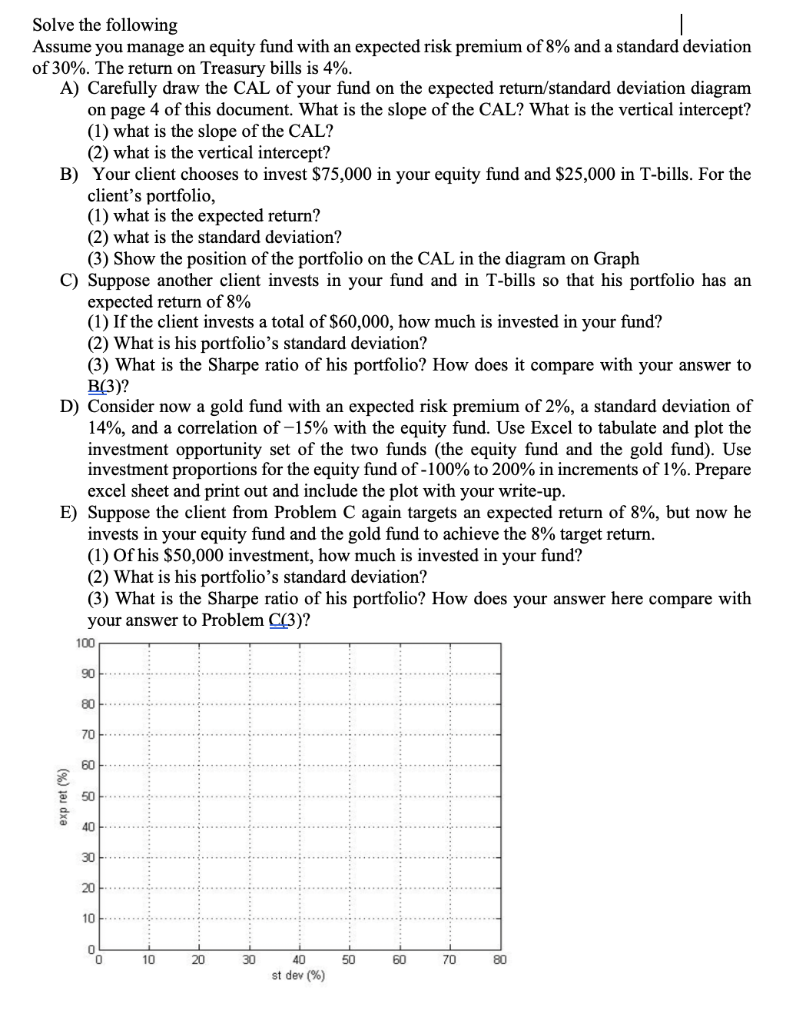

Solve the following Assume you manage an equity fund with an expected risk premium of 8% and a standard deviation of 30%. The return on Treasury bills is 4%. A) Carefully draw the CAL of your fund on the expected return/standard deviation diagram on page 4 of this document. What is the slope of the CAL? What is the vertical intercept? (1) what is the slope of the CAL? (2) what is the vertical intercept? B) Your client chooses to invest $75,000 in your equity fund and $25,000 in T-bills. For the client's portfolio, (1) what is the expected return? (2) what is the standard deviation? (3) Show the position of the portfolio on the CAL in the diagram on Graph C) Suppose another client invests in your fund and in T-bills so that his portfolio has an expected return of 8% (1) If the client invests a total of $60,000, how much is invested in your fund? (2) What is his portfolio's standard deviation? (3) What is the Sharpe ratio of his portfolio? How does it compare with your answer to B(3)? D) Consider now a gold fund with an expected risk premium of 2%, a standard deviation of 14%, and a correlation of -15% with the equity fund. Use Excel to tabulate and plot the investment opportunity set of the two funds (the equity fund and the gold fund). Use investment proportions for the equity fund of -100% to 200% in increments of 1%. Prepare excel sheet and print out and include the plot with your write-up. E) Suppose the client from Problem C again targets an expected return of 8%, but now he invests in your equity fund and the gold fund to achieve the 8% target return. (1) Of his $50,000 investment, how much is invested in your fund? (2) What is his portfolio's standard deviation? (3) What is the Sharpe ratio of his portfolio? How does your answer here compare with your answer to Problem C(3)? 100 90 80 70 60 (%) 10 dxe 50 40 30 20 10 0 10 20 30 50 60 70 80 40 st dev (%) Solve the following Assume you manage an equity fund with an expected risk premium of 8% and a standard deviation of 30%. The return on Treasury bills is 4%. A) Carefully draw the CAL of your fund on the expected return/standard deviation diagram on page 4 of this document. What is the slope of the CAL? What is the vertical intercept? (1) what is the slope of the CAL? (2) what is the vertical intercept? B) Your client chooses to invest $75,000 in your equity fund and $25,000 in T-bills. For the client's portfolio, (1) what is the expected return? (2) what is the standard deviation? (3) Show the position of the portfolio on the CAL in the diagram on Graph C) Suppose another client invests in your fund and in T-bills so that his portfolio has an expected return of 8% (1) If the client invests a total of $60,000, how much is invested in your fund? (2) What is his portfolio's standard deviation? (3) What is the Sharpe ratio of his portfolio? How does it compare with your answer to B(3)? D) Consider now a gold fund with an expected risk premium of 2%, a standard deviation of 14%, and a correlation of -15% with the equity fund. Use Excel to tabulate and plot the investment opportunity set of the two funds (the equity fund and the gold fund). Use investment proportions for the equity fund of -100% to 200% in increments of 1%. Prepare excel sheet and print out and include the plot with your write-up. E) Suppose the client from Problem C again targets an expected return of 8%, but now he invests in your equity fund and the gold fund to achieve the 8% target return. (1) Of his $50,000 investment, how much is invested in your fund? (2) What is his portfolio's standard deviation? (3) What is the Sharpe ratio of his portfolio? How does your answer here compare with your answer to Problem C(3)? 100 90 80 70 60 (%) 10 dxe 50 40 30 20 10 0 10 20 30 50 60 70 80 40 st dev (%)