Answered step by step

Verified Expert Solution

Question

1 Approved Answer

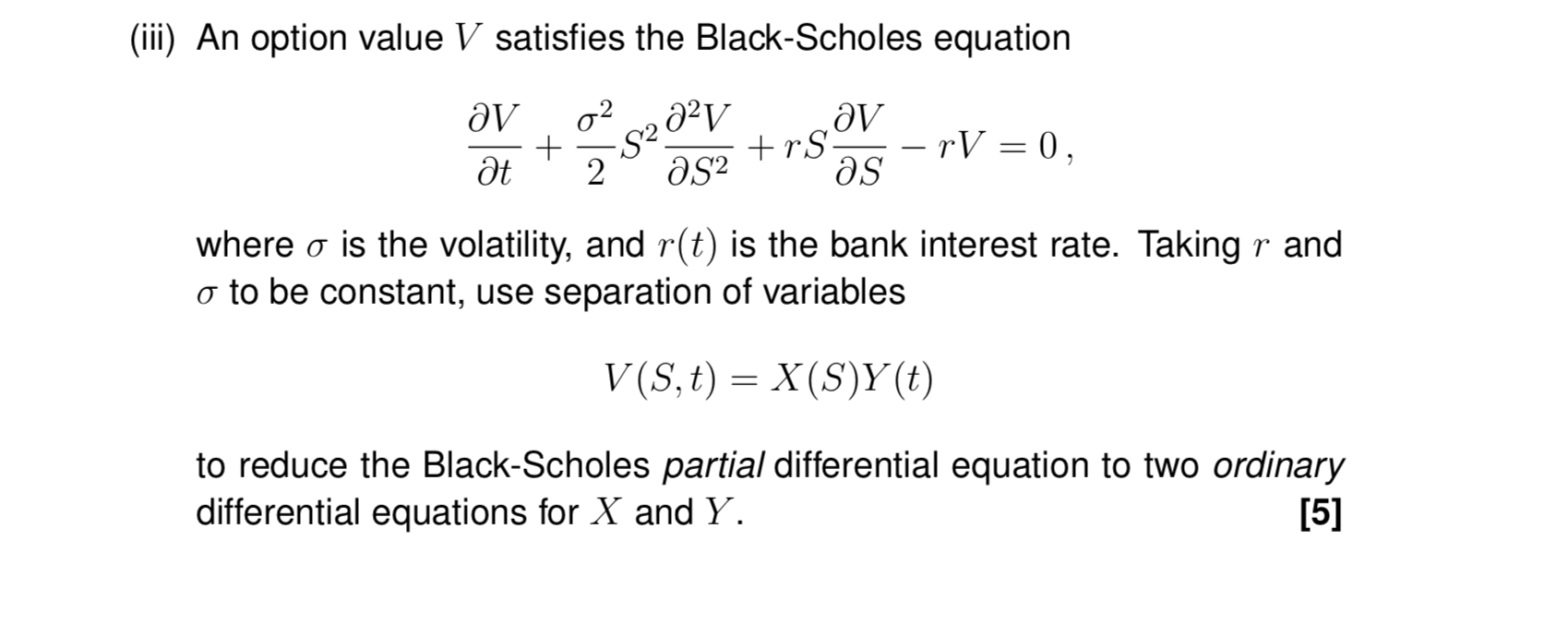

See the question below (iii) An option value V satisfies the Black-Scholes equation av 022321/ av 5+388824TSTV0, where a is the volatility, and r(t) is

See the question below

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Solutions Of The Examples In Higher Algebra

Authors: H S Hall ,S R Knight

1st Edition

B00AU0ZD3O