Answered step by step

Verified Expert Solution

Question

1 Approved Answer

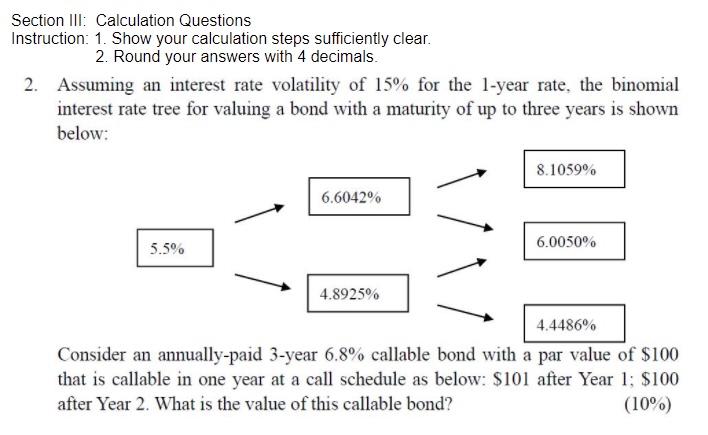

Section III: Calculation Questions Instruction: 1. Show your calculation steps sufficiently clear. 2. Round your answers with 4 decimals. 2. Assuming an interest rate volatility

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Corporate Finance

Authors: Mark R. Eaker, Frank J. Fabozzi, Dwight Grant

1st Edition

0030693063, 9780030693069