Answered step by step

Verified Expert Solution

Question

1 Approved Answer

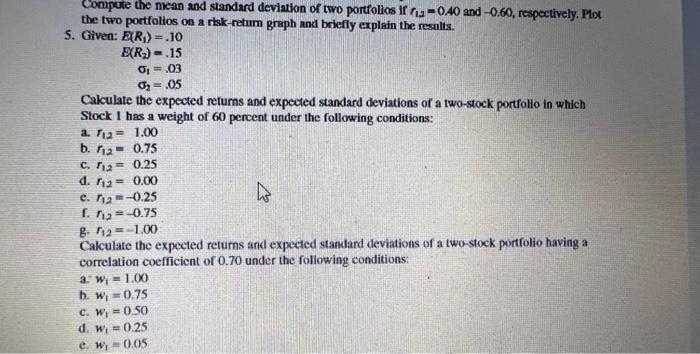

solve the following question its related to markovits portfolio. pls solve all parts else leave it. the two portfolios on a risk-retum graph and briefly

solve the following question its related to markovits portfolio. pls solve all parts else leave it.

the two portfolios on a risk-retum graph and briefly explain the results. 5. Given: E(R1)E(R2)12=.10=.15=.03=.05 Calculate the expected returns and expected standard deviations of a two-stock portfolio in which Stock 1 has a weight of 60 percent under the following conditions: a. r12=1.00 b. r12=0.75 c. r12=0.25 d. r12=0.00 e. r12=0.25 f. r12=0.75 g. r12=1.00 Calculate the expected returns and expected standard deviations of a two-stock portfolio having a correlation coefficient of 0.70 under the following conditions: a: w1=1.00 b. w1=0.75 c. w1=0.50 d. w1=0.25 e. w1=0.05

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Coping With Financial Accounting 1 For Senior Secondary Schools And Undergraduate Studies

Authors: Festus Chukwunwendu Akpotohwo ,Stella Alfred-Jaja Wellington-Igonibo ,Cletus Ogeibiri

1st Edition

3659611034, 978-3659611032