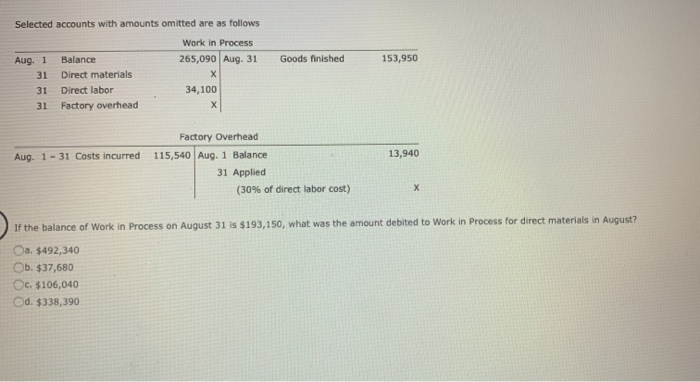

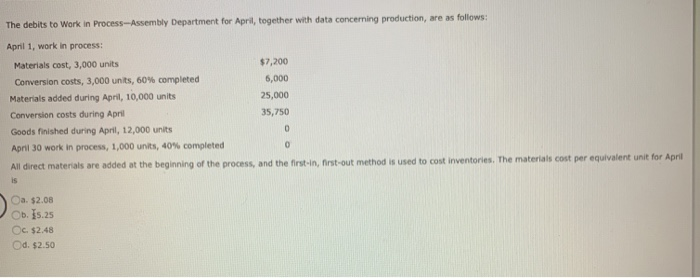

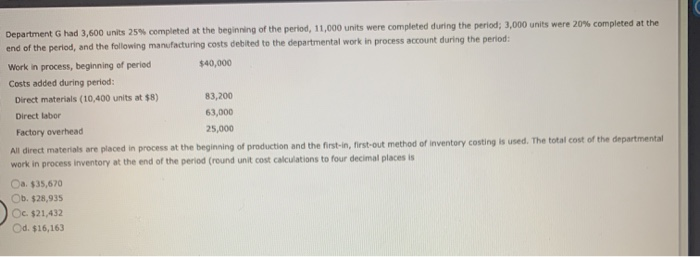

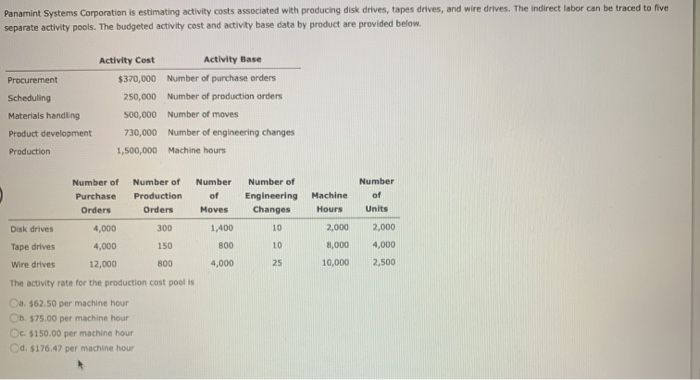

Selected accounts with amounts omitted are as follows Goods finished 153,950 Aug. 1 31 31 31 Balance Direct materials Direct labor Factory overhead Work in Process 265,090 Aug. 31 X 34,100 X 13,940 Factory Overhead Aug. 1-31 Costs incurred 115,540 Aug. 1 Balance 31 Applied (30% of direct labor cost) If the balance of Work in Process on August 31 is $193,150, what was the amount debited to Work in Process for direct materials in August? a. $492,340 Ob. $37,680 c. $106,040 d. $338,390 In applying the first-in, first-out method of costing inventories, if 8,000 units which were 30% completed are in process at June 1, 28,000 units were completed during June, and 4,000 units were 75% completed at June 30, the number of equivalent units of production for June was 33,400. True False The debits to Work in Process-Assembly Department for April, together with data concerning production, are as follows: April 1, work in process: Materials cost, 3,000 units $7,200 Conversion costs, 3,000 units, 60% completed 6,000 Materials added during April 10,000 units 25,000 Conversion costs during April 35,750 Goods finished during April 12,000 units 0 April 30 work in process, 1,000 units, 40% completed 0 All direct materials are added at the beginning of the process, and the first-in, first-out method is used to cost inventories. The materials cost per equivalent unit for April is a $2.08 b. 15.25 c. $2.48 d. $2.50 Department had 3,600 units 25% completed at the beginning of the period, 11,000 units were completed during the period; 3,000 units were 20% completed at the end of the period, and the following manufacturing costs debited to the departmental work in process account during the period: Work in process, beginning of period $40,000 Costs added during period: Direct materials (10,400 units at $8) 83,200 Direct labor 63,000 Factory overhead 25,000 All direct materials are placed in process at the beginning of production and the first in, first-out method of inventory costing is used. The total cost of the departmental work in process inventory at the end of the period (round unit cost calculations to four decimal places is a $35,670 Ob. $28,935 c. $21,432 Od. $16,163 Panamint Systems Corporation is estimating activity costs associated with producing disk drives, tapes drives, and wire drives. The Indirect labor can be traced to five separate activity pools. The budgeted activity cost and activity base data by product are provided below. Procurement Scheduling Materials handling Product development Production Activity Cost Activity Base $370,000 Number of purchase orders 250,000 Number of production orders 500,000 Number of moves 730,000 Number of engineering changes 1,500,000 Machine hours Number of Purchase Orders Number of Production Orders Number of Moves Number of Engineering Changes 10 Machine Hours 2,000 Number of Units 300 2,000 1,400 800 4,000 10 4,000 8,000 10,000 25 2,500 Disk drives 4,000 Tape drives 4,000 150 Wire drives 12,000 800 The activity rate for the production cost pool is Oa: $62.50 per machine hour Cb. $75.00 per machine hour c. $150.00 per machine hour d. $176.47 per machine hour