Answered step by step

Verified Expert Solution

Question

1 Approved Answer

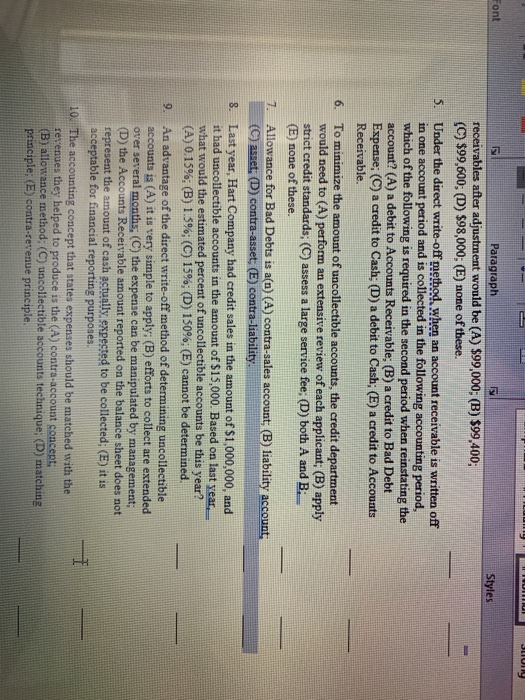

SLUI ront Styles | Paragraph receivables after adjustment would be (A) $99,000; (B) $99.400; (C) $99,600; (D) $98,000, (E) none of these. Under the direct

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing And Systems Exam Questions And Explanations Comprehensive Covarage Of Auditing And Systems Topics

Authors: Gleim, Hillison

22nd Edition

1618544284, 978-1618544285