Answered step by step

Verified Expert Solution

Question

1 Approved Answer

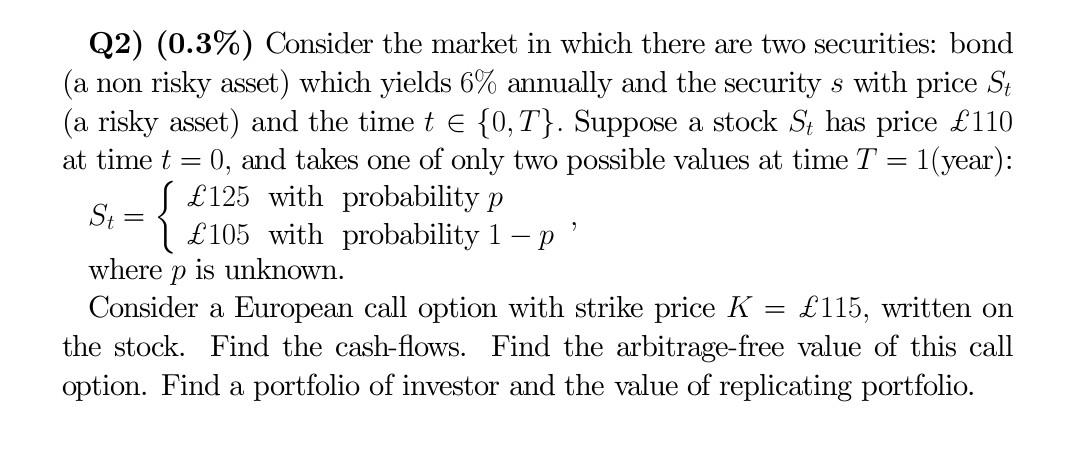

solve in 50 mins i will give thumb up. Q2) (0.3% ) Consider the market in which there are two securities: bond (a non risky

solve in 50 mins i will give thumb up.

Q2) (0.3% ) Consider the market in which there are two securities: bond (a non risky asset) which yields 6% annually and the security s with price St (a risky asset) and the time t{0,T}. Suppose a stock St has price 110 at time t=0, and takes one of only two possible values at time T=1 (year): St={125withprobabilityp105withprobability1p, where p is unknown. Consider a European call option with strike price K=115, written on the stock. Find the cash-flows. Find the arbitrage-free value of this call option. Find a portfolio of investor and the value of replicating portfolioStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Short Term Financial Management

Authors: Terry S. Maness, John T. Zietlow

2nd Edition

0030315131, 978-0030315138