Answered step by step

Verified Expert Solution

Question

1 Approved Answer

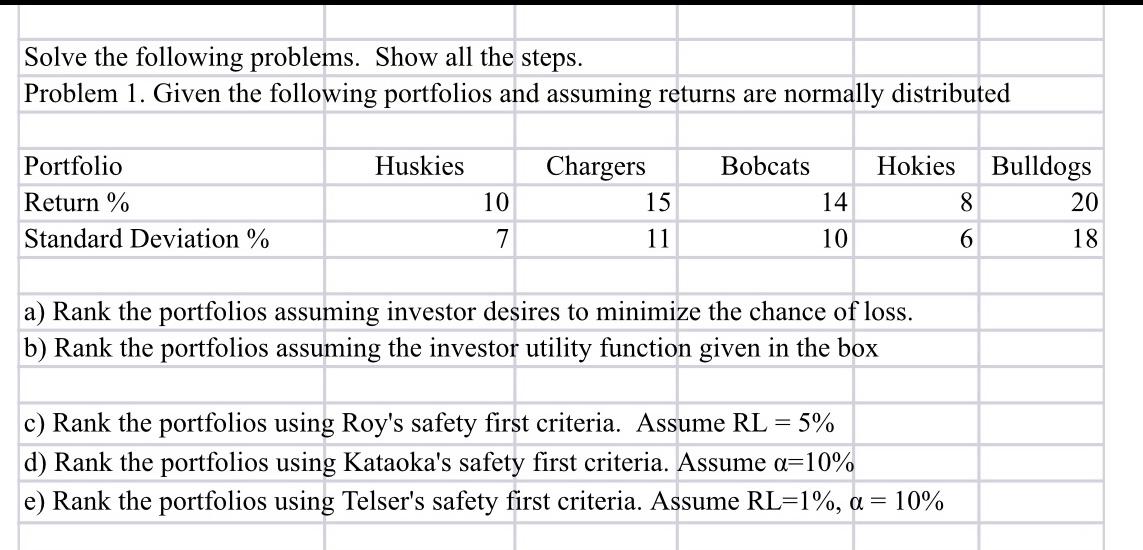

Solve the following problems. Show all the steps. Problem 1. Given the following portfolios and assuming returns are normally distributed begin{tabular}{|l|r|r|r|r|r|} hline Portfolio & Huskies

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Asset Allocation Strategies For Mutual Funds Evaluating Performance Risk And Return

Authors: Giuseppe Galloppo

1st Edition

3030761274,3030761282