Answered step by step

Verified Expert Solution

Question

1 Approved Answer

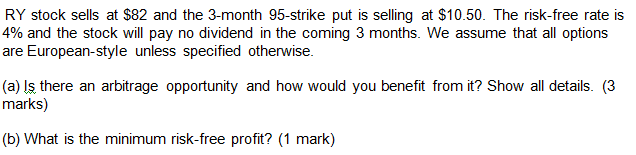

Someone please answer this financial derivatives problem. im really struggling with it RY stock sells at $82 and the 3-month 95-strike put is selling at

Someone please answer this financial derivatives problem. im really struggling with it

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Bitcoin Cash What You Need To Know About Bch

Authors: Alexander O. M.

1st Edition

1976721229, 978-1976721229