Answered step by step

Verified Expert Solution

Question

1 Approved Answer

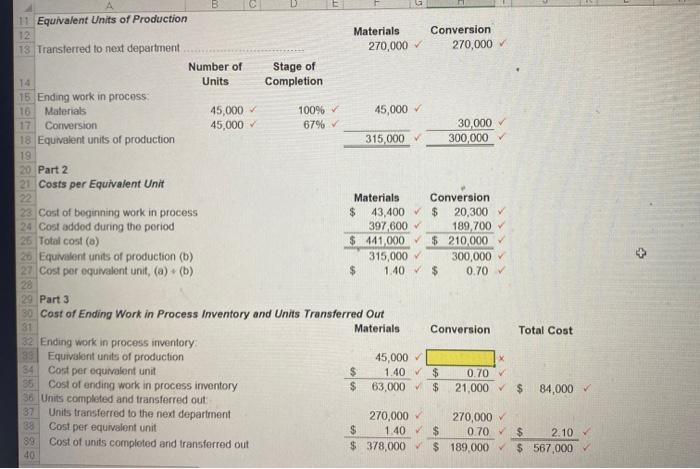

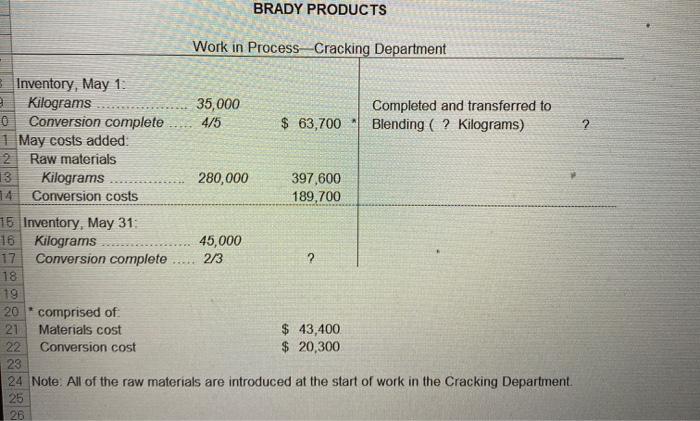

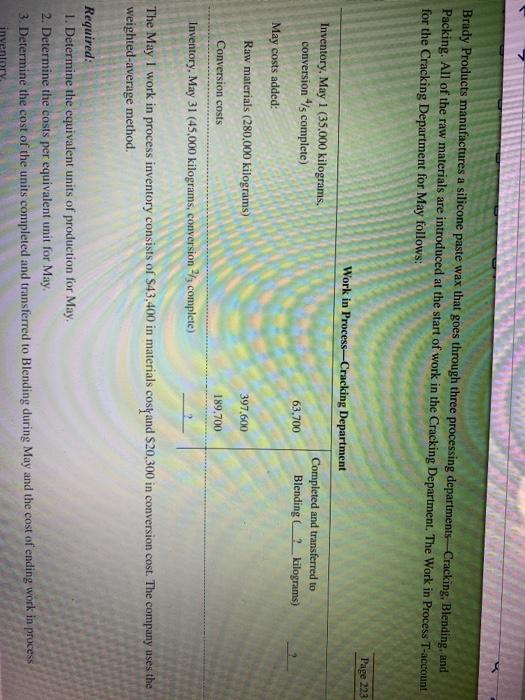

solve for the yellow square as well as part 4 Q: what critisicism can be made of the unit costs that you have computed if

solve for the yellow square as well as part 4 Q: what critisicism can be made of the unit costs that you have computed if they are used to evaulate how well costs have been controlled?

i found the missing answer. the only thing i need is the answer for Part 4

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Advanced Financial Accounting

Authors: Richard E. Baker, Valdean C. Lembke, Thomas E. King

5th Edition

0072444126, 978-0072444124