Answered step by step

Verified Expert Solution

Question

1 Approved Answer

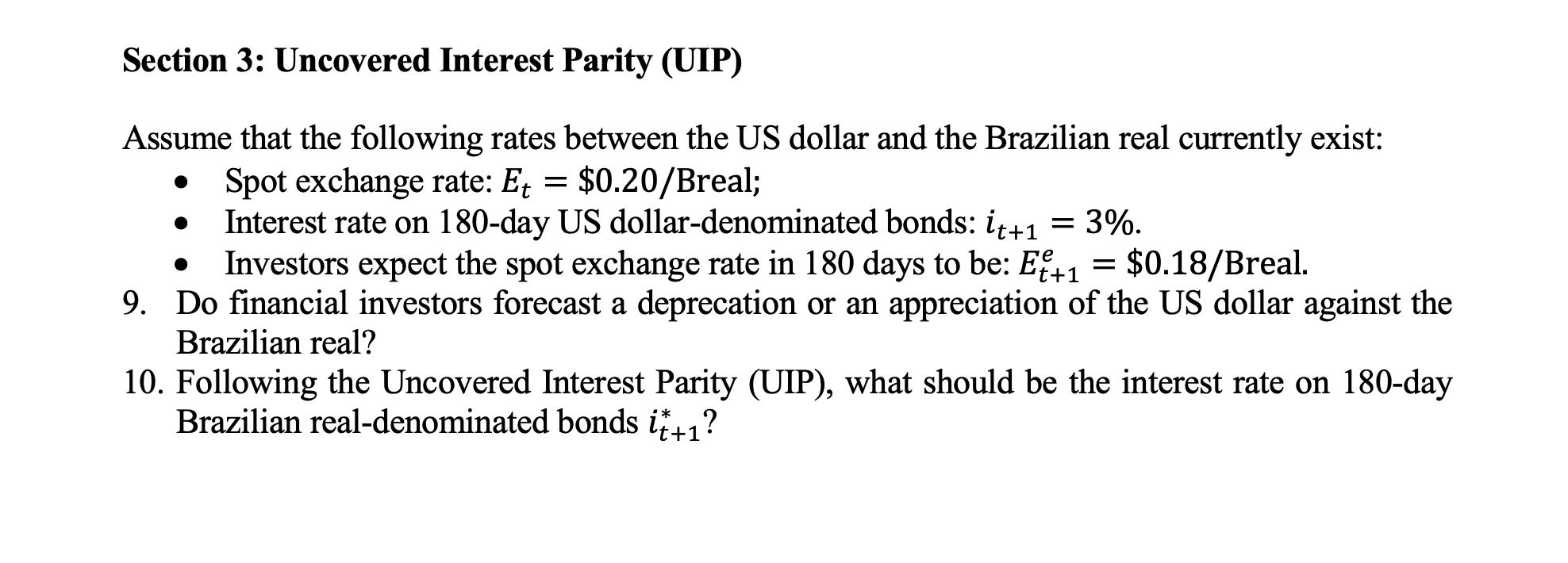

Section 3 : Uncovered Interest Parity ( UIP ) Assume that the following rates between the US dollar and the Brazilian real currently exist: Spot

Section : Uncovered Interest Parity UIP

Assume that the following rates between the US dollar and the Brazilian real currently exist:

Spot exchange rate: $real;

Interest rate on day US dollardenominated bonds:

Investors expect the spot exchange rate in days to be: $ Breal.

Do financial investors forecast a deprecation or an appreciation of the US dollar against the

Brazilian real?

Following the Uncovered Interest Parity UIP what should be the interest rate on day

Brazilian realdenominated bonds

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Research In Finance Volume 24

Authors: Andrew H. Chen

1st Edition

0762313773, 978-0762313778