Speedy Motors assembles and sells motor vehicles and uses standard costing. Actual data and variable costing and absorption costing income statements relating The variable

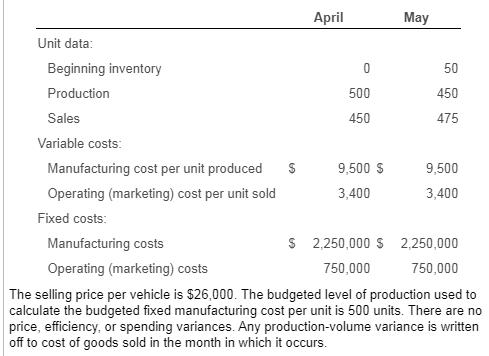

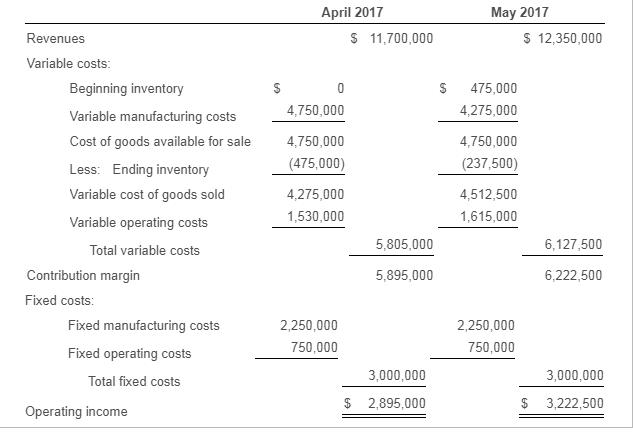

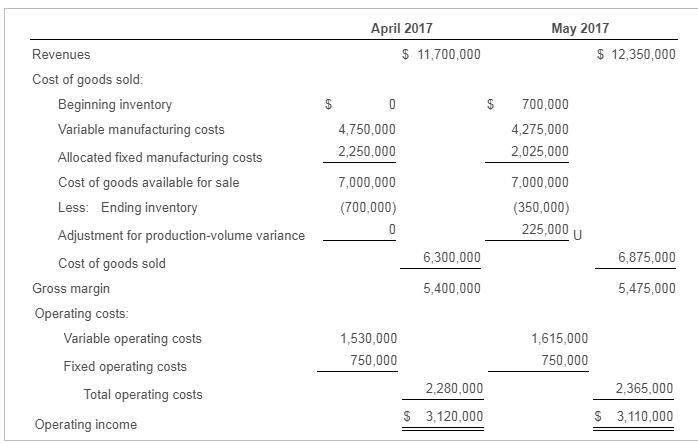

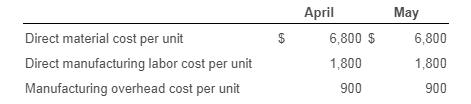

Speedy Motors assembles and sells motor vehicles and uses standard costing. Actual data and variable costing and absorption costing income statements relating The variable manufacturing costs per unit of Speedy Motors are as follows: to April and May 2017 are as follows: E: (Click the icon to view the variable manufacturing costs per unit.) Unit data: Beginning inventory Production Sales Variable costs: Manufacturing cost per unit produced Operating (marketing) cost per unit sold $ April 0 500 450 9,500 $ 3,400 May 50 450 475 9,500 3,400 Fixed costs: Manufacturing costs $ 2,250,000 $2,250,000 Operating (marketing) costs 750,000 750,000 The selling price per vehicle is $26,000. The budgeted level of production used to calculate the budgeted fixed manufacturing cost per unit is 500 units. There are no price, efficiency, or spending variances. Any production-volume variance is written off to cost of goods sold in the month in which it occurs. Revenues Variable costs: Beginning inventory Variable manufacturing costs Cost of goods available for sale Less: Ending inventory Variable cost of goods sold Variable operating costs Total variable costs Contribution margin Fixed costs: Fixed manufacturing costs Fixed operating costs Total fixed costs Operating income April 2017 4,750,000 4,750,000 (475,000) 4,275,000 1,530,000 2,250,000 750,000 $ 11,700,000 5,805,000 5,895,000 3,000,000 $ 2,895,000 May 2017 475,000 4,275,000 4,750,000 (237,500) 4,512,500 1,615,000 2,250,000 750,000 $ 12,350,000 6,127,500 6,222,500 3,000,000 $ 3,222,500 Revenues Cost of goods sold: Beginning inventory Variable manufacturing costs Allocated fixed manufacturing costs Cost of goods available for sale Less: Ending inventory Adjustment for production-volume variance Cost of goods sold Gross margin Operating costs: Variable operating costs Fixed operating costs Total operating costs Operating income $ April 2017 $ 11,700,000 0 4,750,000 2,250,000 7,000,000 (700,000) 0 1,530,000 750,000 6,300,000 5,400,000 2,280,000 $ 3,120,000 $ May 2017 700,000 4,275,000 2,025,000 7,000,000 (350,000) 225,000 U 1,615,000 750,000 $ 12,350,000 6,875,000 5,475,000 2,365,000 $ 3,110,000 Direct material cost per unit Direct manufacturing labor cost per unit Manufacturing overhead cost per unit $ April 6,800 $ 1,800 900 May 6,800 1,800 900 1. Prepare income statements for Speedy Motors in April and May 2017 under throughput costing. 2. Contrast the results in requirement 1 with the absorption and variable costing income statements presented. 3. Give one motivation for Speedy Motors to adopt throughput costing.

Step by Step Solution

3.40 Rating (153 Votes )

There are 3 Steps involved in it

Step: 1

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Document Format ( 2 attachments)

6367a2ed5c0e9_235740.pdf

180 KBs PDF File

6367a2ed5c0e9_235740.docx

120 KBs Word File

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Srikant M. Datar, Madhav V. Rajan

16th edition

134475585, 978-0134475998, 134475992, 978-0134475585