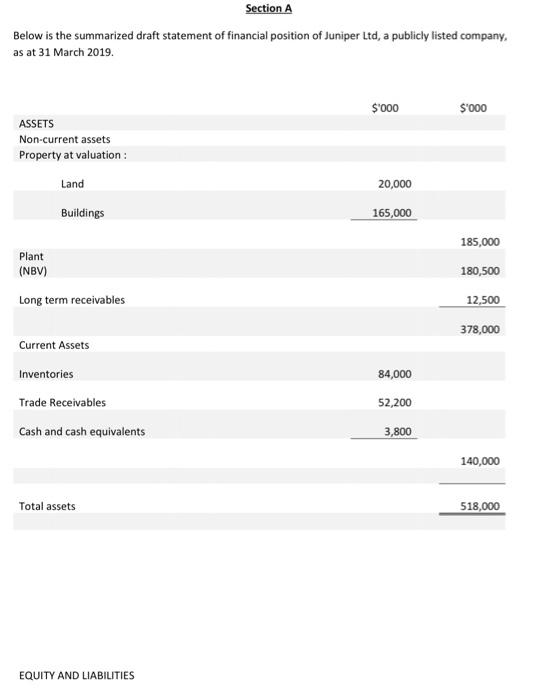

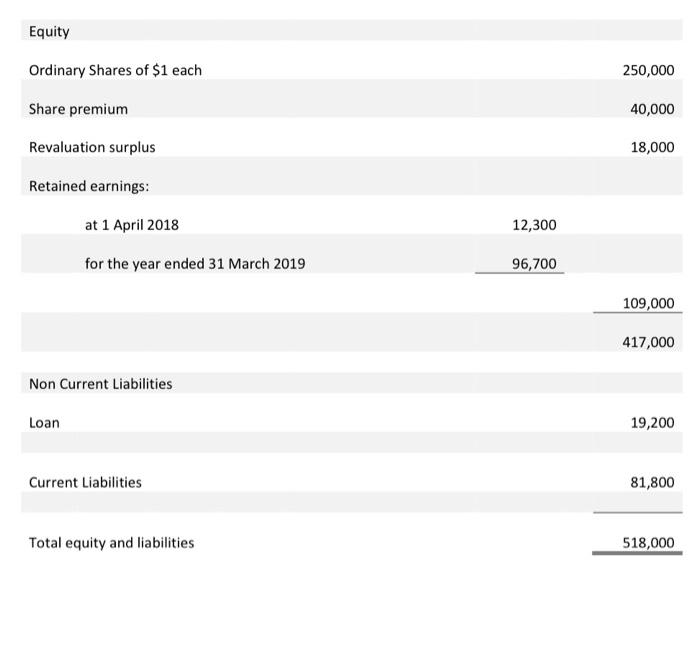

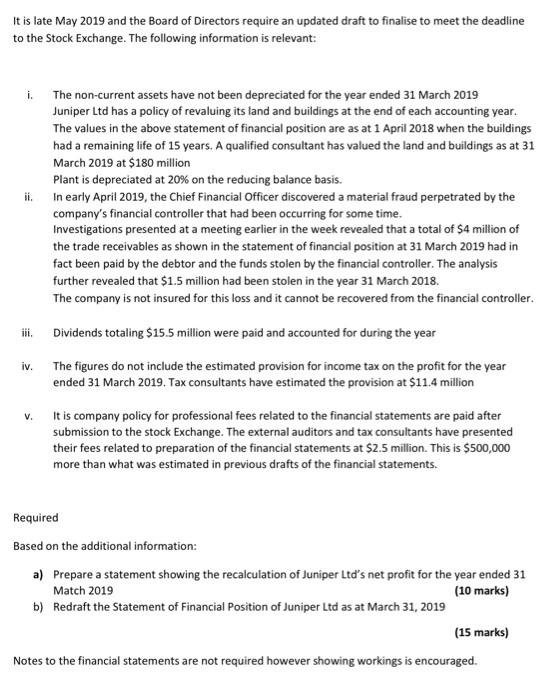

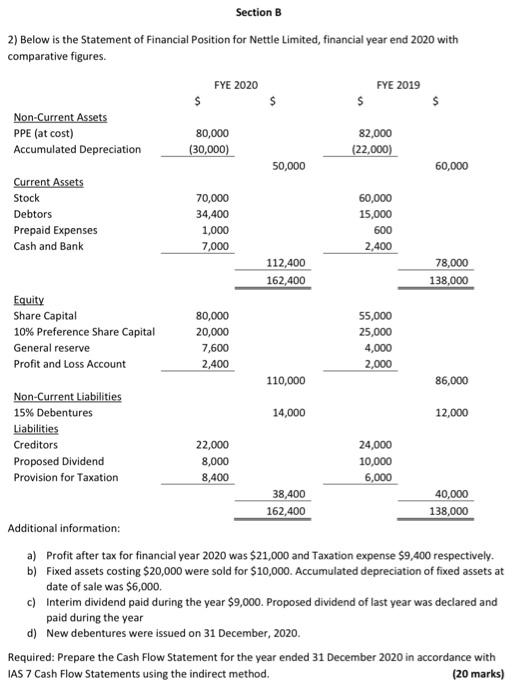

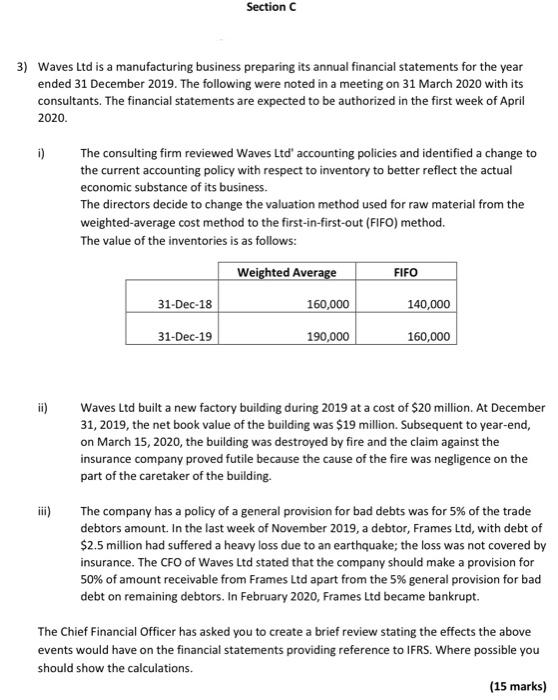

Section A Below is the summarized draft statement of financial position of Juniper Ltd, a publicly listed company, as at 31 March 2019. $'000 $'000 ASSETS Non-current assets Property at valuation : Land 20,000 Buildings 165,000 185,000 Plant (NBV) 180,500 Long term receivables 12,500 378,000 Current Assets Inventories Trade Receivables 84,000 52,200 Cash and cash equivalents 3,800 140,000 Total assets 518,000 EQUITY AND LIABILITIES Equity 250,000 Ordinary Shares of $1 each Share premium 40,000 Revaluation surplus 18,000 Retained earnings: at 1 April 2018 12,300 for the year ended 31 March 2019 96,700 109,000 417,000 Non Current Liabilities Loan 19,200 Current Liabilities 81,800 Total equity and liabilities 518,000 It is late May 2019 and the Board of Directors require an updated draft to finalise to meet the deadline to the Stock Exchange. The following information is relevant: ii. i. The non-current assets have not been depreciated for the year ended 31 March 2019 Juniper Ltd has a policy of revaluing its land and buildings at the end of each accounting year. The values in the above statement of financial position are as at 1 April 2018 when the buildings had a remaining life of 15 years. A qualified consultant has valued the land and buildings as at 31 March 2019 at $180 million Plant is depreciated at 20% on the reducing balance basis. In early April 2019, the Chief Financial Officer discovered a material fraud perpetrated by the company's financial controller that had been occurring for some time. Investigations presented at a meeting earlier in the week revealed that a total of $4 million of the trade receivables as shown in the statement of financial position at 31 March 2019 had in fact been paid by the debtor and the funds stolen by the financial controller.The analysis further revealed that $1.5 million had been stolen in the year 31 March 2018. The company is not insured for this loss and it cannot be recovered from the financial controller. iii. Dividends totaling $15.5 million were paid and accounted for during the year The figures do not include the estimated provision for income tax on the profit for the year ended 31 March 2019. Tax consultants have estimated the provision at $11.4 million iv. V. It is company policy for professional fees related to the financial statements are paid after submission to the stock Exchange. The external auditors and tax consultants have presented their fees related to preparation of the financial statements at $2.5 million. This is $500,000 more than what was estimated in previous drafts of the financial statements. Required Based on the additional information: a) Prepare a statement showing the recalculation of Juniper Ltd's net profit for the year ended 31 Match 2019 (10 marks) b) Redraft the Statement of Financial Position of Juniper Ltd as at March 31, 2019 (15 marks) Notes to the financial statements are not required however showing workings is encouraged. Section B 2) Below is the Statement of Financial Position for Nettle Limited, financial year end 2020 with comparative figures. FYE 2020 FE 2019 $ $ $ Non-Current Assets PPE (at cost) 80,000 82,000 Accumulated Depreciation (30,000) (22,000) 50,000 60,000 Current Assets Stock 70,000 60,000 Debtors 34,400 15,000 Prepaid Expenses 1,000 600 Cash and Bank 7,000 2,400 112,400 78,000 162,400 138,000 Equity Share Capital 80,000 55,000 10% Preference Share Capital 20,000 25,000 General reserve 7,600 4,000 Profit and Loss Account 2,400 2,000 110,000 86,000 Non-Current Liabilities 15% Debentures 14,000 12,000 Liabilities Creditors 22,000 24,000 Proposed Dividend 8,000 10,000 Provision for Taxation 8,400 6,000 38,400 40,000 162,400 138,000 Additional information: a) Profit after tax for financial year 2020 was $21,000 and Taxation expense $9,400 respectively. b) Fixed assets costing $20,000 were sold for $10,000. Accumulated depreciation of fixed assets at date of sale was $6,000 c) Interim dividend paid during the year $9,000. Proposed dividend of last year was declared and paid during the year d) New debentures were issued on 31 December, 2020. Required: Prepare the Cash Flow Statement for the year ended 31 December 2020 in accordance with IAS 7 Cash Flow Statements using the indirect method. (20 marks) Section 3) Waves Ltd is a manufacturing business preparing its annual financial statements for the year ended 31 December 2019. The following were noted in a meeting on 31 March 2020 with its consultants. The financial statements are expected to be authorized in the first week of April 2020 i) The consulting firm reviewed Waves Ltd' accounting policies and identified a change to the current accounting policy with respect to inventory to better reflect the actual economic substance of its business. The directors decide to change the valuation method used for raw material from the weighted average cost method to the first-in-first-out (FIFO) method. The value of the inventories is as follows: Weighted Average FIFO 31-Dec-18 160,000 140,000 31-Dec-19 190,000 160,000 ii) Waves Ltd built a new factory building during 2019 at a cost of $20 million. At December 31, 2019, the net book value of the building was $19 million. Subsequent to year-end, on March 15, 2020, the building was destroyed by fire and the claim against the insurance company proved futile because the cause of the fire was negligence on the part of the caretaker of the building. The company has a policy of a general provision for bad debts was for 5% of the trade debtors amount. In the last week of November 2019, a debtor, Frames Ltd, with debt of $2.5 million had suffered a heavy loss due to an earthquake; the loss was not covered by insurance. The CFO of Waves Ltd stated that the company should make a provision for 50% of amount receivable from Frames Ltd apart from the 5% general provision for bad debt on remaining debtors. In February 2020, Frames Ltd became bankrupt. The Chief Financial Officer has asked you to create a brief review stating the effects the above events would have on the financial statements providing reference to IFRS. Where possible you should show the calculations. (15 marks) 4) The financial controller of Greener Pastures Inc is reviewing recent transactions related to property plant and equipment: i) Greener Pastures Inc, is installing a new plant at its production facility. It has incurred these costs: - Cost of the plant $250,000. - Initial delivery and handling cost $ 20,000.- Cost of site preparation $ 60,000. - Consultants used to advice on the acquisition $ 70,000. - Interest charges paid to supplier for deferred credit $ 20,000.- Estimated dismantling cost to be incurred after 7 years $ 30,000.- Operating losses before commercial production $40,000. ii) Greener Pastures Inc. has acquired a heavy road transporter at a cost of $ 100,000 (with no breakdown of component parts). The estimated useful life is 10 years and depreciation is calculated on a straight-line basis. At the end of the sixth year, the roller requires replacement, as further maintenance is uneconomical due to the off-road time required. The value of the roller at date of replacement was $33,500 and was scrapped for parts without compensation. The remainder of the vehicle is perfectly road worthy and is expected to last for the next four years. The cost of the new roller is $ 45,000 The accounting team does not know if the roller can be recognized as an asset and if so, what treatment they should use for original and new roller. The financial controller requires you to create a brief review to state how the above transactions should be treated according to IFRS. They requested you show calculations where necessary. (15 marks) 5) New Medz Pharmaceutical is a young small drug company that specializes in research and development. i) Acquired patent for established successful drug that has a remaining life of 8 years. An expert consultancy firm has estimated the current value of the patent to be $20 million. ii) New Medz has developed and patented a new drug, "Clora", which was approved for medical use on 1 February 2019. The cost of developing the drug was $24 million of which $11.5 million was incurred after date of approval. Based on early assessments its recoverable amount is estimated at $10 million. The directors wish to capitalize the full cost of developing the drug. ) The company spent $2.5 million sending staff on a specialist training course at the beginning of the current year. The directors noted that though the course was expensive they have seen a marked improvement in production quality, increase in revenue and cost reductions. The directors of New Medz believe these benefits will continue for another 2 years and wish to capitalize the training costs as an intangible asset. iv) New Medz invested $1.8 million into their advertising campaign for their new drug Clora'. The advertising agency told them it would build brand recognition for many years to come. The directors are of the opinion they should capitalize the advertising campaign. Their accounting team has asked for your opinion in respect of recognizing the above as assets, and if so, what is their accounting treatment, for the year 31 December 2019 with reference to IFRS. For the transactions that cannot be capitalized you are required to give the directors details of the reasons in relation to IFRS. (15 marks) 6) Heavy Lifting Trucking (HLT) Ltd specializes in construction and development. The following transactions were highlighted for review by the financial controller: i) A machine was purchased on 1 January 2020 with an estimated useful life of 5 years and no residual value; therefore, $100,000 of depreciation was recognized on a straight line basis for 2020. At 31 December 2020, the CFO and auditing committee determined the fair value of the asset to be $74,000 and based on projected cash flow, noted its value in use is $68,000. ii) On 1 January 2021, HLT Ltd entered into a contract with Client A to refurbish an old building and install an elevator for $9 million. They also included the service of a 2 year maintenance on the elevator in the contract. The services would be monthly and start on the last day of the month after installation. At time of negotiations, the HLT Ltd directors agreed that the standalone price for servicing is $2 million and the elevator purchase and installation is $4 million. Based on previous projects they reasonably estimated, using that basic cost plus a margin approach, that the renovations would have a $ 4 million revenue. Client A made a 50% deposit at beginning of contract. Elevator was installed on 31 October 2021 and renovations were completed on 1 December 2021. The remaining deposit from Client is A is still outstanding. The accounting team is unclear as to when revenue from this project should be recognized in the accounts. The financial controller requires you to make a brief review stating the effects the above events would have on the financial statements for 31 December 2021, providing reference to IFRS. Where possible you should show the calculations. The financial controller also wants to see all the journal entries for the year pertaining to the contact with Client A. Round calculations to two (2) decimal places where necessary. (15 marks)