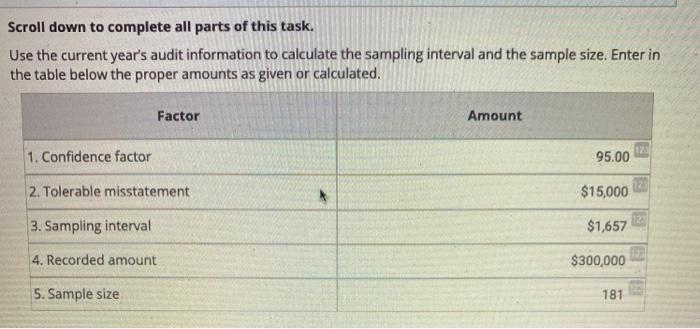

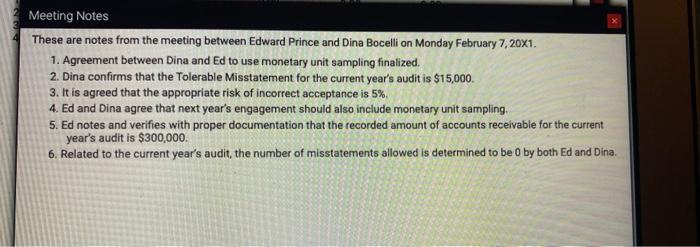

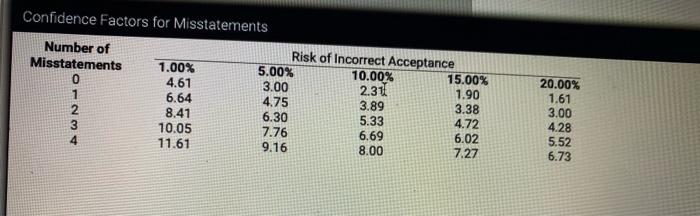

Scroll down to complete all parts of this task. Use the current year's audit information to calculate the sampling interval and the sample size. Enter in the table below the proper amounts as given or calculated. Factor Amount 1. Confidence factor 95.00 2. Tolerable misstatement $15,000 3. Sampling interval $1,657 4. Recorded amount $300,000 5. Sample size 181 Meeting Notes These are notes from the meeting between Edward Prince and Dina Bocelli on Monday February 7, 20x1. 1. Agreement between Dina and Ed to use monetary unit sampling finalized. 2. Dina confirms that the Tolerable Misstatement for the current year's audit is $15,000 3. It is agreed that the appropriate risk of incorrect acceptance is 5% 4. Ed and Dina agree that next year's engagement should also include monetary unit sampling. 5. Ed notes and verifies with proper documentation that the recorded amount of accounts receivable for the current year's audit is $300,000. 6. Related to the current year's audit, the number of misstatements allowed is determined to be o by both Ed and Dina. Confidence Factors for Misstatements Number of Risk of Incorrect Acceptance Misstatements 1.00% 5.00% 10.00% 15.00% 0 4.61 3.00 2.31 1.90 1 6.64 4.75 3.89 3.38 8.41 6.30 5.33 4.72 10.05 7.76 6.69 6.02 11.61 9.16 8.00 7.27 AN- 20.00% 1.61 3.00 4.28 5.52 6.73 Scroll down to complete all parts of this task. Use the current year's audit information to calculate the sampling interval and the sample size. Enter in the table below the proper amounts as given or calculated. Factor Amount 1. Confidence factor 95.00 2. Tolerable misstatement $15,000 3. Sampling interval $1,657 4. Recorded amount $300,000 5. Sample size 181 Meeting Notes These are notes from the meeting between Edward Prince and Dina Bocelli on Monday February 7, 20x1. 1. Agreement between Dina and Ed to use monetary unit sampling finalized. 2. Dina confirms that the Tolerable Misstatement for the current year's audit is $15,000 3. It is agreed that the appropriate risk of incorrect acceptance is 5% 4. Ed and Dina agree that next year's engagement should also include monetary unit sampling. 5. Ed notes and verifies with proper documentation that the recorded amount of accounts receivable for the current year's audit is $300,000. 6. Related to the current year's audit, the number of misstatements allowed is determined to be o by both Ed and Dina. Confidence Factors for Misstatements Number of Risk of Incorrect Acceptance Misstatements 1.00% 5.00% 10.00% 15.00% 0 4.61 3.00 2.31 1.90 1 6.64 4.75 3.89 3.38 8.41 6.30 5.33 4.72 10.05 7.76 6.69 6.02 11.61 9.16 8.00 7.27 AN- 20.00% 1.61 3.00 4.28 5.52 6.73