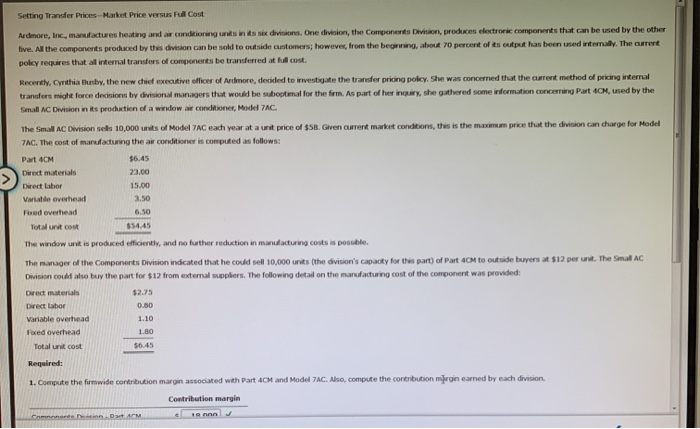

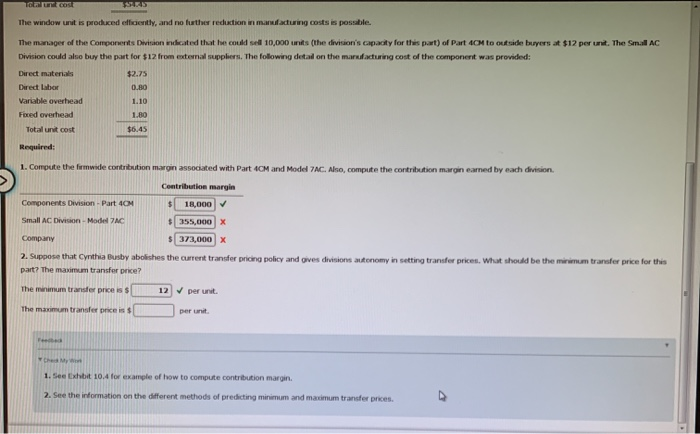

Setting Transder Prices-Market Price versus Full Cost Ardmore, Inc, manufactures heating and ar conditioning units in its six divisions. One division, the Components Division, produces electronic components that can be used by the other five. All the components produced by this division can be sold to outside customers; however, from the beginning, about 70 percent of ts output has been used internally. The current polcy requires that all intemal transfers of components be transferred at full cost. Recently, Cynthia Busby, the new chief executive officer of Ardmore, decided to investigate the transfer pricing policy. She was concermed that the aurrent method of pricing internal transfers might force decisions by divisional managers that would be suboptimal for the firm. As part of her inquiry, she gathered some information conceming Part 4CM, used by the Small AC Division in its production of a window ar conditioner, Model 7AC The Seall AC Division sells 10,000 units of Model 7AC each year at a unit price of $58. Gven aurent market conditions, this is the maximum price that the division can charge for Model 7AC. The cost of manufacturing the air conditioner is computed as follows: $6.45 Part 4CM 23.00 Direct materials Direct labor 15.00 Variable overhead 3.50 Fixed overhead 6.50 $54.45 Total unit cost The window unit is produced efficiently, and no further reduction in manudacturing costs is possble. The manager of the Components Division indicated that he could sell 10,000 unts (the division's capacty for this part) of Part 4CM to outside buyers at $12 per unit. The Small AC Division could also buy the part for $12 from external supplers. The following detail on the manufacturing cost of the component was provided $2.75 Direct materials Direct labor 0.80 Variable overhead 1.10 Foxed overhead 1.80 Total unit cost $6.45 Required: 1. Compute the firmwide contribution margin associated with Part 4CM and Model 7AC. Also, compute the contrbution margin earned by each division Contribution margin mnonente.Deeion.Dart ACM $54.45 Total unt cost The window unit is produced efficiently, and no further reduction in manufacturing costs is possible. The manager of the Components Division indicated that he could sell 10,000 units (the division's capacity for this part) of Part 4CM to outside buyers at $12 per unit. The Small AC Division could also buy the part for $12 from etemal suppliers. The following detail on the marufacturing cost of the component was provided: Direct materials $2.75 Direct labor 0.80 Variable overhead 1.10 Foxed overhead 1.80 Total unit cost $6.45 Required: 1. Compute the firmwide contribution margin associated with Part 4CM and Model 7AC. Also, compute the contribution margin eamed by each division. Contribution margin Components Division - Part 40M 18,000 Small AC Division-Model 7AC 355,000 X 373000| ompany 2. Suppose that Cynthia Busby abolishes the current transfer pricing policy and gives divisions autonomy in setting transfer prices. What should be the minimum transfer price for this part? The maximum transfer price? The minimum transfer price is $ 12 per unit. The maximum transfer price is $ per unit Feed Che My Wr 1. See Exhbit 10.4 for example of how to compute contribution margin 2. See the information on the different methods of predicting minimum and maximum transfer prices