Answered step by step

Verified Expert Solution

Question

1 Approved Answer

solve for B with formula please for a Consider Commodity Z, which has both exchange-traded futures and optorn call prices associated with it. As you

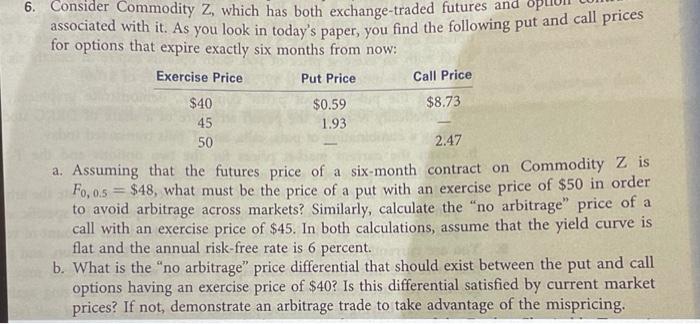

solve for B with formula please for a  Consider Commodity Z, which has both exchange-traded futures and optorn call prices associated with it. As you look in today's paper, you find for options that expire exactly six months from now: a. Assuming that the futures price of a six-month contract on Commodity Z is F0,0.5=$48, what must be the price of a put with an exercise price of $50 in order to avoid arbitrage across markets? Similarly, calculate the "no arbitrage" price of a call with an exercise price of $45. In both calculations, assume that the yield curve is flat and the annual risk-free rate is 6 percent. b. What is the "no arbitrage" price differential that should exist between the put and call options having an exercise price of $40 ? Is this differential satisfied by current market prices? If not, demonstrate an arbitrage trade to take advantage of the mispricing

Consider Commodity Z, which has both exchange-traded futures and optorn call prices associated with it. As you look in today's paper, you find for options that expire exactly six months from now: a. Assuming that the futures price of a six-month contract on Commodity Z is F0,0.5=$48, what must be the price of a put with an exercise price of $50 in order to avoid arbitrage across markets? Similarly, calculate the "no arbitrage" price of a call with an exercise price of $45. In both calculations, assume that the yield curve is flat and the annual risk-free rate is 6 percent. b. What is the "no arbitrage" price differential that should exist between the put and call options having an exercise price of $40 ? Is this differential satisfied by current market prices? If not, demonstrate an arbitrage trade to take advantage of the mispricing

with formula please for a

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Risk Modeling Evaluation Handbook Rethinking Financial Risk Management Methodologies In The Global Capital Markets

Authors: Greg Gregoriou, Christian Hoppe, Carsten Wehn

1st Edition

0071663703, 978-0071663700