Question

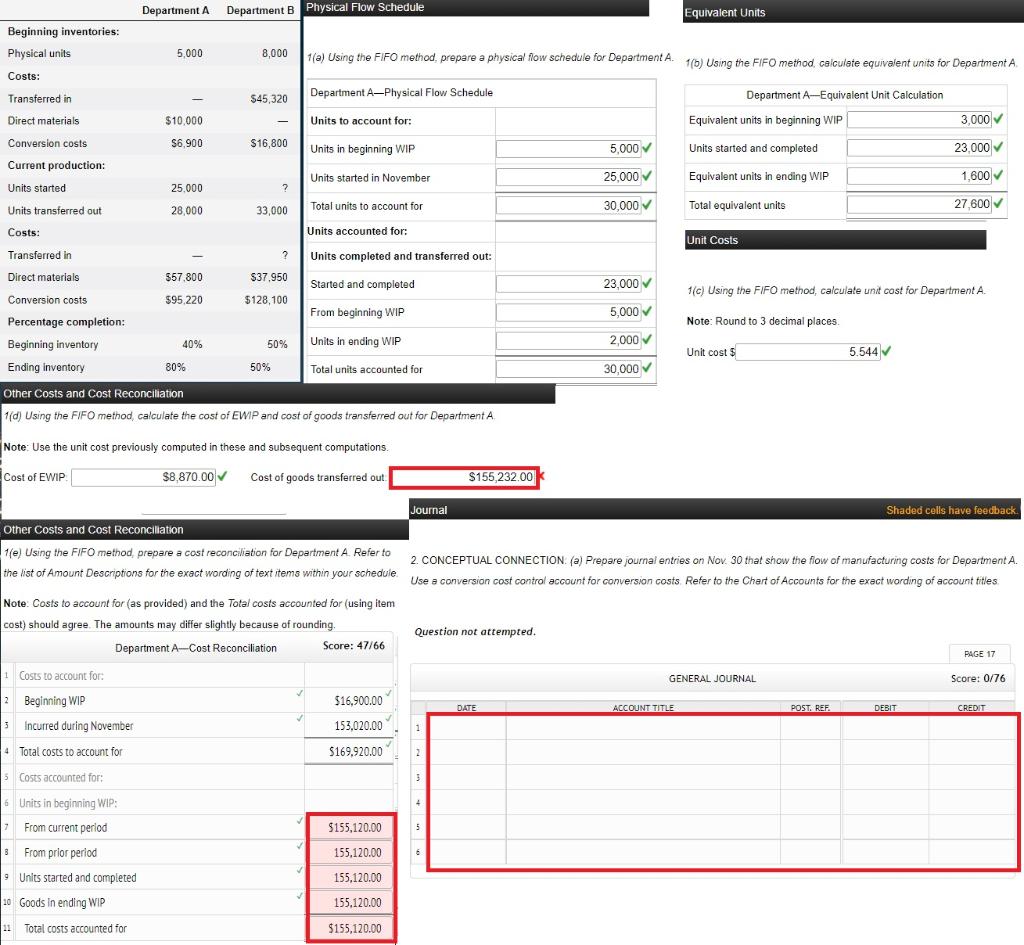

Seacrest Company uses a process costing system. The company manufactures a product that is processed in two departments: A and B. As work is completed,

Seacrest Company uses a process costing system. The company manufactures a product that is processed in two departments: A and B. As work is completed, it is transferred out. All inputs are added uniformly in Department A. The following summarizes the production activity and costs for November:

| Required: | |

| 1. Using the FIFO method, prepare the following for Department A: (a) a physical flow schedule DONE, (b) an equivalent unit calculation DONE, (c) calculation of unit costs (round to two decimal places) DONE, (d) cost of EWIP and cost of goods transferred out, 1/2 DONE - NEED HELP and (e) a cost reconciliation NEED HELP. | |

| (f) CONCEPTUAL CONNECTION: Prepare journal entries that show the flow of manufacturing costs for Department A. Use a conversion cost control account for conversion costs. Many firms are now combining direct labor and overhead costs into one category. They are not tracking direct labor separately. Offer some reasons for this practice. NEED HELP |

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Energy Audit Of Building Systems An Engineering Approach

Authors: Moncef Krarti

1st Edition

0849395879, 978-0849395871