Answered step by step

Verified Expert Solution

Question

1 Approved Answer

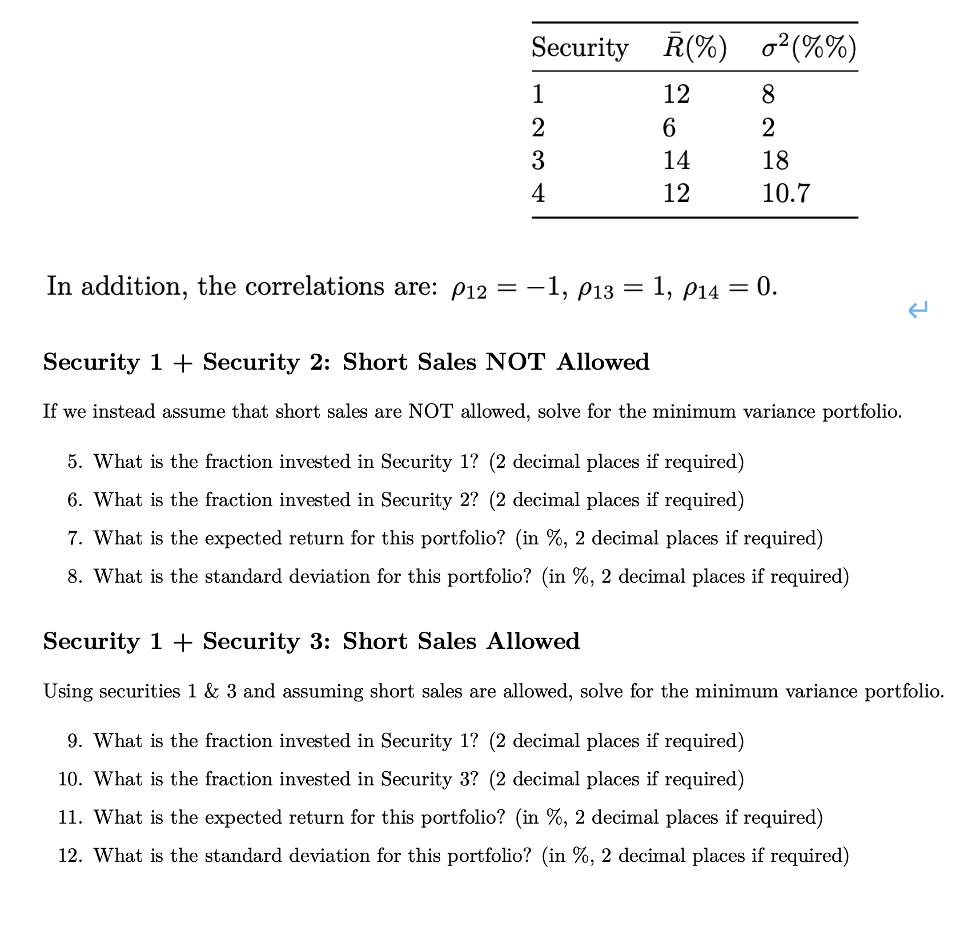

Security R(%) 1 12 2 6 3 14 4 12 In addition, the correlations are: P12 = -1, P13 1, P14 = 0. Security 1+

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting Essentials You Always Wanted To Know Self Learning Management Series

Authors: Vibrant Publishers , Kalpesh Ashar

5th Edition

1636510973, 978-1636510972