Answered step by step

Verified Expert Solution

Question

1 Approved Answer

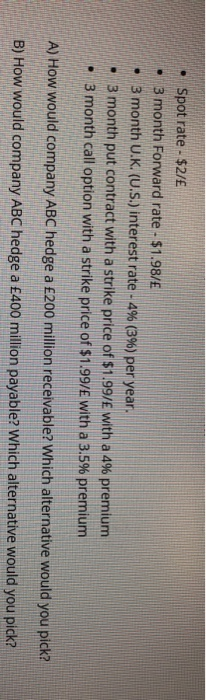

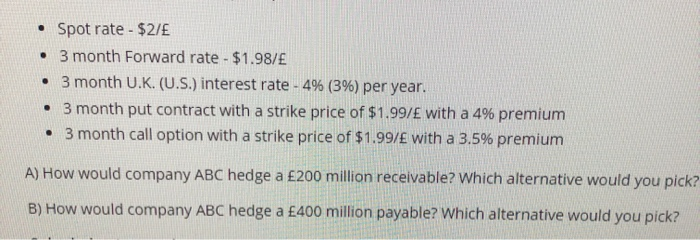

Spot rate - $2/E 3 month Forward rate -$1.98/E 3 month U.K. (U.S.) interest rate- 4% ( 396 ) per year. 3 month put contract

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Commodity Futures And Forex Technical Analysis October To November 2020

Authors: Ascencore Site

1st Edition

979-8693096387