Answered step by step

Verified Expert Solution

Question

1 Approved Answer

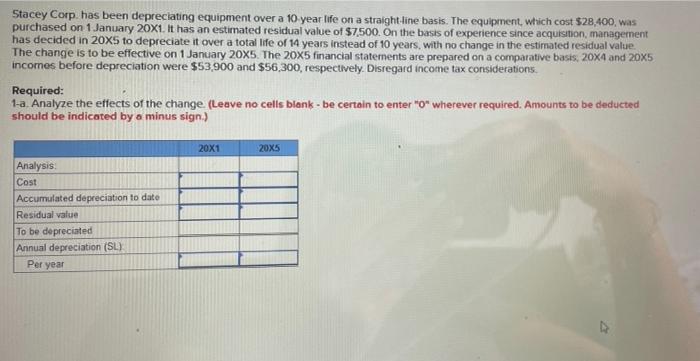

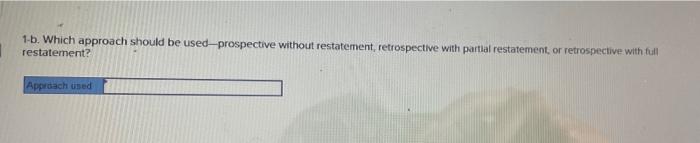

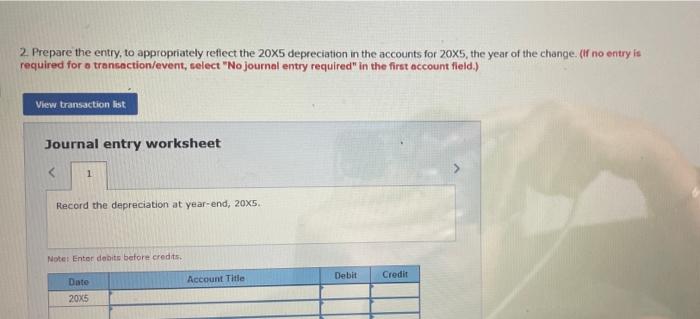

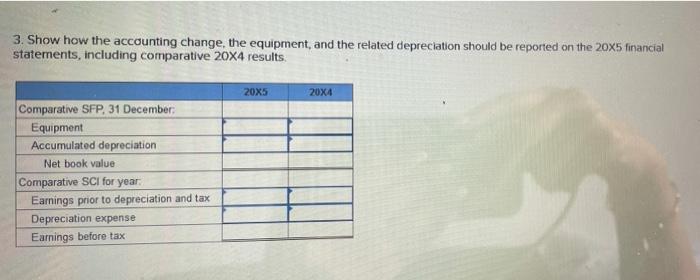

Stacey Corp. has been depreciating equipment over a 10 year life on a straight line basis. The equipment, which cost $28,400, was purchased on 1

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Information Audit For The Management Process Empresa Nacional De Productos Agropecuarios ENPA Of Villa Clara

Authors: Alejandra María Osorio Capote, Manuel Osvaldo Machado Rivero, Dianelys Martínez Paz

1st Edition

6203767883, 978-6203767889