Answered step by step

Verified Expert Solution

Question

1 Approved Answer

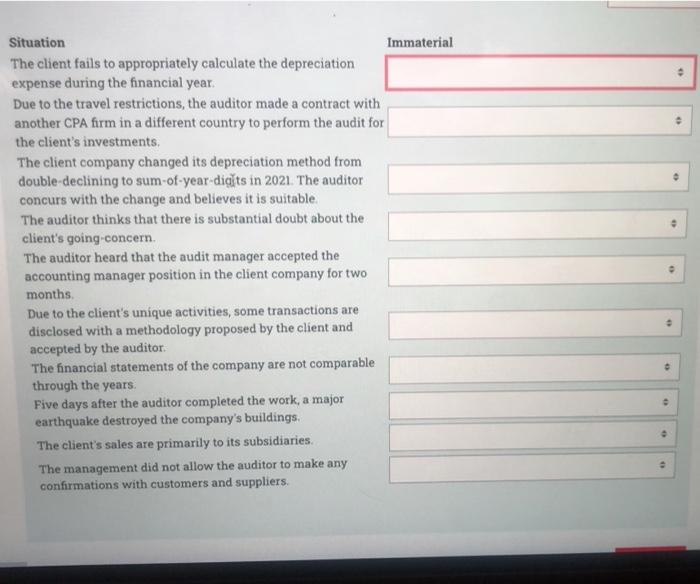

Situation Immaterial The client fails to appropriately calculate the depreciation expense during the financial year. Due to the travel restrictions, the auditor made a contract

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Ethics And The Internal Auditors Political Dilemma Tools And Techniques To Evaluate A Companys Ethical Culture Internal Audit And IT Audit

Authors: Lynn Fountain

1st Edition

149876780X, 978-1498767804