Answered step by step

Verified Expert Solution

Question

1 Approved Answer

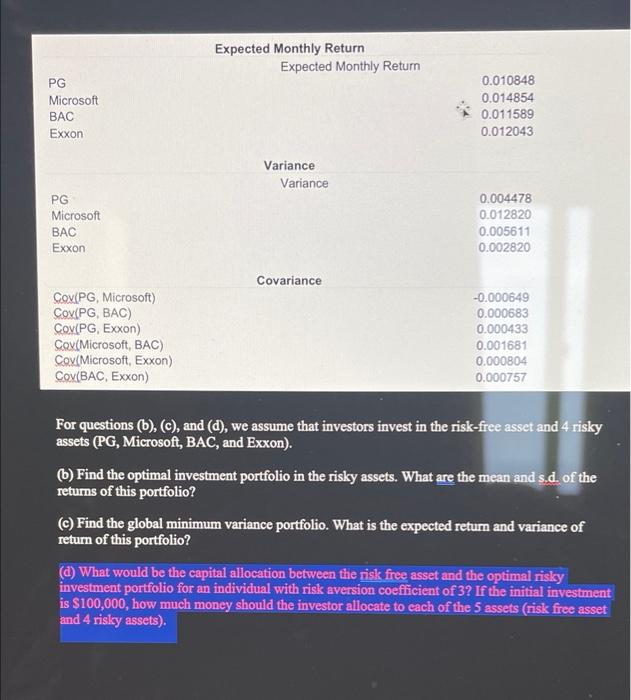

Solve for part D only. Also, please show your work/formulas in excel and thank you. Expected Monthly Return Expected Monthly Return PG Microsoft BAC Exxon

Solve for part D only. Also, please show your work/formulas in excel and thank you.

Expected Monthly Return Expected Monthly Return PG Microsoft BAC Exxon 0.010848 0.014854 0.011589 0.012043 Variance Variance PG Microsoft BAC Exxon 0.004478 0.012820 0.005611 0.002820 Covariance COX(PG, Microsoft) Cox(PG, BAC) Cov(PG, Exxon Cox(Microsoft, BAC) Cox(Microsoft Exxon) COX BAC, Exxon) -0.000649 0.000683 0.000433 0.001681 0.000804 0.000757 For questions (b), (c), and (d), we assume that investors invest in the risk-free asset and 4 risky assets (PG, Microsoft, BAC, and Exxon). (6) Find the optimal investment portfolio in the risky assets. What are the mean and s.d. of the returns of this portfolio? (c) Find the global minimum variance portfolio. What is the expected return and variance of return of this portfolio? (d) What would be the capital allocation between the risk free asset and the optimal risky investment portfolio for an individual with risk aversion coefficient of 3? If the initial investment is $100,000, how much money should the investor allocate to each of the 5 assets (risk free asset and 4 risky assets). Expected Monthly Return Expected Monthly Return PG Microsoft BAC Exxon 0.010848 0.014854 0.011589 0.012043 Variance Variance PG Microsoft BAC Exxon 0.004478 0.012820 0.005611 0.002820 Covariance COX(PG, Microsoft) Cox(PG, BAC) Cov(PG, Exxon Cox(Microsoft, BAC) Cox(Microsoft Exxon) COX BAC, Exxon) -0.000649 0.000683 0.000433 0.001681 0.000804 0.000757 For questions (b), (c), and (d), we assume that investors invest in the risk-free asset and 4 risky assets (PG, Microsoft, BAC, and Exxon). (6) Find the optimal investment portfolio in the risky assets. What are the mean and s.d. of the returns of this portfolio? (c) Find the global minimum variance portfolio. What is the expected return and variance of return of this portfolio? (d) What would be the capital allocation between the risk free asset and the optimal risky investment portfolio for an individual with risk aversion coefficient of 3? If the initial investment is $100,000, how much money should the investor allocate to each of the 5 assets (risk free asset and 4 risky assets) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Crypto Asset Investing In The Age Of Autonomy

Authors: Jake Ryan

1st Edition

1119705363, 978-1119705369