Answered step by step

Verified Expert Solution

Question

1 Approved Answer

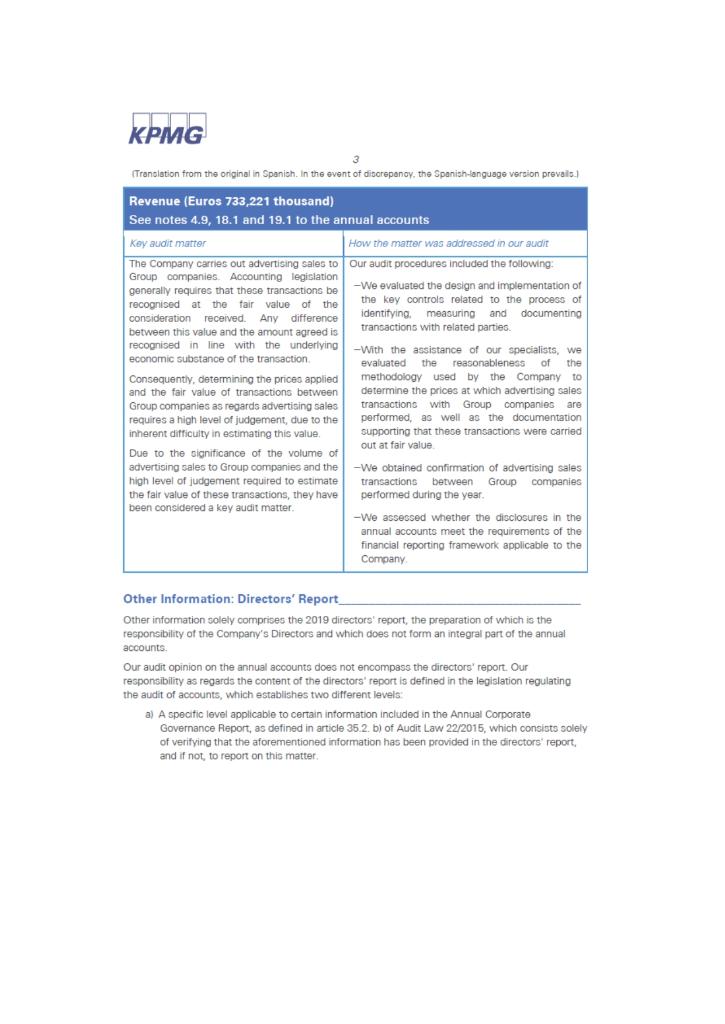

Select key audit issues. You can find them, in the Key Audit Matters paragraphs. For each one, explain auditors reasons of concern with that issue

- Select key audit issues. You can find them, in the Key Audit Matters paragraphs. For each one, explain auditors reasons of concern with that issue and how the described audit procedures being applied, can give response to them

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Contemporary Auditing

Authors: Michael C Knapp

12th Edition

357515404, 978-0357515402