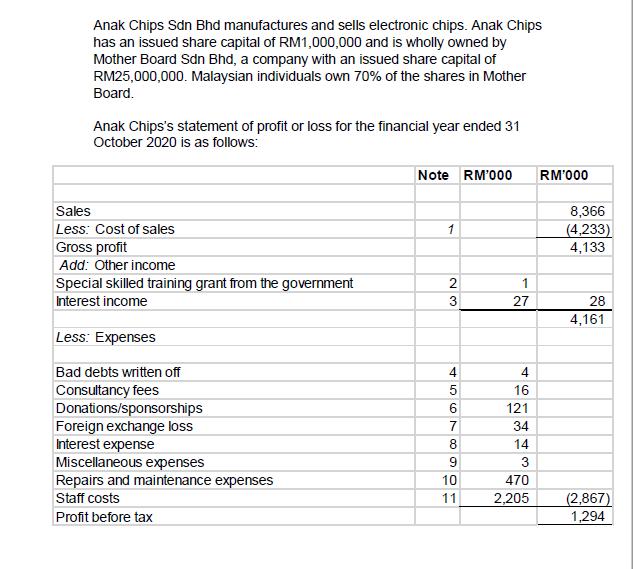

Anak Chips Sdn Bhd manufactures and sells electronic chips. Anak Chips has an issued share capital...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

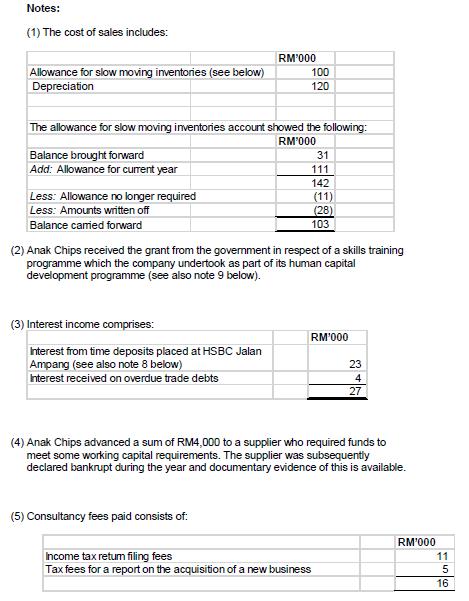

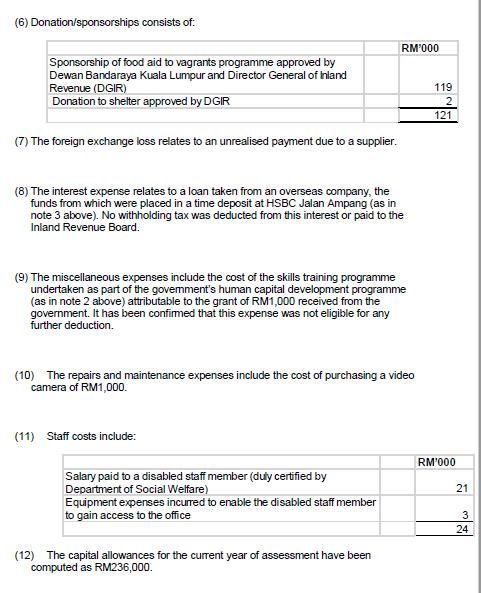

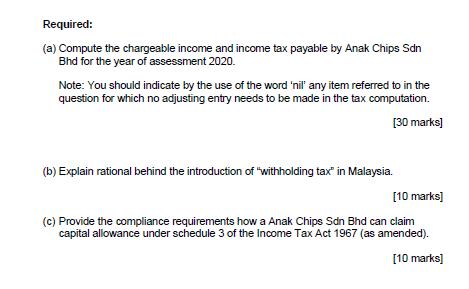

Anak Chips Sdn Bhd manufactures and sells electronic chips. Anak Chips has an issued share capital of RM1,000,000 and is wholly owned by Mother Board Sdn Bhd, a company with an issued share capital of RM25,000,000. Malaysian individuals own 70% of the shares in Mother Board. Anak Chips's statement of profit or loss for the financial year ended 31 October 2020 is as follows: Sales Less: Cost of sales Gross profit Add: Other income Special skilled training grant from the government Interest income Less: Expenses Bad debts written off Consultancy fees Donations/sponsorships Foreign exchange loss Interest expense Miscellaneous expenses Repairs and maintenance expenses Staff costs Profit before tax Note RM'000 1 23 4967 5 7 8901 10 11 1 27 4 st RM'000 8,366 (4,233) 4,133 28 4,161 16 121 34 14 3 470 2,205 (2,867) 1,294 Notes: (1) The cost of sales includes: Allowance for slow moving inventories (see below) Depreciation Balance brought forward Add: Allowance for current year The allowance for slow moving inventories account showed the following: RM'000 Less: Allowance no longer required Less: Amounts written off Balance carried forward RM'000 (3) Interest income comprises: Interest from time deposits placed at HSBC Jalan Ampang (see also note 8 below) Interest received on overdue trade debts 100 120 (5) Consultancy fees paid consists of: 31 111 142 (2) Anak Chips received the grant from the government in respect of a skills training programme which the company undertook as part of its human capital development programme (see also note 9 below). (11) (28) 103 RM'000 (4) Anak Chips advanced a sum of RM4,000 to a supplier who required funds to meet some working capital requirements. The supplier was subsequently declared bankrupt during the year and documentary evidence of this is available. 23 4 27 Income tax retum filing fees Tax fees for a report on the acquisition of a new business RM'000 11 5 16 (6) Donation/sponsorships consists of: Sponsorship of food aid to vagrants programme approved by Dewan Bandaraya Kuala Lumpur and Director General of Inland Revenue (DGIR) Donation to shelter approved by DGIR (7) The foreign exchange loss relates to an unrealised payment due to a supplier. (8) The interest expense relates to a loan taken from an overseas company, the funds from which were placed in a time deposit at HSBC Jalan Ampang (as in note 3 above). No withholding tax was deducted from this interest or paid to the Inland Revenue Board. (9) The miscellaneous expenses include the cost of the skills training programme undertaken as part of the government's human capital development programme (as in note 2 above) attributable to the grant of RM1,000 received from the government. It has been confirmed that this expense was not eligible for any further deduction. (10) The repairs and maintenance expenses include the cost of purchasing a video camera of RM1,000. (11) Staff costs include: RM'000 Salary paid to a disabled staff member (duty certified by Department of Social Welfare) Equipment expenses incurred to enable the disabled staff member to gain access to the office (12) The capital allowances for the current year of assessment have been computed as RM236,000. 119 2 121 RM'000 21 3 24 Required: (a) Compute the chargeable income and income tax payable by Anak Chips Sdn Bhd for the year of assessment 2020. Note: You should indicate by the use of the word 'nil' any item referred to in the question for which no adjusting entry needs to be made in the tax computation. [30 marks] (b) Explain rational behind the introduction of "withholding tax" in Malaysia. [10 marks] (c) Provide the compliance requirements how a Anak Chips Sdn Bhd can claim capital allowance under schedule 3 of the Income Tax Act 1967 (as amended). [10 marks] Anak Chips Sdn Bhd manufactures and sells electronic chips. Anak Chips has an issued share capital of RM1,000,000 and is wholly owned by Mother Board Sdn Bhd, a company with an issued share capital of RM25,000,000. Malaysian individuals own 70% of the shares in Mother Board. Anak Chips's statement of profit or loss for the financial year ended 31 October 2020 is as follows: Sales Less: Cost of sales Gross profit Add: Other income Special skilled training grant from the government Interest income Less: Expenses Bad debts written off Consultancy fees Donations/sponsorships Foreign exchange loss Interest expense Miscellaneous expenses Repairs and maintenance expenses Staff costs Profit before tax Note RM'000 1 23 4967 5 7 8901 10 11 1 27 4 st RM'000 8,366 (4,233) 4,133 28 4,161 16 121 34 14 3 470 2,205 (2,867) 1,294 Notes: (1) The cost of sales includes: Allowance for slow moving inventories (see below) Depreciation Balance brought forward Add: Allowance for current year The allowance for slow moving inventories account showed the following: RM'000 Less: Allowance no longer required Less: Amounts written off Balance carried forward RM'000 (3) Interest income comprises: Interest from time deposits placed at HSBC Jalan Ampang (see also note 8 below) Interest received on overdue trade debts 100 120 (5) Consultancy fees paid consists of: 31 111 142 (2) Anak Chips received the grant from the government in respect of a skills training programme which the company undertook as part of its human capital development programme (see also note 9 below). (11) (28) 103 RM'000 (4) Anak Chips advanced a sum of RM4,000 to a supplier who required funds to meet some working capital requirements. The supplier was subsequently declared bankrupt during the year and documentary evidence of this is available. 23 4 27 Income tax retum filing fees Tax fees for a report on the acquisition of a new business RM'000 11 5 16 (6) Donation/sponsorships consists of: Sponsorship of food aid to vagrants programme approved by Dewan Bandaraya Kuala Lumpur and Director General of Inland Revenue (DGIR) Donation to shelter approved by DGIR (7) The foreign exchange loss relates to an unrealised payment due to a supplier. (8) The interest expense relates to a loan taken from an overseas company, the funds from which were placed in a time deposit at HSBC Jalan Ampang (as in note 3 above). No withholding tax was deducted from this interest or paid to the Inland Revenue Board. (9) The miscellaneous expenses include the cost of the skills training programme undertaken as part of the government's human capital development programme (as in note 2 above) attributable to the grant of RM1,000 received from the government. It has been confirmed that this expense was not eligible for any further deduction. (10) The repairs and maintenance expenses include the cost of purchasing a video camera of RM1,000. (11) Staff costs include: RM'000 Salary paid to a disabled staff member (duty certified by Department of Social Welfare) Equipment expenses incurred to enable the disabled staff member to gain access to the office (12) The capital allowances for the current year of assessment have been computed as RM236,000. 119 2 121 RM'000 21 3 24 Required: (a) Compute the chargeable income and income tax payable by Anak Chips Sdn Bhd for the year of assessment 2020. Note: You should indicate by the use of the word 'nil' any item referred to in the question for which no adjusting entry needs to be made in the tax computation. [30 marks] (b) Explain rational behind the introduction of "withholding tax" in Malaysia. [10 marks] (c) Provide the compliance requirements how a Anak Chips Sdn Bhd can claim capital allowance under schedule 3 of the Income Tax Act 1967 (as amended). [10 marks]

Expert Answer:

Related Book For

Federal Taxation 2016 Comprehensive

ISBN: 9780134104379

29th edition

Authors: Thomas R. Pope, Timothy J. Rupert, Kenneth E. Anderson

Posted Date:

Students also viewed these accounting questions

-

Select an "X" for the entities or business forms that offer the tax advantage listed when doing business as that type of entity. (If the entity or business form does not create the advantage listed,...

-

There are two identical firms EQT Corp and DBT Corp except for their capital structure. For example none of the firms pay taxes, and both firms have EBIT of $15,000 per year for both firms. There is...

-

Danny Featherweight is taking a tough course in law school. His Prof agreed to give him a course grade of max{2x; 3y} where x and y are the number of answers he gets right on the first and second...

-

Codominance observable effect on the phenotype of a heter neither allele is recessive-both alleles are dominant. 6. Which of the genotypes results in a blood type that provides clear evidence of...

-

In a sample of 2016 U.S. adults, 383 said Franklin Roosevelt was the best president since World War II. Two U.S. adults are selected at random without replacement. (a) Find the probability that both...

-

A company issued five-year, 5% bonds with a par value of $100,000. The company received $95,735 for the bonds. Using the straight-line method, the companys interest expense for the first semiannual...

-

White Top Rafters uses the direct write-off method to account for bad debts. Record the following transactions that occurred during the year: May 3 Nov 8 Dec 10 Provided $970 of services to Sam...

-

The inventory of Hang Company was destroyed by fire on March 1. From an examination of the accounting records, the following data for the first 2 months of the year are obtained: Sales Revenue...

-

firm's president or chief executive officer (CEO) characteristically plays a dominant role in strategic planning at the firm. Explain why this can be desirable in many ways. Also explain what can...

-

Lombard Ltd has been offered a contract for which there is available production capacity. The contract is for 20,000 identical items, manufactured by an intricate assembly operation, to be produced...

-

Identify various national health insurance schemes existing in your country and list their merits.

-

Southern Company issued a $600,000 bond at 99% on January 1st. The bond has a two year life and pays 5% interest annually each December 31s t. Prepare the Appropriate Journal entries 2. Magnolia...

-

Digging Deeper: Interdependences between Practical components and other components 1. The author suggests that the nine components of the deliberations dimension "should not be thought of as...

-

Compute break - even units using the following formula: Break - Even Units = Total Fixed Costs / ( Unit Selling Price Unit Variable Cost ) suppose that a firm has an existing product with a combined...

-

4. Solve for n if 2(nC) = n+1C3-

-

Novak Company's standard materials cost per unit of output is $10 (2 kg x $5). During July, the company purchases and uses 3,300 kg of materials costing $16,929 in making 1,500 units of finished...

-

At the beginning of Year 2, Better Corporation's accounting equation showed the following accounts and balances: Event Balance BETTER CORPORATION Accounting Equation Assets Liabilities Cash Land...

-

The baseball player A hits the ball from a height of 3.36 ft with an initial velocity of 34.8 ft/s. 0.14 seconds after the ball is hit, player B who is standing 15 ft away from home plate begins to...

-

Alan, Barbara, and Dave are unrelated. Each has owned 100 shares of Time Corporation stock for five years and each has a $60,000 basis in those shares. Times E&P is $240,000. Time redeems all 100 of...

-

The following advertisement appeared in a financial journal: $17 MILLION CASH WITH ADDITIONAL CASH AVAILABLE $105 MM TAX LOSS GOOD THROUGH 2029 CAPITAL GROUP, INC. NASDAQ listed w/300 shareholders...

-

Mariel has a $60,000 basis in her partnership interest just before receiving a parcel of land as a liquidating distribution. She has no remaining precontribution gain and will receive no other...

-

For the Scotch yoke mechanism shown in Fig.3.27, find the velocity and acceleration of point \(B\). \(\omega_{2}=5 \mathrm{rad} / \mathrm{s}\), and \(O_{2} A=100 \mathrm{~mm}\). 2 45 3 .B. Scale: 1...

-

In Example 3.14 , calculate analytically, the acceleration of the piston and angular acceleration of the rod.

-

The crank of an engine \(300 \mathrm{~mm}\) long rotates at a uniform speed of \(300 \mathrm{rpm}\). The ratio of connecting rod length to crank radius is 4 . Determine (a) acceleration of the...

Study smarter with the SolutionInn App