Question

Sheridan Corp. owns 75% of Concord Inc. Both companies are in the mining industry. During 2020, Sheridan Corp. purchased a building from Concord Inc. for

Sheridan Corp. owns 75% of Concord Inc. Both companies are in the mining industry. During 2020, Sheridan Corp. purchased a building from Concord Inc. for $1,990. The buildings original cost is $25,000 and its carrying amount in Concord Inc.s financial statements is $1,600. Sheridans Contributed Surplus account contains a credit balance of $260 from previous related-party transactions. Concords Contributed Surplus account is nil. There is no available independent evidence of the value of the building because it is a unique building in a remote part of the country. Sheridan subsequently sold the building, during 2021, to an unrelated party for $2,150. Both Sheridan and Concord follow ASPE. Using the related-party decision tree answer the following.

A) How would both Sheridan and Concord record the purchase and sale of the building during 2020?

B) Record the subsequent sale of the building by Sheridan during 2021.

C) Assume that the transaction is in the normal course of operations for both Sheridan and Concord and that it has commercial substance. Record the journal entries.

D) Calculate the total impact on income of the purchase and sale of the building for 2020 and 2021 for the consolidated reporting unit of the two companies. What can you conclude from your calculation?

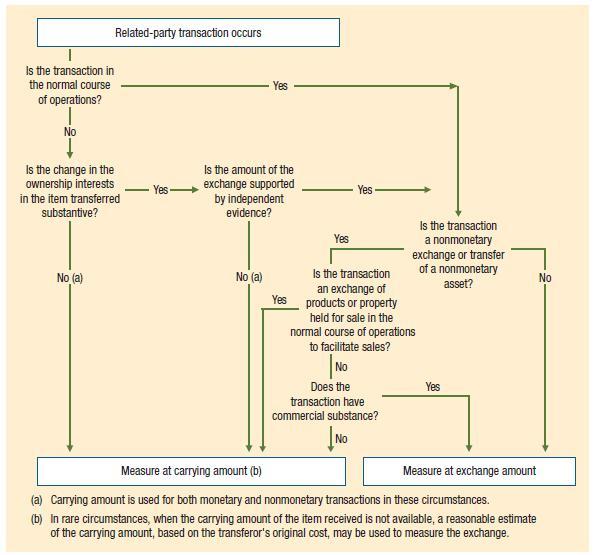

Related-party transaction occurs Is the transaction in the normal course of operations? Yes No Is the change in the ownership interests in the item transferred substantive? Yes No (a) No Is the amount of the exchange supported Yes by independent evidence? Is the transaction Yes a nonmonetary exchange or transfer No (a) Is the transaction of a nonmonetary an exchange of asset? Yes products or property held for sale in the normal course of operations to facilitate sales? NO Does the Yes transaction have commercial substance? No Measure at carrying amount (b) Measure at exchange amount (a) Carrying amount is used for both monetary and nonmonetary transactions in these circumstances. (b) In rare circumstances, when the carrying amount of the item received is not available, a reasonable estimate of the carrying amount, based on the transferor's original cost, may be used to measure the exchange. Related-party transaction occurs Is the transaction in the normal course of operations? Yes No Is the change in the ownership interests in the item transferred substantive? Yes No (a) No Is the amount of the exchange supported Yes by independent evidence? Is the transaction Yes a nonmonetary exchange or transfer No (a) Is the transaction of a nonmonetary an exchange of asset? Yes products or property held for sale in the normal course of operations to facilitate sales? NO Does the Yes transaction have commercial substance? No Measure at carrying amount (b) Measure at exchange amount (a) Carrying amount is used for both monetary and nonmonetary transactions in these circumstances. (b) In rare circumstances, when the carrying amount of the item received is not available, a reasonable estimate of the carrying amount, based on the transferor's original cost, may be used to measure the exchangeStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investments

Authors: Zvi Bodie, Alex Kane, Alan J. Marcus

9th Edition

73530700, 978-0073530703