments were made. To remove the non-cash interest (i.e. the interest NOT paid this year), you will need to change the equation in the Change in Interest Payable line to include the interest on the lease. Then, since that line item isn't just the Change in Interest Payable anymore, you'll need to change the title to be Change in Interest Accrued.

5.Make sure that you round all of your numbers to the nearest dollar! That's a general rule for Saola, and it is especially important with all of the PV estimates and other calculations you will need to make in this portion of the project. If necessary, use the "rounddown" for your Income Tax Expense calculation, since we have done a lot of rounding up to this point in the project that can easily throw off this calculation and make your B/S off by $1.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Audit Criteria For Electronic Document Management Processes And Associated IT Solutions

Authors: Alexander D Balzer, Dr Klaus-Peter Elpel, Volker Feist

5th Edition

3932898281, 978-3932898280