Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Solve the following 3 questions with explanations please. Required: Using the IMA's Statement of Ethical Professional Practice provided, answer the following questions, making sure to

Solve the following 3 questions with explanations please.

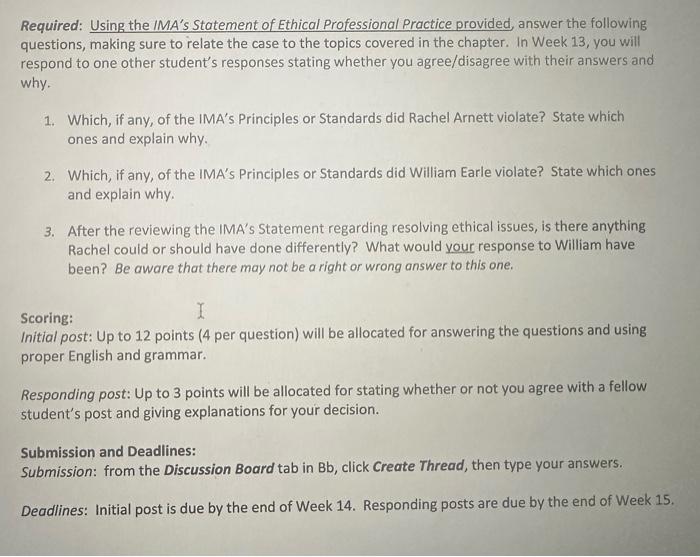

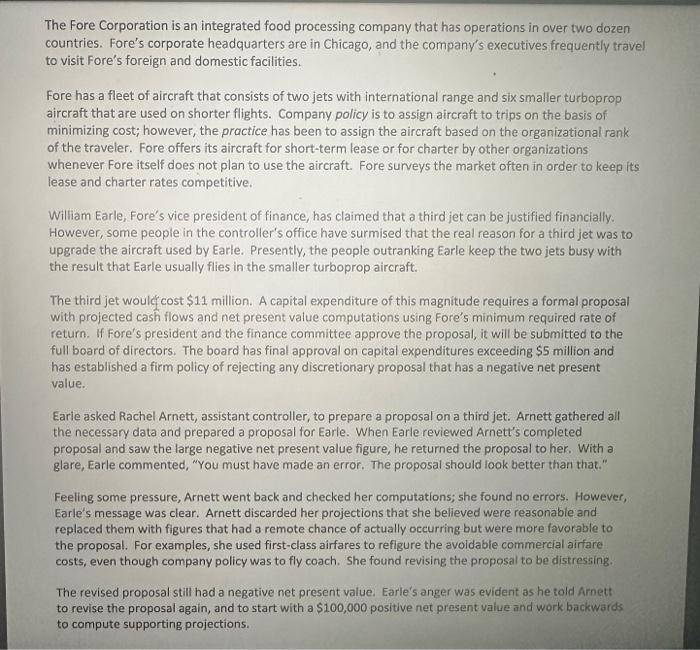

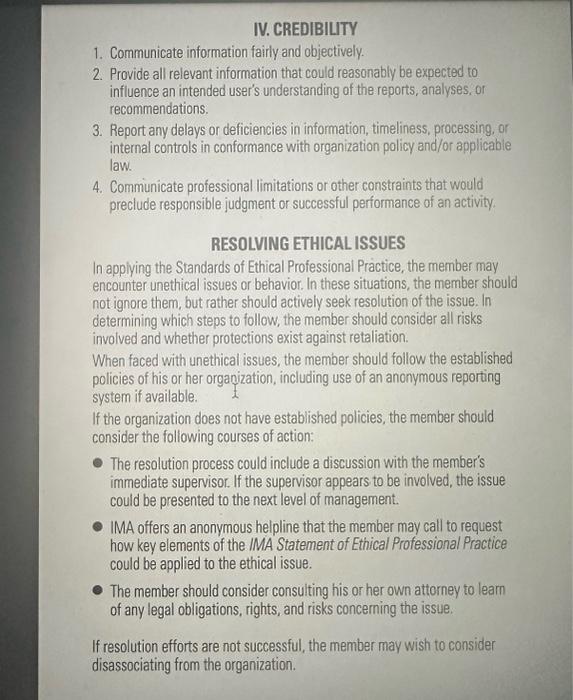

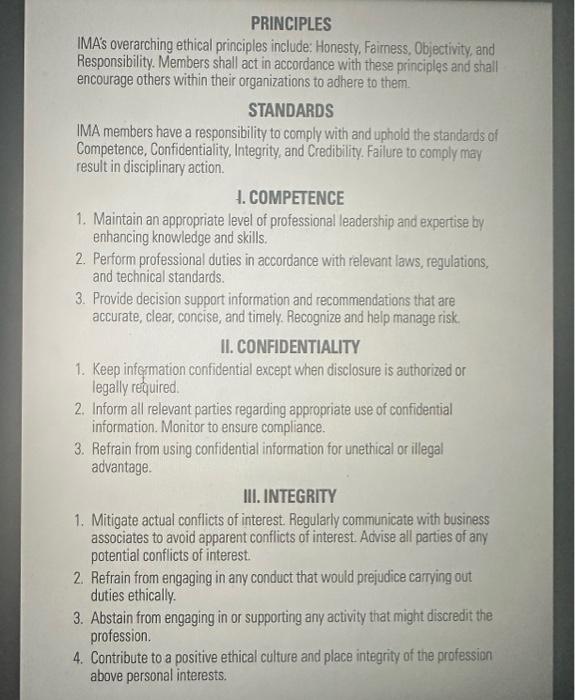

Required: Using the IMA's Statement of Ethical Professional Practice provided, answer the following questions, making sure to relate the case to the topics covered in the chapter. In Week 13 , you will respond to one other student's responses stating whether you agree/disagree with their answers and why. 1. Which, if any, of the IMA's Principles or Standards did Rachel Arnett violate? State which ones and explain why. 2. Which, if any, of the IMA's Principles or Standards did William Earle violate? State which ones and explain why. 3. After the reviewing the IMA's Statement regarding resolving ethical issues, is there anything Rachel could or should have done differently? What would your response to William have been? Be aware that there may not be a right or wrong answer to this one. Scoring: Initial post: Up to 12 points (4 per question) will be allocated for answering the questions and using proper English and grammar. Responding post: Up to 3 points will be allocated for stating whether or not you agree with a fellow student's post and giving explanations for your decision. Submission and Deadlines: Submission: from the Discussion Board tab in Bb, click Create Thread, then type your answers. Deadlines: Initial post is due by the end of Week 14. Responding posts are due by the end of Week 15. The Fore Corporation is an integrated food processing company that has operations in over two dozen countries. Fore's corporate headquarters are in Chicago, and the company's executives frequently travel to visit Fore's foreign and domestic facilities. Fore has a fleet of aircraft that consists of two jets with international range and six smaller turboprop aircraft that are used on shorter flights. Company policy is to assign aircraft to trips on the basis of minimizing cost; however, the practice has been to assign the aircraft based on the organizational rank of the traveler. Fore offers its aircraft for short-term lease or for charter by other organizations whenever Fore itself does not plan to use the aircraft. Fore surveys the market often in order to keep its lease and charter rates competitive. William Earle, Fore's vice president of finance, has claimed that a third jet can be justified financially. However, some people in the controller's office have surmised that the real reason for a third jet was to upgrade the aircraft used by Earle. Presently, the people outranking Earle keep the two jets busy with the result that Earle usually flies in the smaller turboprop aircraft. The third jet woulc cost $11 million. A capital expenditure of this magnitude requires a formal proposal with projected cash flows and net present value computations using fore's minimum required rate of return. If Fore's president and the finance committee approve the proposal, it will be submitted to the full board of directors. The board has final approval on capital expenditures exceeding $5 million and has established a firm policy of rejecting any discretionary proposal that has a negative net present value. Earie asked Rachel Arnett, assistant controller, to prepare a proposal on a third jet. Arnett gathered all the necessary data and prepared a proposal for Earle. When Earle reviewed Arnett's completed proposal and saw the large negative net present value figure, he returned the proposal to her. With a glare, Earle commented, "You must have made an error. The proposal should look better than that." Feeling some pressure, Arnett went back and checked her computations; she found no errors. However, Earle's message was clear. Arnett discarded her projections that she believed were reasonable and replaced them with figures that had a remote chance of actually occurring but were more favorable to the proposal. For examples, she used first-class airfares to refigure the avoidable commercial airfare costs, even though company policy was to fly coach. She found revising the proposal to be distressing. The revised proposal still had a negative net present value. Earle's anger was evident as he told Arnett to revise the proposal again, and to start with a $100,000 positive net present value and work backwards to compute supporting projections. IV. CREDIBILITY 1. Communicate information fairly and objectively. 2. Provide all relevant information that could reasonably be expected to influence an intended user's understanding of the reports, analyses, or recommendations. 3. Report any delays or deficiencies in information, timeliness, processing, or internal controls in conformance with organization policy and/or applicable law. 4. Communicate professional limitations or other constraints that would preclude responsible judgment or successful performance of an activity. RESOLVING ETHICAL ISSUES In applying the Standards of Ethical Professional Practice, the member may encounter unethical issues or behavior. In these situations, the member should not ignore them, but rather should actively seek resolution of the issue. In determining which steps to follow, the member should consider all risks involved and whether protections exist against retaliation. When faced with unethical issues, the member should follow the established policies of his or her organization, including use of an anonymous reporting system if available. If the organization does not have established policies, the member should consider the following courses of action: The resolution process could include a discussion with the member's immediate supervisor. If the supervisor appears to be involved, the issue could be presented to the next level of management. IMA offers an anonymous helpline that the member may call to request how key elements of the IMA Statement of Ethical Professional Practice could be applied to the ethical issue. The member should consider consulting his or her own attorney to learn of any legal obligations, rights, and risks concerning the issue. If resolution efforts are not successful, the member may wish to consider disassociating from the organization. PRINCIPLES IMA's overarching ethical principles include: Honesty, Faimess, Objectivity, and Responsibility. Members shall act in accordance with these principles and shall encourage others within their organizations to adhere to them. STANDARDS IMA members have a responsibility to comply with and uphoid the standards of Competence, Confidentiality, Integrity, and Credibility. Failure to comply may result in disciplinary action. 1. COMPETENCE 1. Maintain an appropriate level of professional leadership and expertise by enhancing knowledge and skills. 2. Perform professional duties in accordance with relevant laws, regulations, and technical standards. 3. Provide decision support information and recommendations that are accurate, clear, concise, and timely. Recognize and help manage risk. II. CONFIDENTIALITY 1. Keep infemmation confidential except when disclosure is authorized or legally required. 2. Inform all relevant parties regarding appropriate use of confidential information. Monitor to ensure compliance. 3. Refrain from using confidential information for unethical or illegal advantage. III. INTEGRITY 1. Mitigate actual conflicts of interest. Regularly communicate with business associates to avoid apparent conflicts of interest. Advise all parties of any potential conflicts of interest. 2. Refrain from engaging in any conduct that would prejudice carrying out duties ethically. 3. Abstain from engaging in or supporting any activity that might discredit the profession. 4. Contribute to a positive ethical culture and place integrity of the profession above personal interests. Required: Using the IMA's Statement of Ethical Professional Practice provided, answer the following questions, making sure to relate the case to the topics covered in the chapter. In Week 13 , you will respond to one other student's responses stating whether you agree/disagree with their answers and why. 1. Which, if any, of the IMA's Principles or Standards did Rachel Arnett violate? State which ones and explain why. 2. Which, if any, of the IMA's Principles or Standards did William Earle violate? State which ones and explain why. 3. After the reviewing the IMA's Statement regarding resolving ethical issues, is there anything Rachel could or should have done differently? What would your response to William have been? Be aware that there may not be a right or wrong answer to this one. Scoring: Initial post: Up to 12 points (4 per question) will be allocated for answering the questions and using proper English and grammar. Responding post: Up to 3 points will be allocated for stating whether or not you agree with a fellow student's post and giving explanations for your decision. Submission and Deadlines: Submission: from the Discussion Board tab in Bb, click Create Thread, then type your answers. Deadlines: Initial post is due by the end of Week 14. Responding posts are due by the end of Week 15. The Fore Corporation is an integrated food processing company that has operations in over two dozen countries. Fore's corporate headquarters are in Chicago, and the company's executives frequently travel to visit Fore's foreign and domestic facilities. Fore has a fleet of aircraft that consists of two jets with international range and six smaller turboprop aircraft that are used on shorter flights. Company policy is to assign aircraft to trips on the basis of minimizing cost; however, the practice has been to assign the aircraft based on the organizational rank of the traveler. Fore offers its aircraft for short-term lease or for charter by other organizations whenever Fore itself does not plan to use the aircraft. Fore surveys the market often in order to keep its lease and charter rates competitive. William Earle, Fore's vice president of finance, has claimed that a third jet can be justified financially. However, some people in the controller's office have surmised that the real reason for a third jet was to upgrade the aircraft used by Earle. Presently, the people outranking Earle keep the two jets busy with the result that Earle usually flies in the smaller turboprop aircraft. The third jet woulc cost $11 million. A capital expenditure of this magnitude requires a formal proposal with projected cash flows and net present value computations using fore's minimum required rate of return. If Fore's president and the finance committee approve the proposal, it will be submitted to the full board of directors. The board has final approval on capital expenditures exceeding $5 million and has established a firm policy of rejecting any discretionary proposal that has a negative net present value. Earie asked Rachel Arnett, assistant controller, to prepare a proposal on a third jet. Arnett gathered all the necessary data and prepared a proposal for Earle. When Earle reviewed Arnett's completed proposal and saw the large negative net present value figure, he returned the proposal to her. With a glare, Earle commented, "You must have made an error. The proposal should look better than that." Feeling some pressure, Arnett went back and checked her computations; she found no errors. However, Earle's message was clear. Arnett discarded her projections that she believed were reasonable and replaced them with figures that had a remote chance of actually occurring but were more favorable to the proposal. For examples, she used first-class airfares to refigure the avoidable commercial airfare costs, even though company policy was to fly coach. She found revising the proposal to be distressing. The revised proposal still had a negative net present value. Earle's anger was evident as he told Arnett to revise the proposal again, and to start with a $100,000 positive net present value and work backwards to compute supporting projections. IV. CREDIBILITY 1. Communicate information fairly and objectively. 2. Provide all relevant information that could reasonably be expected to influence an intended user's understanding of the reports, analyses, or recommendations. 3. Report any delays or deficiencies in information, timeliness, processing, or internal controls in conformance with organization policy and/or applicable law. 4. Communicate professional limitations or other constraints that would preclude responsible judgment or successful performance of an activity. RESOLVING ETHICAL ISSUES In applying the Standards of Ethical Professional Practice, the member may encounter unethical issues or behavior. In these situations, the member should not ignore them, but rather should actively seek resolution of the issue. In determining which steps to follow, the member should consider all risks involved and whether protections exist against retaliation. When faced with unethical issues, the member should follow the established policies of his or her organization, including use of an anonymous reporting system if available. If the organization does not have established policies, the member should consider the following courses of action: The resolution process could include a discussion with the member's immediate supervisor. If the supervisor appears to be involved, the issue could be presented to the next level of management. IMA offers an anonymous helpline that the member may call to request how key elements of the IMA Statement of Ethical Professional Practice could be applied to the ethical issue. The member should consider consulting his or her own attorney to learn of any legal obligations, rights, and risks concerning the issue. If resolution efforts are not successful, the member may wish to consider disassociating from the organization. PRINCIPLES IMA's overarching ethical principles include: Honesty, Faimess, Objectivity, and Responsibility. Members shall act in accordance with these principles and shall encourage others within their organizations to adhere to them. STANDARDS IMA members have a responsibility to comply with and uphoid the standards of Competence, Confidentiality, Integrity, and Credibility. Failure to comply may result in disciplinary action. 1. COMPETENCE 1. Maintain an appropriate level of professional leadership and expertise by enhancing knowledge and skills. 2. Perform professional duties in accordance with relevant laws, regulations, and technical standards. 3. Provide decision support information and recommendations that are accurate, clear, concise, and timely. Recognize and help manage risk. II. CONFIDENTIALITY 1. Keep infemmation confidential except when disclosure is authorized or legally required. 2. Inform all relevant parties regarding appropriate use of confidential information. Monitor to ensure compliance. 3. Refrain from using confidential information for unethical or illegal advantage. III. INTEGRITY 1. Mitigate actual conflicts of interest. Regularly communicate with business associates to avoid apparent conflicts of interest. Advise all parties of any potential conflicts of interest. 2. Refrain from engaging in any conduct that would prejudice carrying out duties ethically. 3. Abstain from engaging in or supporting any activity that might discredit the profession. 4. Contribute to a positive ethical culture and place integrity of the profession above personal interests Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Successful Audit New Ways To Reduce Risk Exposure And Increase Efficiency

Authors: Felix Pomeranz

1st Edition

1556233914, 978-1556233913