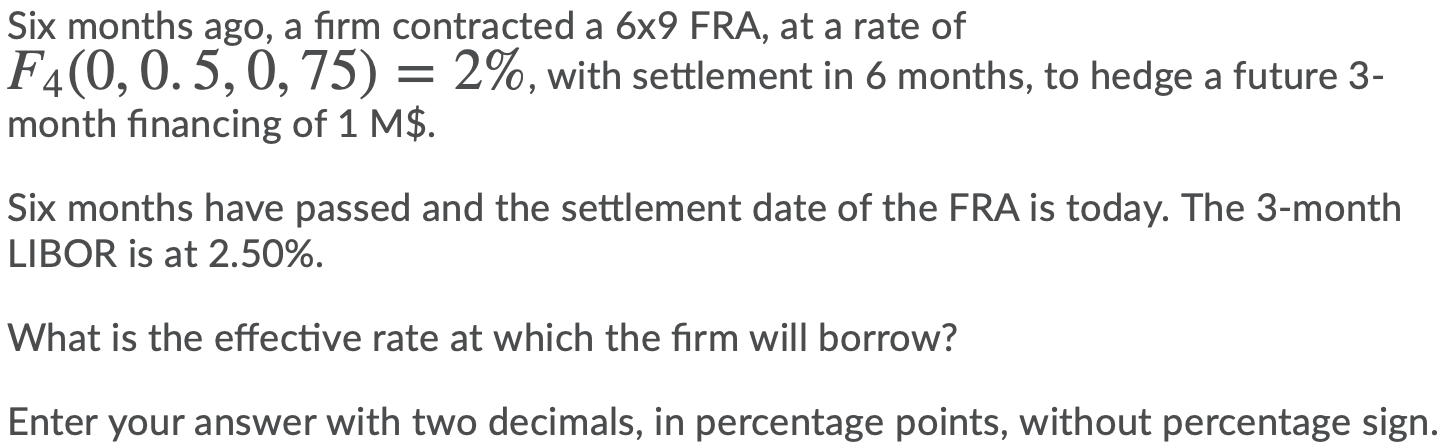

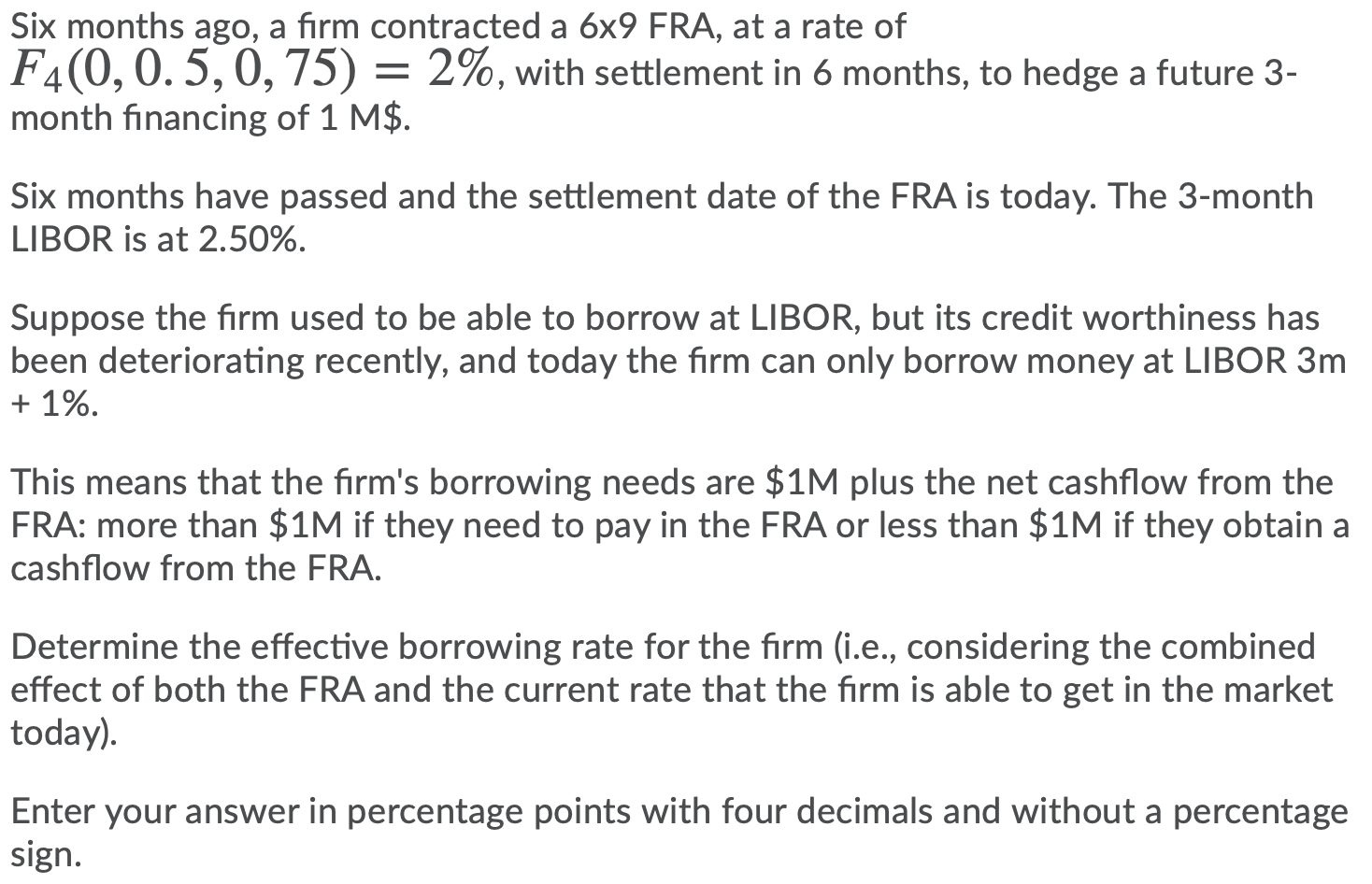

Six months ago, a firm contracted a 6x9 FRA, at a rate of F4(0,0.5,0, 75) = 2%, with settlement in 6 months, to hedge a future 3- ( , month financing of 1 M$. = Six months have passed and the settlement date of the FRA is today. The 3-month LIBOR is at 2.50%. What is the effective rate at which the firm will borrow? Enter your answer with two decimals, in percentage points, without percentage sign. Six months ago, a firm contracted a 6x9 FRA, at a rate of F4(0,0.5, 0, 75) = 2%, with settlement in 6 months, to hedge a future 3- month financing of 1 M$. = Six months have passed and the settlement date of the FRA is today. The 3-month LIBOR is at 2.50%. Suppose the firm used to be able to borrow at LIBOR, but its credit worthiness has been deteriorating recently, and today the firm can only borrow money at LIBOR 3m + 1%. This means that the firm's borrowing needs are $1M plus the net cashflow from the FRA: more than $1M if they need to pay in the FRA or less than $1M if they obtain a cashflow from the FRA. Determine the effective borrowing rate for the firm (i.e., considering the combined effect of both the FRA and the current rate that the firm is able to get in the market today). Enter your answer in percentage points with four decimals and without a percentage sign. Six months ago, a firm contracted a 6x9 FRA, at a rate of F4(0,0.5,0, 75) = 2%, with settlement in 6 months, to hedge a future 3- ( , month financing of 1 M$. = Six months have passed and the settlement date of the FRA is today. The 3-month LIBOR is at 2.50%. What is the effective rate at which the firm will borrow? Enter your answer with two decimals, in percentage points, without percentage sign. Six months ago, a firm contracted a 6x9 FRA, at a rate of F4(0,0.5, 0, 75) = 2%, with settlement in 6 months, to hedge a future 3- month financing of 1 M$. = Six months have passed and the settlement date of the FRA is today. The 3-month LIBOR is at 2.50%. Suppose the firm used to be able to borrow at LIBOR, but its credit worthiness has been deteriorating recently, and today the firm can only borrow money at LIBOR 3m + 1%. This means that the firm's borrowing needs are $1M plus the net cashflow from the FRA: more than $1M if they need to pay in the FRA or less than $1M if they obtain a cashflow from the FRA. Determine the effective borrowing rate for the firm (i.e., considering the combined effect of both the FRA and the current rate that the firm is able to get in the market today). Enter your answer in percentage points with four decimals and without a percentage sign