Question

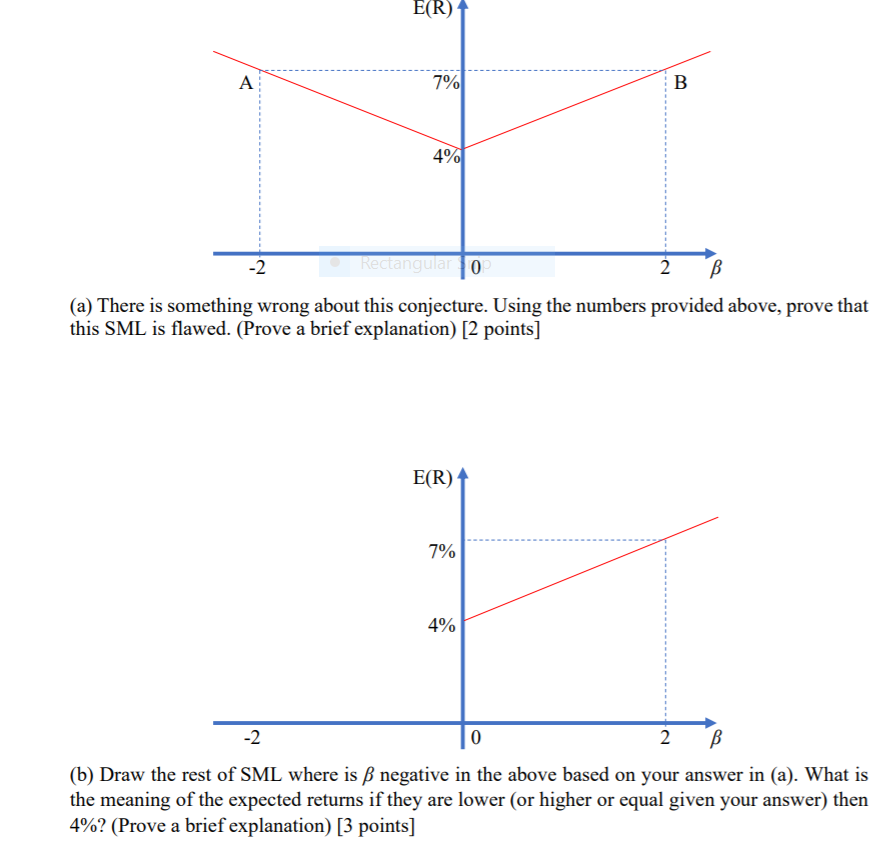

So far, we have been silent about expected returns of assets with negative beta. You conjecture that expected return must be positively correlated with absolute

So far, we have been silent about expected returns of assets with negative beta. You conjecture that expected return must be positively correlated with absolute value of beta. The following is an example of the modified SML based on this conjecture (Assume CAPM holds):

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Foundations Of Personal Finance

Authors: Sally R. Campbell, Robert L. Dansby

9th Edition

1619603578, 9781619603578