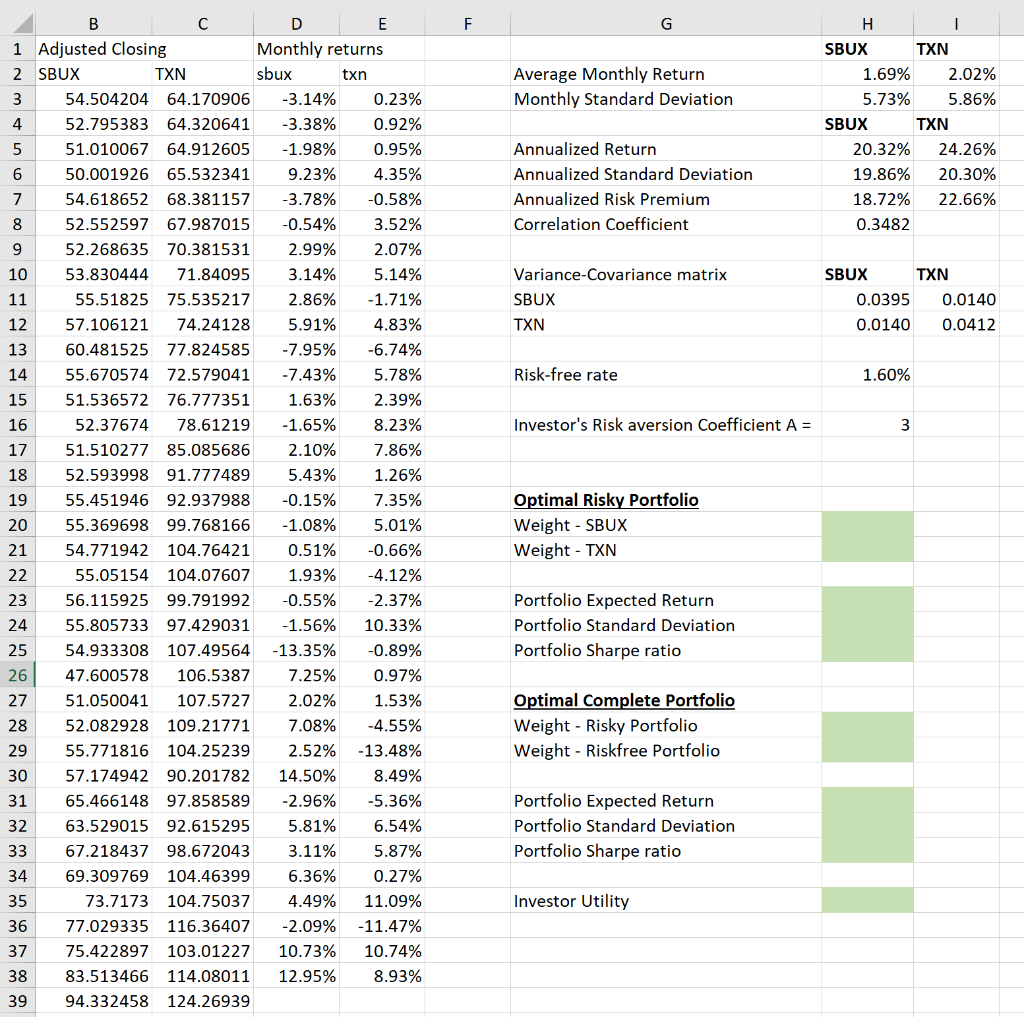

Solve Optimal Risky Portfolio and Optimal Complete Portfolio- Green Fields. Show Formulas

- Find the appropriate weights for the "optimal risky portfolio", which maximize the Sharpe ratio of the portfolio, based on the two stocks you choose. Also, calculate the portfolio expected returns and standard deviation (and Sharpe ratio).

- Find the appropriate weights for the "optimal complete portfolio", which is formed by allocating your funds between optimal risky portfolio formed in Step 6 and the risk-free asset. Also, calculate the portfolio expected returns, standard deviation, Sharpe ratio and investor's utility.

F Average Monthly Return Monthly Standard Deviation 3 SBUX 1.69% 5.73% SBUX 20.32% 19.86% 18.72% 0.3482 TXN 2.02% 5.86% TXN 24.26% 20.30% 22.66% Annualized Return Annualized Standard Deviation Annualized Risk Premium Correlation Coefficient Variance-Covariance matrix SBUX TXN SBUX TXN 0.0395 0.0140 0.0140 0.0412 Risk-free rate 1.60% Investor's Risk aversion Coefficient A = D E 1 Adjusted Closing Monthly returns 2 SBUX TXN Sbux txn 54.504204 64.170906 -3.14% 0.23% 52.795383 64.320641 -3.38% 0.92% 51.010067 64.912605 -1.98% 0.95% 50.001926 65.532341 9.23% 4.35% 54.618652 68.381157 -3.78% -0.58% 52.552597 67.987015 -0.54% 3.52% 52.268635 70.381531 2.99% 2.07% 53.830444 71.84095 3.14% 5.14% 55.51825 75.535217 2.86% -1.71% 57.106121 74.24128 5.91% 4.83% 60.481525 77.824585 -7.95% -6.74% 55.670574 72.579041 -7.43% 5.78% 51.536572 76.777351 1.63% 2.39% 52.37674 78.61219 -1.65% 8.23% 51.510277 85.085686 2.10% 7.86% 52.593998 91.777489 5.43% 1.26% 55.451946 92.937988 -0.15% 7.35% 55.369698 99.768166 -1.08% 5.01% 21 54.771942 104.76421 0.51% -0.66% 55.05154 104.07607 1.93% -4.12% 23 56.115925 99.791992 -0.55% -2.37% 55.805733 97.429031 -1.56% 10.33% 25 54.933308 107.49564 -13.35% -0.89% 26 47.600578 106.5387 7.25% 0.97% 51.050041 107.5727 2.02% 1.53% 28 52.082928 109.21771 7.08% -4.55% 55.771816 104.25239 2.52% -13.48% 57.174942 90.201782 14.50% 8.49% 65.466148 97.858589 -2.96% -5.36% 32 63.529015 92.615295 5.81% 6.54% 33 67.218437 98.672043 3.11% 5.87% 34 69.309769 104.46399 6.36% 0.27% 73.7173 104.75037 4.49% 11.09% 36 77.029335 116.36407 -2.09% -11.47% 75.422897 103.01227 10.73% 10.74% 38 83.513466 114.08011 12.95% 8.93% 94.332458 124.26939 Optimal Risky Portfolio Weight - SBUX Weight - TXN 22 Portfolio Expected Return Portfolio Standard Deviation Portfolio Sharpe ratio Optimal Complete Portfolio Weight - Risky Portfolio Weight - Riskfree Portfolio 31 Portfolio Expected Return Portfolio Standard Deviation Portfolio Sharpe ratio 35 Investor Utility 39 F Average Monthly Return Monthly Standard Deviation 3 SBUX 1.69% 5.73% SBUX 20.32% 19.86% 18.72% 0.3482 TXN 2.02% 5.86% TXN 24.26% 20.30% 22.66% Annualized Return Annualized Standard Deviation Annualized Risk Premium Correlation Coefficient Variance-Covariance matrix SBUX TXN SBUX TXN 0.0395 0.0140 0.0140 0.0412 Risk-free rate 1.60% Investor's Risk aversion Coefficient A = D E 1 Adjusted Closing Monthly returns 2 SBUX TXN Sbux txn 54.504204 64.170906 -3.14% 0.23% 52.795383 64.320641 -3.38% 0.92% 51.010067 64.912605 -1.98% 0.95% 50.001926 65.532341 9.23% 4.35% 54.618652 68.381157 -3.78% -0.58% 52.552597 67.987015 -0.54% 3.52% 52.268635 70.381531 2.99% 2.07% 53.830444 71.84095 3.14% 5.14% 55.51825 75.535217 2.86% -1.71% 57.106121 74.24128 5.91% 4.83% 60.481525 77.824585 -7.95% -6.74% 55.670574 72.579041 -7.43% 5.78% 51.536572 76.777351 1.63% 2.39% 52.37674 78.61219 -1.65% 8.23% 51.510277 85.085686 2.10% 7.86% 52.593998 91.777489 5.43% 1.26% 55.451946 92.937988 -0.15% 7.35% 55.369698 99.768166 -1.08% 5.01% 21 54.771942 104.76421 0.51% -0.66% 55.05154 104.07607 1.93% -4.12% 23 56.115925 99.791992 -0.55% -2.37% 55.805733 97.429031 -1.56% 10.33% 25 54.933308 107.49564 -13.35% -0.89% 26 47.600578 106.5387 7.25% 0.97% 51.050041 107.5727 2.02% 1.53% 28 52.082928 109.21771 7.08% -4.55% 55.771816 104.25239 2.52% -13.48% 57.174942 90.201782 14.50% 8.49% 65.466148 97.858589 -2.96% -5.36% 32 63.529015 92.615295 5.81% 6.54% 33 67.218437 98.672043 3.11% 5.87% 34 69.309769 104.46399 6.36% 0.27% 73.7173 104.75037 4.49% 11.09% 36 77.029335 116.36407 -2.09% -11.47% 75.422897 103.01227 10.73% 10.74% 38 83.513466 114.08011 12.95% 8.93% 94.332458 124.26939 Optimal Risky Portfolio Weight - SBUX Weight - TXN 22 Portfolio Expected Return Portfolio Standard Deviation Portfolio Sharpe ratio Optimal Complete Portfolio Weight - Risky Portfolio Weight - Riskfree Portfolio 31 Portfolio Expected Return Portfolio Standard Deviation Portfolio Sharpe ratio 35 Investor Utility 39