Answered step by step

Verified Expert Solution

Question

1 Approved Answer

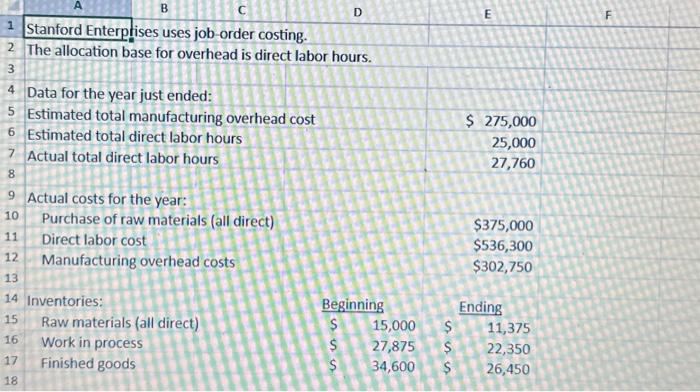

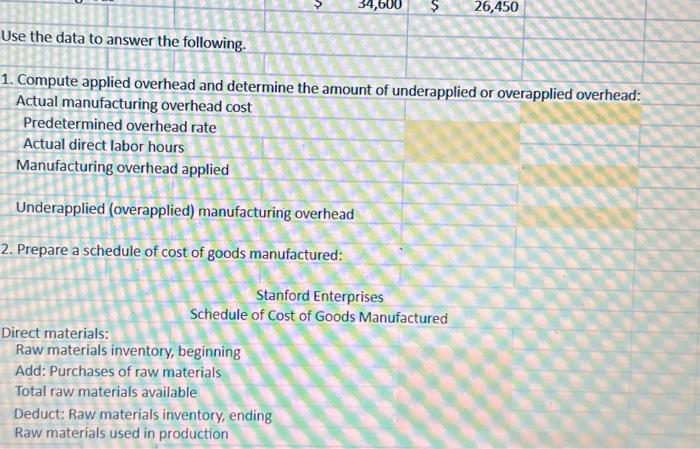

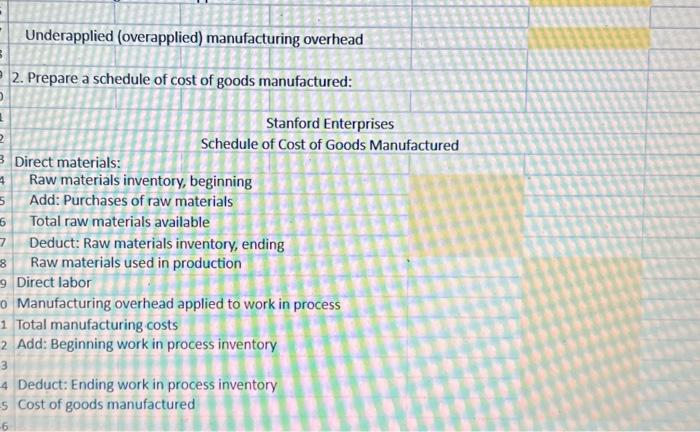

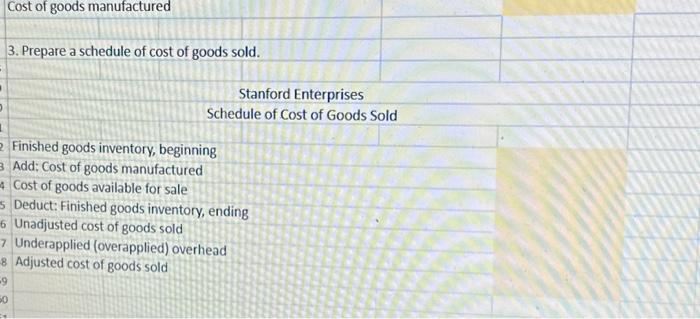

Stanford Enterptises uses job-order costing. The allocation base for overhead is direct labor hours. Actual costs for the year: begin{tabular}{ll} Purchase of raw materials (all

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Easyinvoice Invoice Billing Reception Selling Easy To Use

Authors: Thian Thima

B0C87VL1CF