Space one: (a), (b), (c)

space two: a and b, a and c, b and c

space three: had actual indirect cost rates been used, had budgeted indirect cost rates been used, had the over- or understatement occurred in only the goods sold

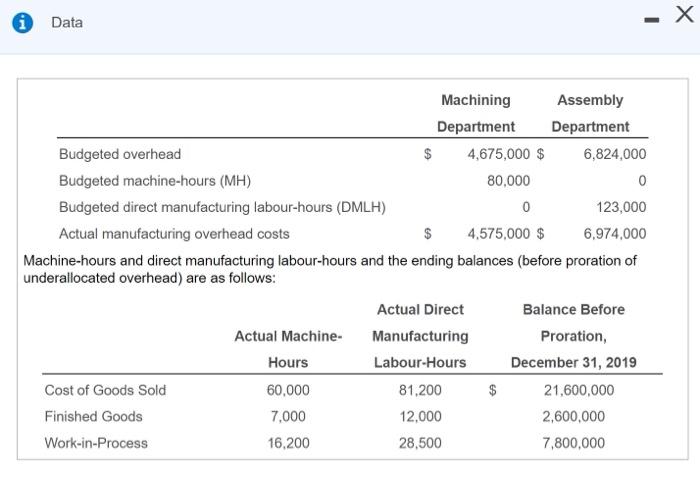

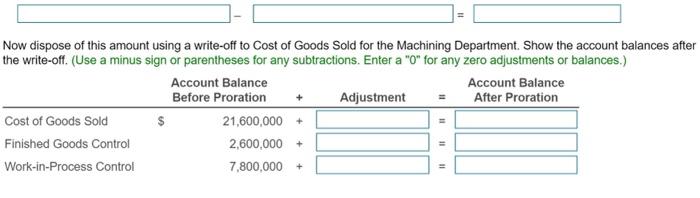

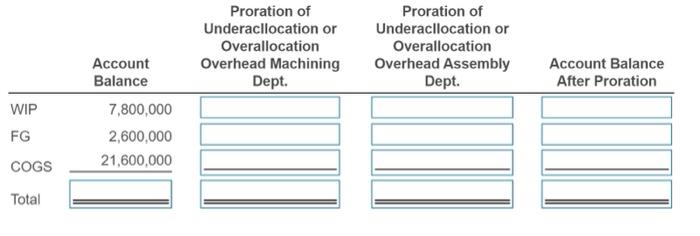

Data - X Machining Assembly Department Department Budgeted overhead $ 4,675,000 $ 6,824,000 Budgeted machine-hours (MH) 80,000 0 Budgeted direct manufacturing labour-hours (DMLH) 0 123,000 Actual manufacturing overhead costs $ 4,575,000 $ 6,974,000 Machine-hours and direct manufacturing labour-hours and the ending balances (before proration of underallocated overhead) are as follows: Actual Direct Balance Before Actual Machine- Manufacturing Proration, Hours Labour-Hours December 31, 2019 Cost of Goods Sold 60,000 81,200 $ 21,600,000 Finished Goods 7,000 12,000 2,600,000 Work-in-Process 16,200 28,500 7,800,000 Heat Corporation manufactures precision equipment made to order for the semiconductor industry, Heat uses two manufacturing overhead cost poolsone for the overhead costs incurred in its highly automated Machining Department and another for overhead costs incurred in its labour-based Assembly Department Heat uses a normal costing system. It allocates Machining Department overhead costs to jobs based on actual machine-hours using a budgeted machine-hour overhead rate. It allocates Assembly Department overhead costs to jobs based on actual direct manufacturing labour-hours using a budgeted direct manufacturing labour-hour rate. The following data are for the year 2019. (Click the icon to view the data.) Requirement 1. Compute the budgeted overhead rates for the year in the Machining and Assembly Departments. (Round your answers to the nearest whole dollar.) The budgeted overhead rate for the year in the Machining Department is $ The budgeted overhead rate for the year in the Assembly Department is s Requirement 2. Compute the under-or overallocated overhead in each department for the year. Dispose of the under-or overallocated amount in department using a. immediate write-off to Cost of Goods Sold; b. proration based on ending balances (before proration) in Cost of Goods Sold, Fi Goods, and Work-in-Process; and c. proration based on the allocated overhead amount (before proration) in the ending balances of Cost of Goods Finished Goods, and Work-in-process. We will begin with a. immediate write-off to Cost of Goods Sold. The first step is to find the over- or underallocated amounts for each department. Begin by selecting the formula and then enter the amounts for the Machining Department. (Indicate an overallocated amount using a minus sign.) Over- or underallocation Using the formula you determined above, compute the overallocated/underallocated amount for the Assembly Department + Now dispose of this amount using a write-off to Cost of Goods Sold for the Machining Department Show the account balances after the write-off. (Use a minus sign or parentheses for any subtractions. Enter a "0" for any zero adjustments or balances.) Account Balance Account Balance Before Proration Adjustment After Proration Cost of Goods Sold $ 21,600,000+ Finished Goods Control 2,600,000+ Work-in-Process Control 7,800,000+ 11 b. Compute the under- or overallocated overhead in each department for the year. Dispose of the unde each department using proration based on ending balances (before proration) in Cost of Goods Sold, Work-in-process. (When calculating the prorations, round the interim proration ratio to eight decimal pl answers to the nearest whole number. Use a minus sign or parentheses for any subtractions.) Proration of Underacllocation or Overallocation Overhead Machining Dept. Proration of Underacllocation or Overallocation Overhead Assembly Dept. Account Balance After Proration WIP Account Balance 7,800,000 2,600,000 21,600,000 FG COGS Total c. Compute the under-or overallocated overhead in each department for the year. Dispose of the under-or overallocated amount in each department using proration based on the allocated overhead amount (before proration) in the ending balances of Cost of Goods Sold, Finished Goods, and Work-in-Process. Start with the Machining Department. (Round the proportion to eight decimal places. Round all other amounts to the nearest whole number) Total Amount of Overallocated or Underallocated Overhead Proration of Underacllocation or Overallocation Overhead X Proportion WIP FG X COGS X Total Now complete for the Assembly Department. (Round the proportion to eight decimal places. Round all other amounts to the nearest whole number.) Total Amount of Proration of Overallocated or Underacllocation or Underallocated Overallocation Overhead * Proportion Overhead WIP FG X COGS Total Requirement 3. Which method do you prefer in requirement 2? Explain. Alternative is theoretically preferred over This alternative yields the same ending balances in Work-in-Process, Finished Goods, and Cost of Goods Sold that would have been reported