Answered step by step

Verified Expert Solution

Question

1 Approved Answer

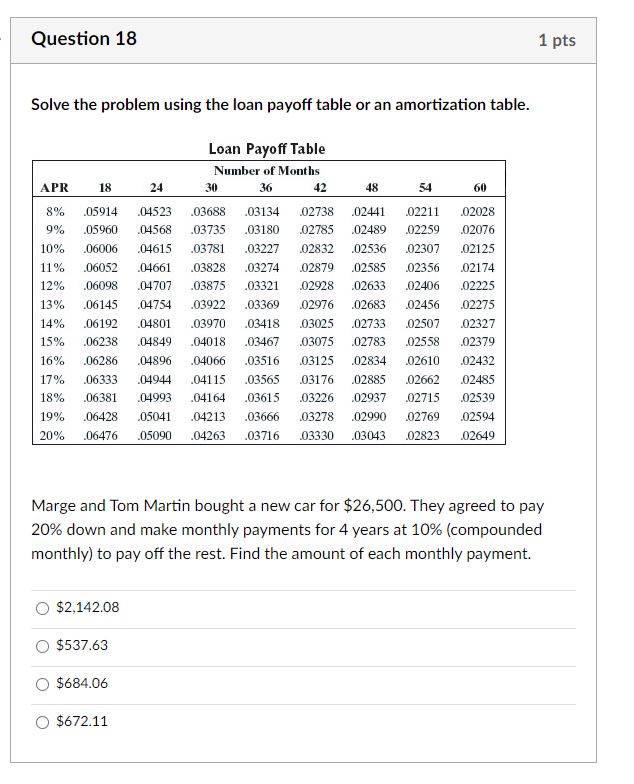

Solve the problem using the loan payoff table or an amortization table. Marge and Tom Martin bought a new car for $26,500. They agreed to

Solve the problem using the loan payoff table or an amortization table. Marge and Tom Martin bought a new car for $26,500. They agreed to pay 20% down and make monthly payments for 4 years at 10% (compounded monthly) to pay off the rest. Find the amount of each monthly payment. $2,142.08 $537.63 $684.06 $672.11

Solve the problem using the loan payoff table or an amortization table. Marge and Tom Martin bought a new car for $26,500. They agreed to pay 20% down and make monthly payments for 4 years at 10% (compounded monthly) to pay off the rest. Find the amount of each monthly payment. $2,142.08 $537.63 $684.06 $672.11 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Markets And Institutions

Authors: Anthony Saunders, Marcia Cornett

4th Edition

0077262379, 978-0077262372