see attachment C courseworks2.columbia.edu/courses/147903/quizzes/123642/take Spring 2022 D Question 3 1 pts Home Read the following and answer questions 3-6: Announcements Robert, has a client who

see attachment

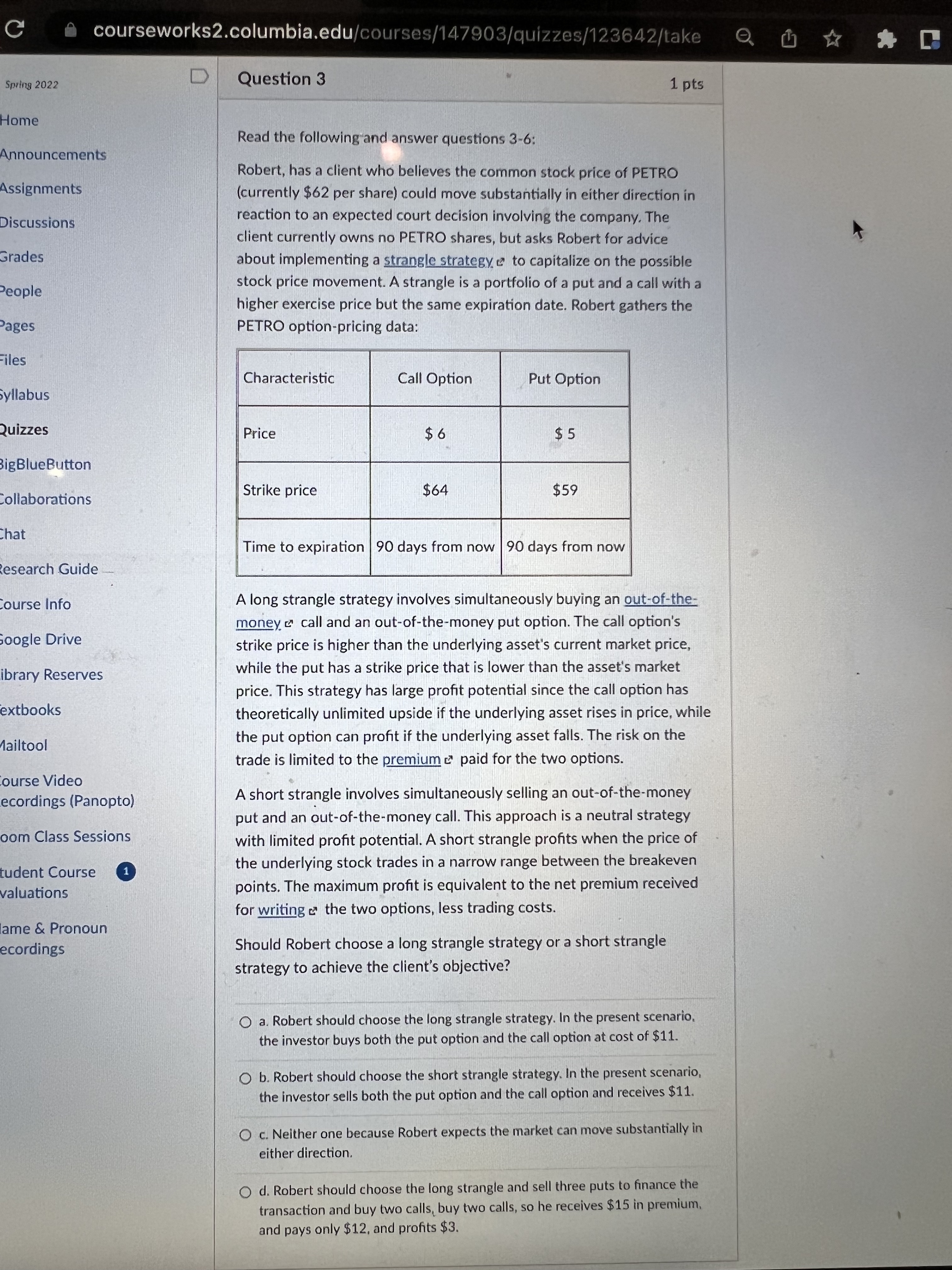

C courseworks2.columbia.edu/courses/147903/quizzes/123642/take Spring 2022 D Question 3 1 pts Home Read the following and answer questions 3-6: Announcements Robert, has a client who believes the common stock price of PETRO Assignments (currently $62 per share) could move substantially in either direction in Discussions reaction to an expected court decision involving the company. The client currently owns no PETRO shares, but asks Robert for advice Grades about implementing a strangle strategy e to capitalize on the possible People stock price movement. A strangle is a portfolio of a put and a call with a higher exercise price but the same expiration date. Robert gathers the Pages PETRO option-pricing data: Files Characteristic Call Option Put Option Syllabus Quizzes Price $6 $ 5 igBlueButton Collaborations Strike price $64 $59 hat Time to expiration | 90 days from now |90 days from now esearch Guide Course Info A long strangle strategy involves simultaneously buying an out-of-the- money c call and an out-of-the-money put option. The call option's Google Drive strike price is higher than the underlying asset's current market price, ibrary Reserves while the put has a strike price that is lower than the asset's market price. This strategy has large profit potential since the call option has extbooks theoretically unlimited upside if the underlying asset rises in price, while Mailtool the put option can profit if the underlying asset falls. The risk on the trade is limited to the premium c paid for the two options. ourse Video ecordings (Panopto) A short strangle involves simultaneously selling an out-of-the-money put and an out-of-the-money call. This approach is a neutral strategy oom Class Sessions with limited profit potential. A short strangle profits when the price of tudent Course the underlying stock trades in a narrow range between the breakeven valuations points. The maximum profit is equivalent to the net premium received for writing & the two options, less trading costs. ame & Pronoun ecordings Should Robert choose a long strangle strategy or a short strangle strategy to achieve the client's objective? O a. Robert should choose the long strangle strategy. In the present scenario, the investor buys both the put option and the call option at cost of $11. O b. Robert should choose the short strangle strategy. In the present scenario, the investor sells both the put option and the call option and receives $11. O c. Neither one because Robert expects the market can move substantially in either direction. O d. Robert should choose the long strangle and sell three puts to finance the transaction and buy two calls, buy two calls, so he receives $15 in premium, and pays only $12, and profits $3

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance