Answered step by step

Verified Expert Solution

Question

1 Approved Answer

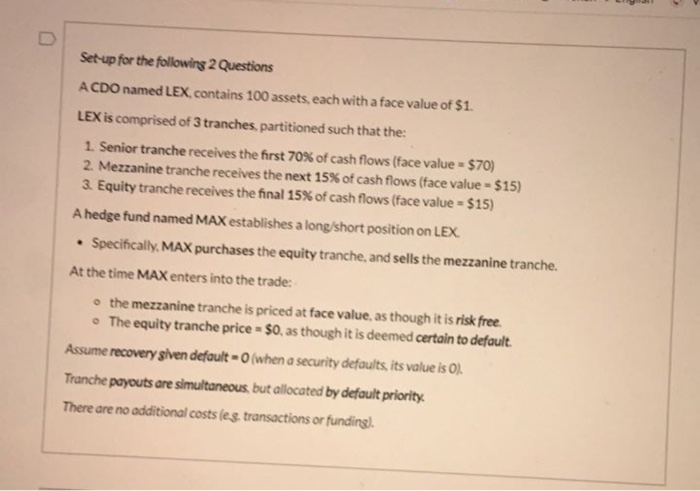

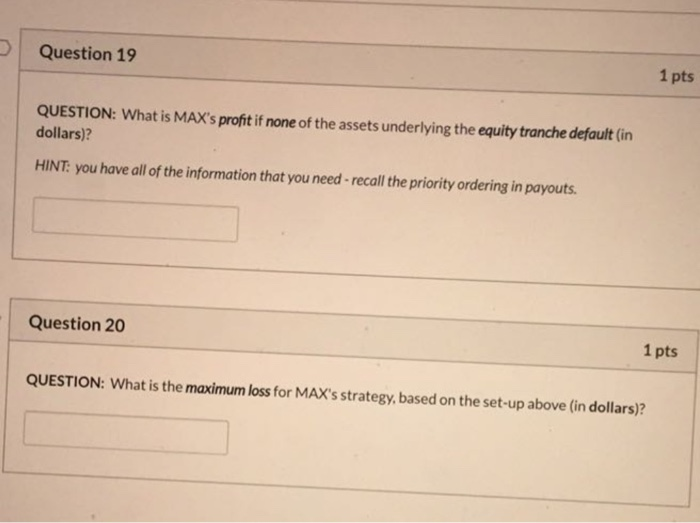

Set-up for the following 2 Questions A CDO named LEX contains 100 assets, each with a face value of $1. LEX is comprised of 3

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Forex Analysis And Strategies For Day Traders Profitable Investing With Currency Swaps Hedges And Scalps For Both Beginning And Advanced Traders

Authors: Steve Alkandros

1st Edition

1545117039, 978-1545117033