Answered step by step

Verified Expert Solution

Question

1 Approved Answer

solve part A & B of this question on PAPER as soon as possible. URGENT HELP REQUIRED. i'll surely give u Thumbs up. Natet Mode

solve part A & B of this question on PAPER as soon as possible. URGENT HELP REQUIRED. i'll surely give u Thumbs up.

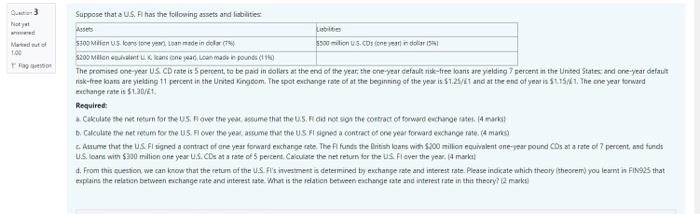

Natet Mode 1.00 Suppose that a U.S. has the following assets and liabilities Assets Lubbe 5300 Mile us on one year Loansdeinde 500 milions. CDs one year in dolara 5200 Milioni kan one year an made in pounds (10 The promises one-year US CD rate is 5 percent, to be paid in dollars at the end of the year, the one year defaultnisk-free loans are yielding 7 percent in the United States and one-year default nisk-free loans are yielding 11 percent in the United Kingdom. The spot exchange rate of at the beginning of the year is $1.25/1 and at the end of year is SUSA. The one year forward change rate is $1.30/1 Required Culate the return for the US over the yer assume that the us did not on the contract of forwardedige stes (4) B. Calculate the net retum for the US. Fl over the year assume that the USF signed a contract of one year forward exchange rate. (A manice Aanume that the US.FI signed a contract of one year forward exchange cebe. The Pfunds the litish loans with $200 milion equivalent one-year pound CDs at a rate of 7 percent, and funch U.S.loans with $300 million one year us.CDs at a rate of 5 percent Calculate the net return for the US Flover the year. (4 markal d. From this cuestion we can know that the return of the USA's investment is determined by exchange rate and interest rate. Please indicate which theory there you learnt in FIN925 that explains the relation between change rate and interest sate. What is the relation between exchange rate and interest rate in this theory? 12 marks Natet Mode 1.00 Suppose that a U.S. has the following assets and liabilities Assets Lubbe 5300 Mile us on one year Loansdeinde 500 milions. CDs one year in dolara 5200 Milioni kan one year an made in pounds (10 The promises one-year US CD rate is 5 percent, to be paid in dollars at the end of the year, the one year defaultnisk-free loans are yielding 7 percent in the United States and one-year default nisk-free loans are yielding 11 percent in the United Kingdom. The spot exchange rate of at the beginning of the year is $1.25/1 and at the end of year is SUSA. The one year forward change rate is $1.30/1 Required Culate the return for the US over the yer assume that the us did not on the contract of forwardedige stes (4) B. Calculate the net retum for the US. Fl over the year assume that the USF signed a contract of one year forward exchange rate. (A manice Aanume that the US.FI signed a contract of one year forward exchange cebe. The Pfunds the litish loans with $200 milion equivalent one-year pound CDs at a rate of 7 percent, and funch U.S.loans with $300 million one year us.CDs at a rate of 5 percent Calculate the net return for the US Flover the year. (4 markal d. From this cuestion we can know that the return of the USA's investment is determined by exchange rate and interest rate. Please indicate which theory there you learnt in FIN925 that explains the relation between change rate and interest sate. What is the relation between exchange rate and interest rate in this theory? 12 marks Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Supernatural Provision Living In Financial Freedom

Authors: Joan Hunter, Sid Roth

1st Edition

1641238232, 978-1641238236