Answered step by step

Verified Expert Solution

Question

1 Approved Answer

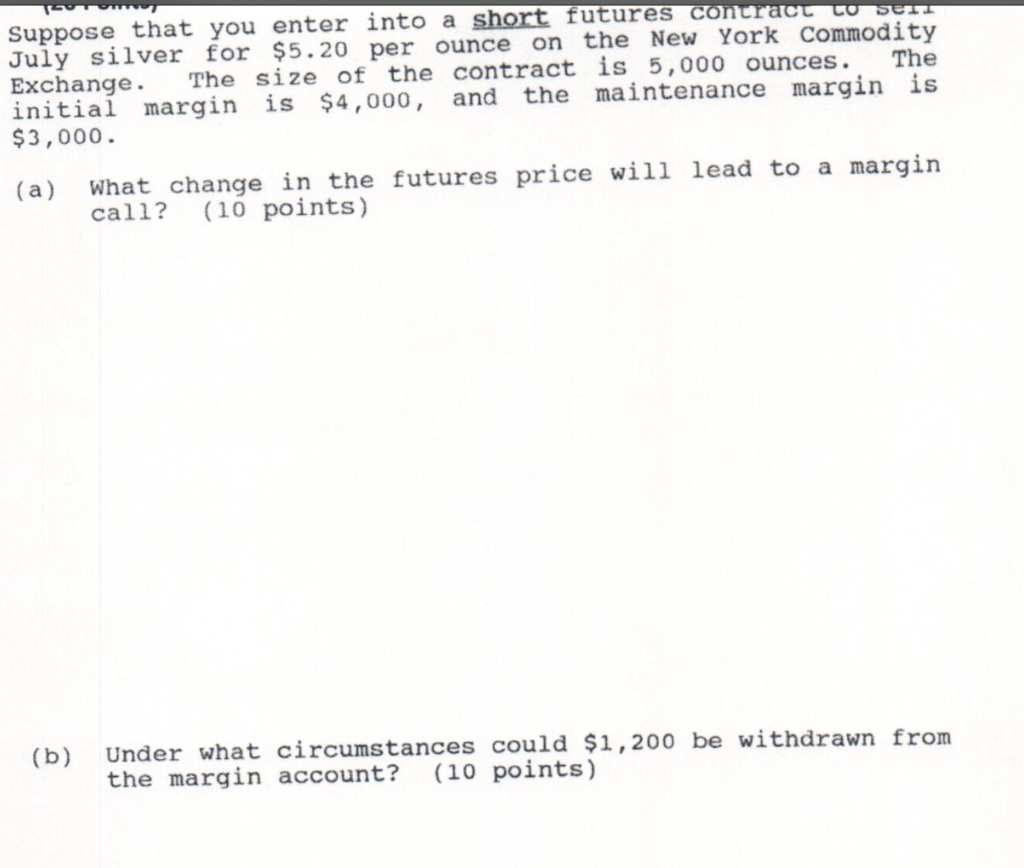

Se Suppose that you enter into a short futures contract July silver for $5.20 per ounce on the New York Commodity Exchange. The size of

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Student Solutions Manual To Accompany Loss Models From Data To Decisions

Authors: Stuart A. Klugman , Harry H. Panjer, Gordon E. Willmot

4th Edition

1118315316,1118472616