Answered step by step

Verified Expert Solution

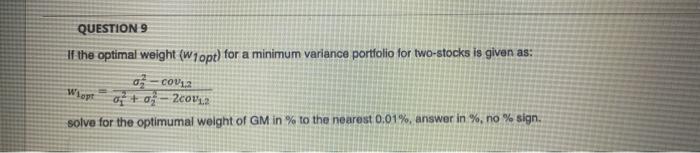

Question

1 Approved Answer

scription ructions You consider General Motors (ticker GM) and Ford Motor (icker and decide to allocate equal capital to both. The discrete monthly mean return

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Derivatives A Blessing Or A Curse

Authors: Simon Grima, Eleftherios I. Thalassinos

1st Edition

1789732468, 9781789732467