Answered step by step

Verified Expert Solution

Question

1 Approved Answer

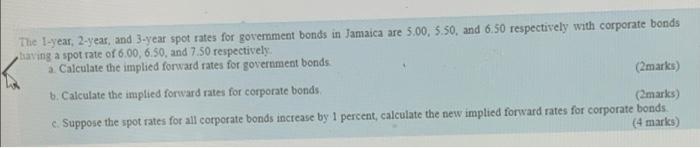

Show all working The 1-year, 2-year, and 3-year spot rates for government bonds in Jamaica are 5.00, 5.50, and 6.50 respectively with corporate bonds laving

Show all working

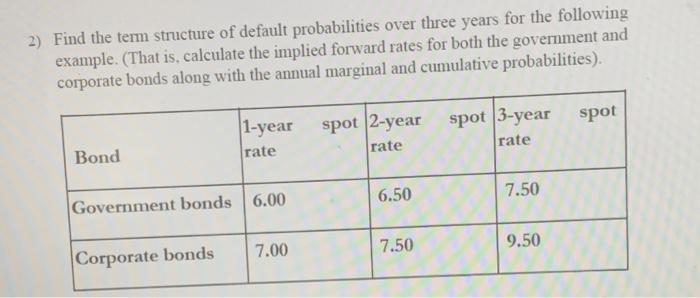

The 1-year, 2-year, and 3-year spot rates for government bonds in Jamaica are 5.00, 5.50, and 6.50 respectively with corporate bonds laving a spot rate of 6.00, 6.50, and 7.50 respectively a Calculate the implied forward rates for government bonds (2marks) b. Calculate the implied forward rates for corporate bonds (marks) c. Suppose the spot rates for all corporate bonds increase by 1 percent, calculate the new implied forward rates for corporate bonds (4 marks) 2) Find the term structure of default probabilities over three years for the following example. (That is, calculate the implied forward rates for both the government and corporate bonds along with the annual marginal and cumulative probabilities). 1-year rate spot 2-year rate spot 3-year spot rate Bond 6.50 7.50 Government bonds 6.00 7.00 7.50 9.50 Corporate bonds Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Handbook Of Research On Behavioral Finance And Investment Strategies Decision Making In The Financial Industry

Authors: Zeynep Copur

1st Edition

1466674849,1466674857