StanfordSOCIAL INNOVATION REVIEW Up For Debate When Can Impact Investing Create Real Impact? By Paul Brest & Kelly Born With Responses From Audrey Choi, Sterling

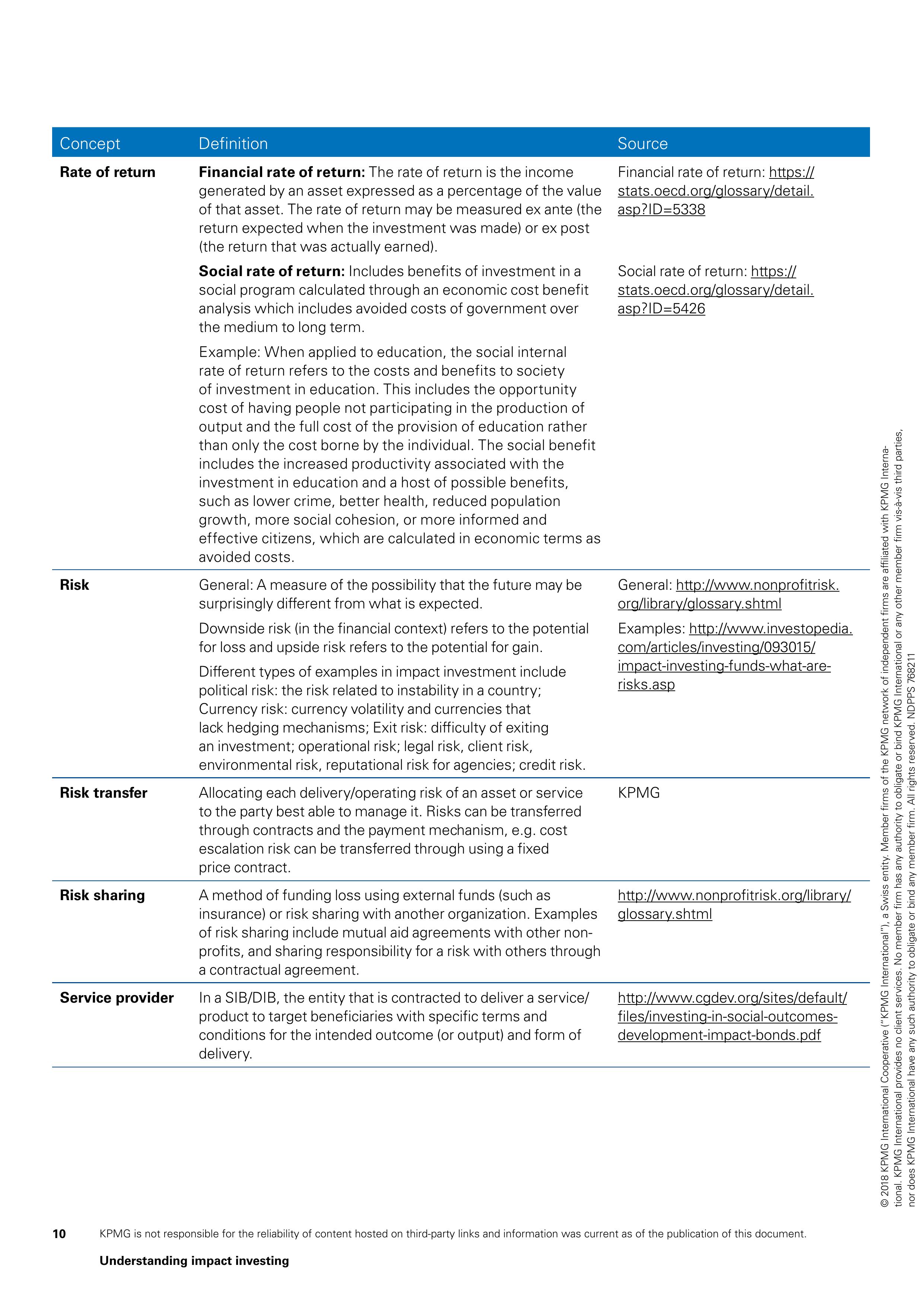

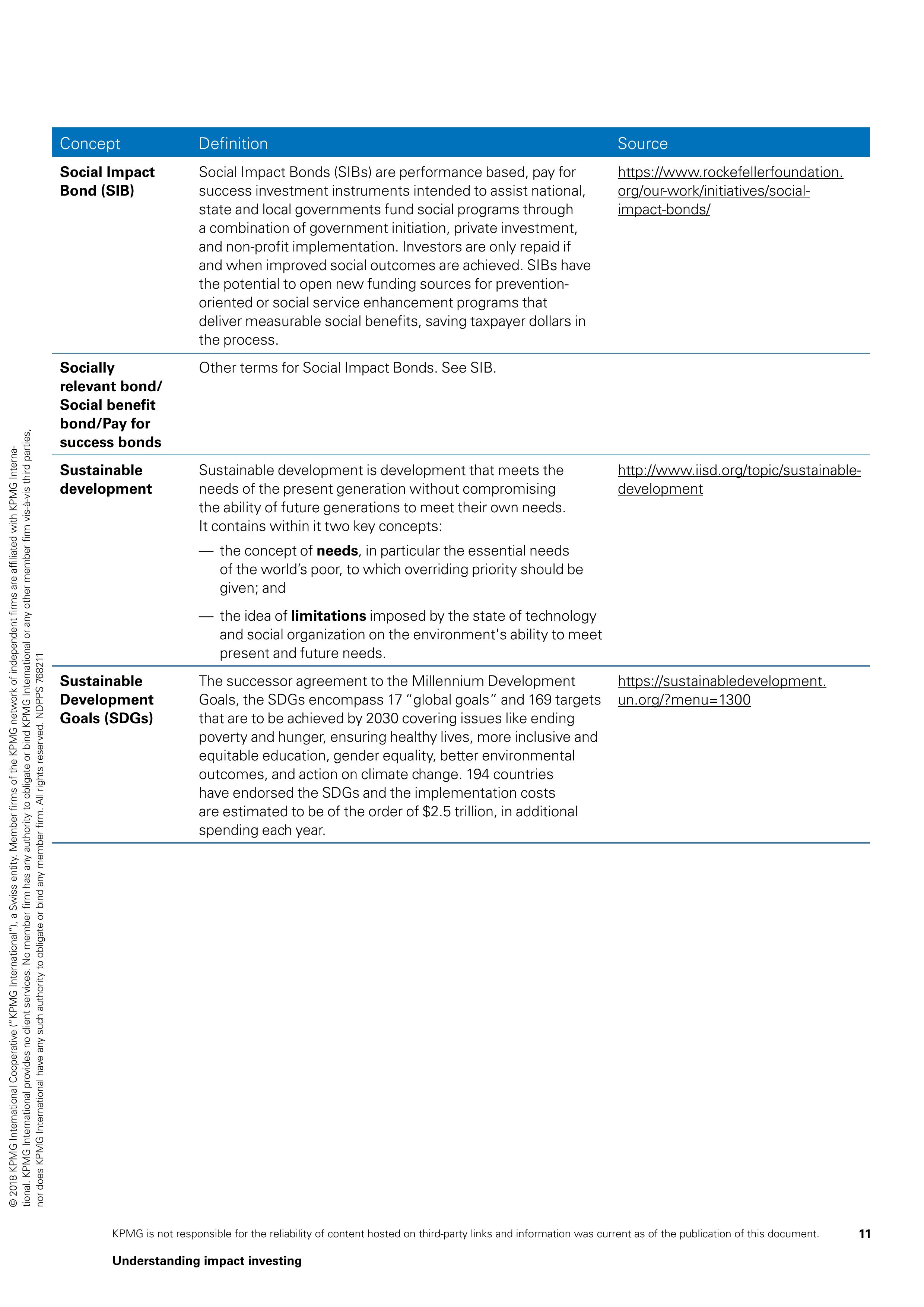

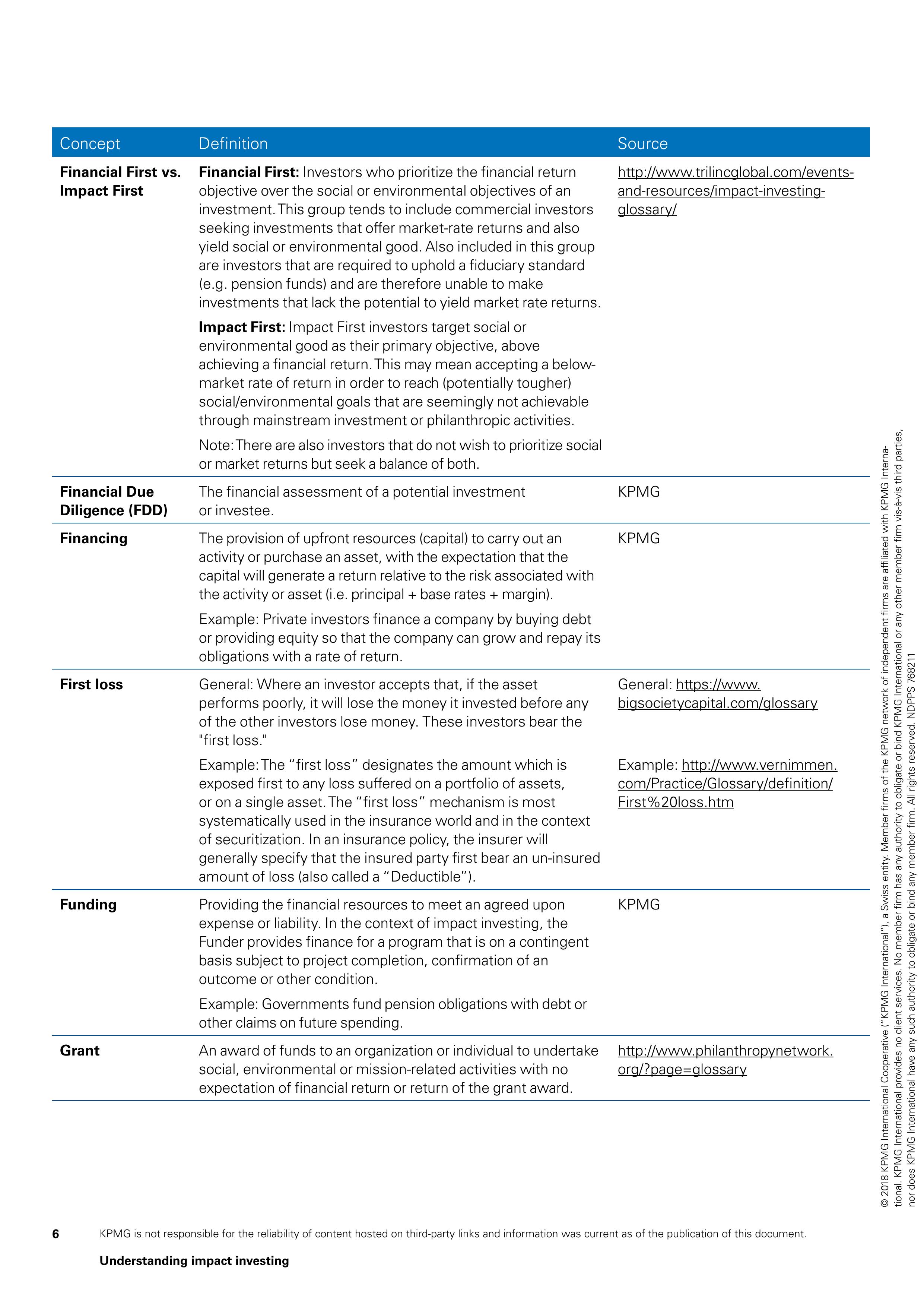

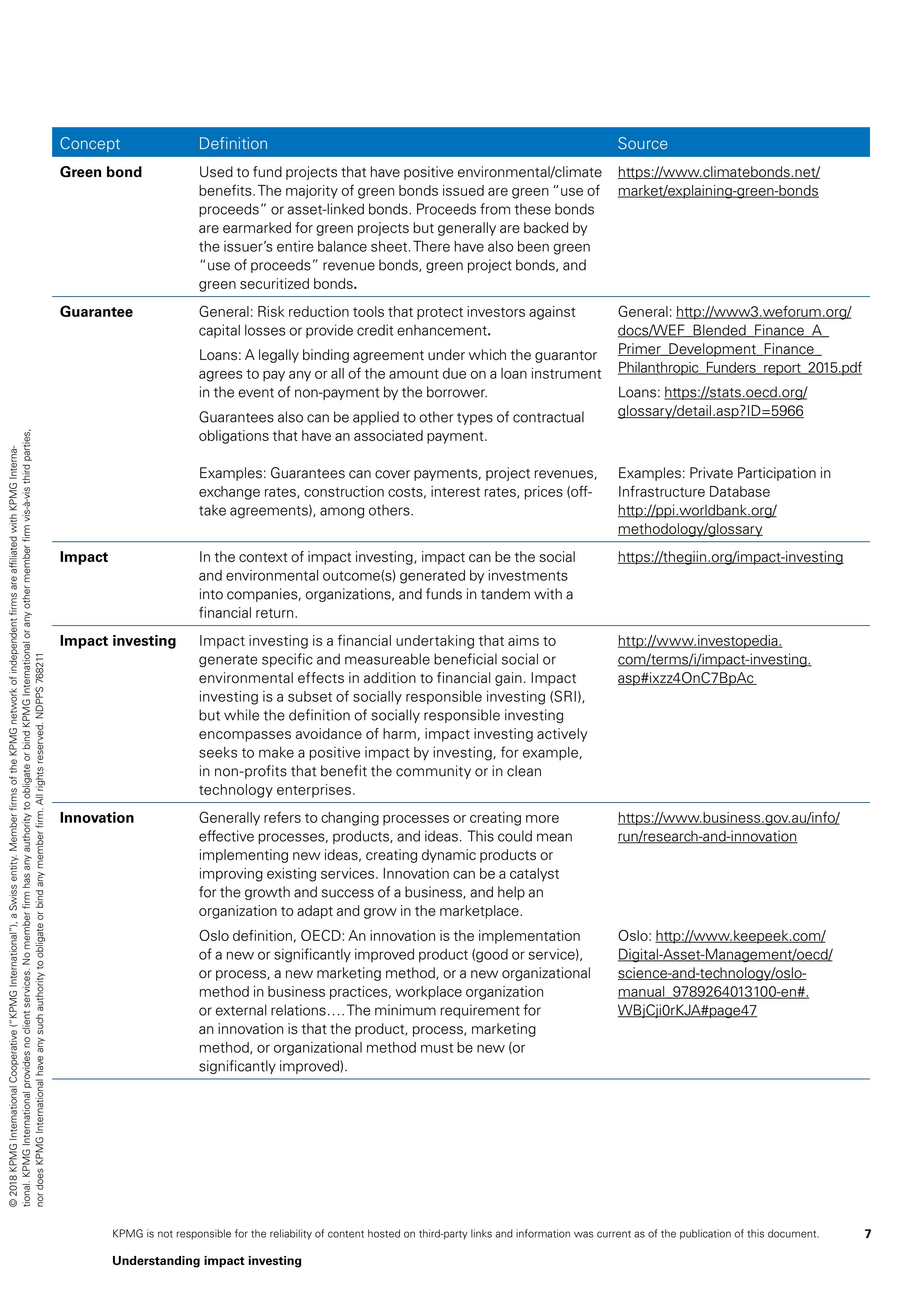

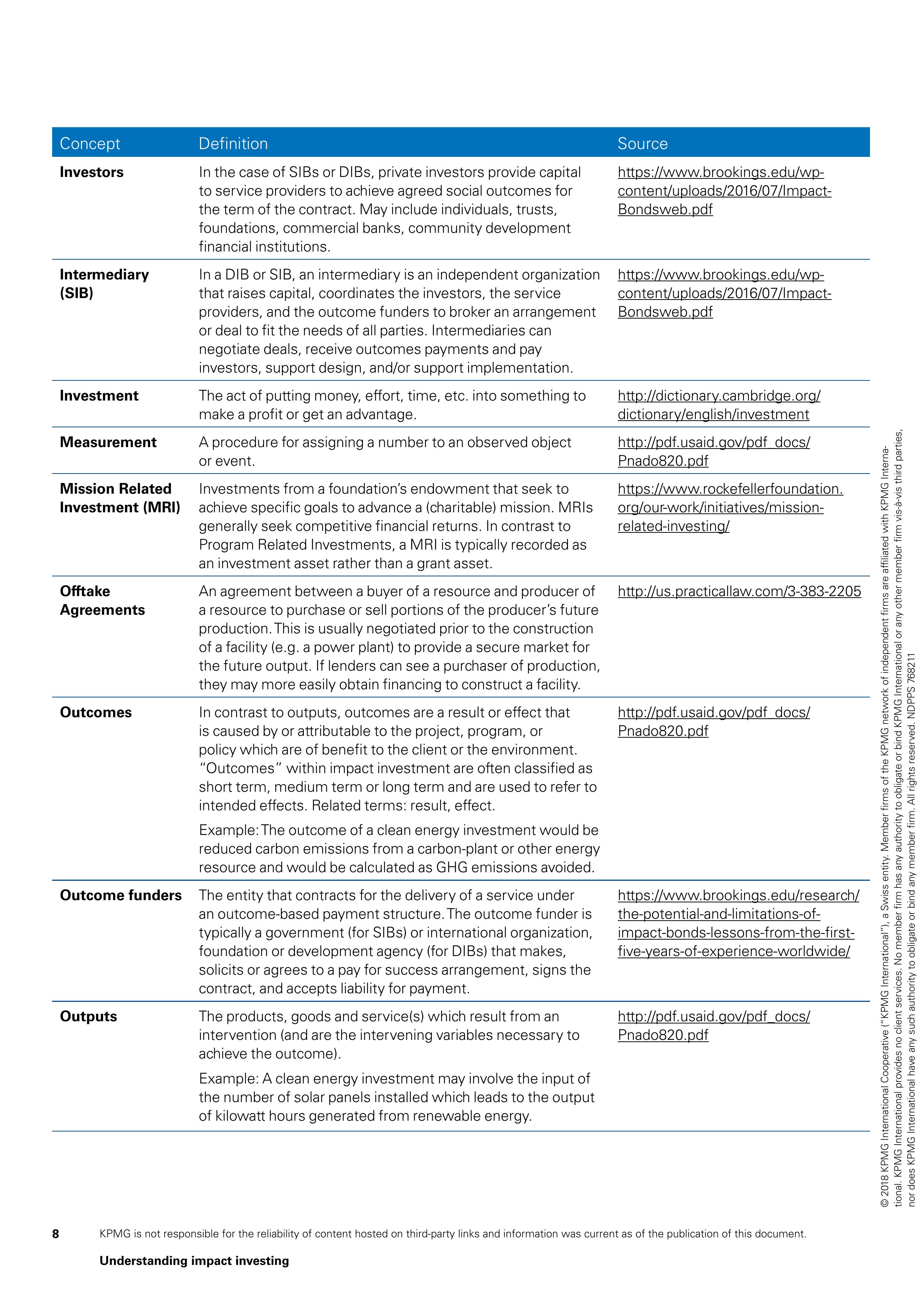

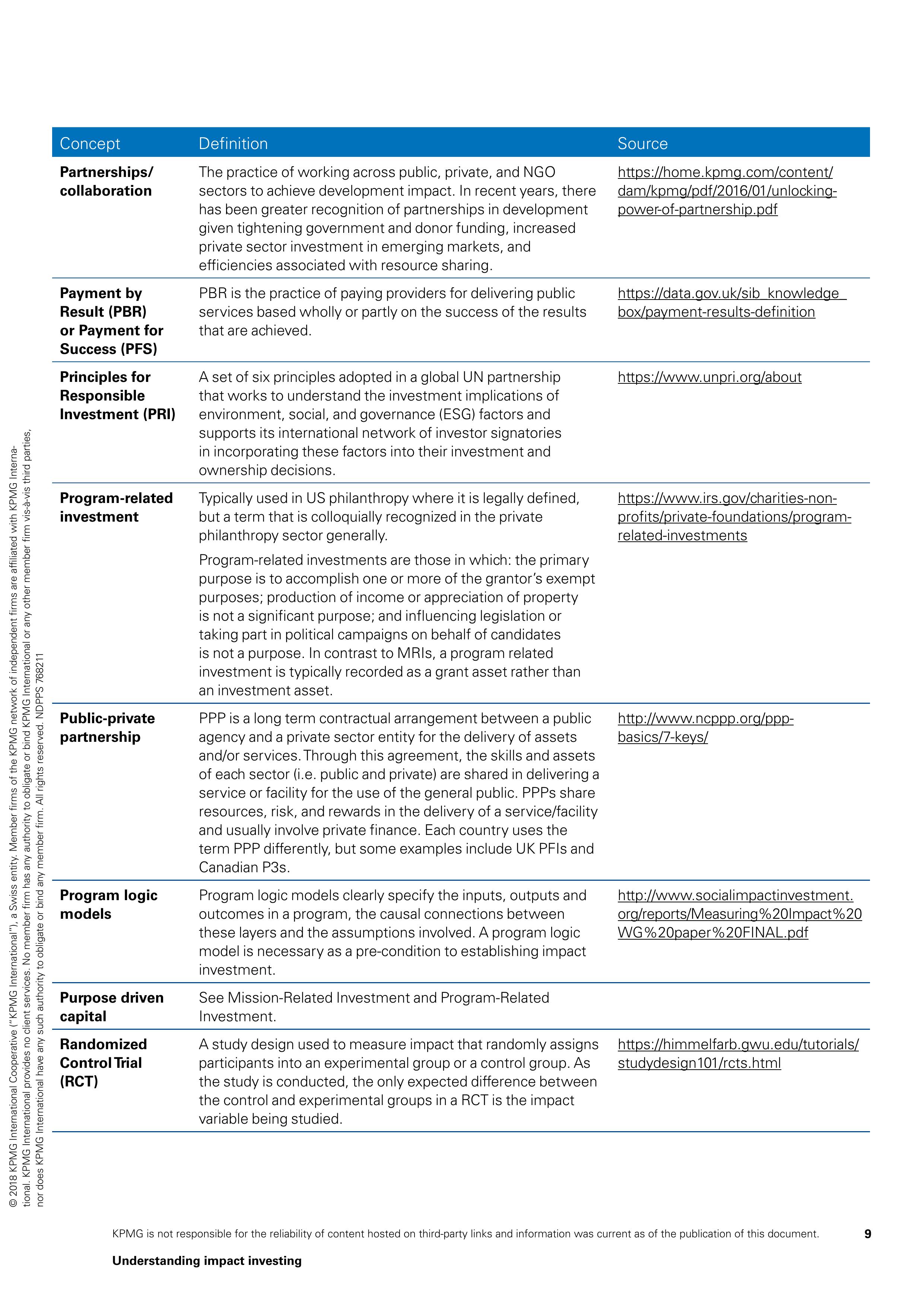

StanfordSOCIAL INNOVATION REVIEW Up For Debate When Can Impact Investing Create Real Impact? By Paul Brest & Kelly Born With Responses From Audrey Choi, Sterling K. Speirn, Alvaro Rodriguez Arregui & Michael Chu, Nancy E. Pfund, and Nick O'Donohoe Stanford Social Innovation Review Fall 2013 Copyright @ 2013 by Leland Stanford Jr. University All Rights Reserved Stanford Social Innovation Review Email: info@ssireview.org, www.ssireview.orgUP FOR DEBATE philanthropy too often funds no risk and therefore no innovation, as when it gives free houses to the homeless or waits in line to provide growth capital to alreadyproven social enterprises. One last thought. Venture capitalists understand that their industry is based on the portfolio approach to returns. In impact investing we seem to have missed this lesson. With a \"concession ary returns\" approach, the end result is a portfolio characterized by very low risk/low returns projects that, by denition, are nei ther transformative not very innovative. Instead we should adopt the portfolio approach, knowing that most projects that swing for the bleachers will fail but those that succeed will achieve such high impact and nancial returns that they will more than compensate for the failures. NAch E. PFUND is founderand man- aging partner at DBL Investors. She was previously a managing director atJ. P. Morgan and managing director in the venture capitaldepartment of Hambrecht& Quist. Nancy E. Pfund ately, it seems, just about everybody is becoming an impact investor. \"All good,\" one might say, for who wouldn't want to rally behind those who strive to make a difference in the world while implementing a compelling investment strategy? The tricky part, as Paul Brest and Kelly Born argue in their thoughtful article, is determining what exactly that impact looks like and whether its existence bears any connection to the investment process attached to it. After almost 10 years of building our practice of doublebottom line venture capital at DBL Investors, we nd many aspects of the authors' conceptual framework resonant, including the notion of perspicacity, the presence or absence of udditz'onality, and the im portance of metrics and nonmonetary benets. By its nature,venture capital as an asset class relies on a certain level of perspicacity, as referenced in the articlediscerning op portunities that ordinary investors don't see. Routinely investing in often unproven entrepreneurs who take on difcult product development challenges in markets that can be hostile does not happen successfully Without some sixth sense that the innovation will prevail and that the odds are not as bad as they appear. What impact investing lends to the venture capital model is another level of purpose, one that reaches into a social or environmental domain by splicing itself into the DNA of a young company whose culture is still in the making. For example, in the early days of Tesla Motors (one of our invest ees), when we were looking for a site to build a manufacturing plant, DBL helped the company explore regions of the San Francisco Bay 30 STANFORD SOCi/L INVOVAIiON REVIEW - Fail 208 Area that might be suitable and where economic development incen tives could help to level the playing eld compared to other countries and states that had lower costs. This effort stemmed from aspects of our mission at that time,which included reducing the carbon footprint of transportation and creating highquality jobs in Bay Area neigh borhoods that needed them. Through a process that broke apart the conventional wisdom about whether California was an appropriate place to manufacture, the Tesla team's perspicacity helped it grab a plant (the former NUMMI plant in Fremont) that many thought was out of its reach, creating a strategic win for both the company and the community. Whether this would have happened without a robust and purposeful early collaboration with DBL Investors we will never know. We do know that to infuse impact into decision making, one needs rst to get a seat at the decisionmaking table. While the Tesla example shows how mission can leadto nonmon etary assistance to a company that can create very strategic benets, the fact that DBL Investors invested alongside traditional venture capital rms makes the question of additionality harder to answer. In other cases, it is much clearer. When evaluating a prospective investment with both a social lens and a nancial returns lens, we have found that we can connect the dots a little sooner as to why a particular company idea might work. This is because we are keyed into certain societal trends, problems, and policies that have been hard to solve and may even be getting worse. In these situations, it may well be time to turn to an entrepreneurial company to build on previous research and programmatic development from public and nonprot organizations and to work to solve the problem at a scale unachievable by grants and socialwelfare programs alone. Revolution Foods is the clearest example of this in our portfolio. DBL seeded this company at a time when it was very difcult for the founders to attract investment because the company's purpose was \"offspec\" from traditional venture business models. For us,by contrast, the company represented an exciting opportunity to ad dress the epidemic of obesity and diabetes in our schools, particularly those in lowerincome demographics. We also believed that crack ing the code on Kiz healthy meal preparation would be of interest and value to existing players in the food service industry, creating potential for signicant value creation. Today, Revolution Foods is serving more than 200,000 meals a day to children in K12 schools and has attracted investment from an array of traditional and impact investors. In this as well as many other cases, the impact investor who sees the potential early and so invests early acts as a catalyst to help the entrepreneur gain access to traditional investors later on. Finally, the appealby Brest and Born at the end of the article for investors to start measuring and analyzing aspects of their work rings very true to DBL Investors. As the examples I have presented here demonstrate, if you don't track the efforts, count the jobs, de tail the carbon saved, or whatever your socialmission priorities happen to be, it is very hard to show how or whether your invest ment approach has made a difference. At DBL, twice a year since the inception of both our funds we have been writing quantitative and qualitative impact reports that detail successes, failures, and works in process across a wide range of industries and locales, and through these reports we have been able to help our investors and ourselves assess the nature and scope of our impact. We believe that some aspects of doublebottomline venture capi tal investing, such as working with broader constituencies, paying attention to place, and engaging in policyissues, will become main stream. In the startup world, using perspicacitywith purpose to build businesses and address social problems is a way to refresh the venture capital model to address 21stcentury needs and opportunities. NlCK O'DONOHOE is CEO of Big Society Capital. He was previously head of global research atJ. P. Morgan. AL Nick O'Donohoe or practitioners in the world of socialimpact invest ing, a number of questions come up time and again: How do we dene a social investment? How do we dene social enterprise? and How big is the market and should we dene it as an asset class? The question that comes up most of all is Do we believe that making an investment with the intent of creating impact necessarilyleads to a riskadjusted return that is lower than a purely nancial investor would expect? Or in other words, Does impact investing require investors to \"trade off\" social return against nancial return, or is it in fact a \"free lunch\" that allows investors to optimize riskadjusted returns at the same time as they generate positive social value? The article by Paul Brest and Kelly Born is by some margin the most coherent attempt yet to consider this question. In the January 2013 survey of impact investors by J. P. Morgan and the Global Impact Investing Network, Perspectives on Progress, 65 per cent of respondents indicated that they were seeking marketrate returns. If Brest and Born are right in saying that they are \"skepti cal about how much of the impact investing market actually ts this description,\" then at best these investors are going to nd it very difcult to nd suitable investments, and at worst they are facing disappointing nancial returns. So is the authors' skepticism justied? Broadly speaking, Ibelieve it is. In my view the vast majority of impact investors projecting marketrate returns fall into one of four categories. They are in fact earning a marketrate return but only because there is subsidy in the capital structure. For example, large US banks are increasingly describing their lending to Community Development Financial Institutions (CDFIs) as impact invest ing. Without wanting in any way to discourage this activity, I would point out that the CDFIs receive signicant subsidy through government grants and tax credits, and the banks that lend to them rely on that subsidy to earn their return. They are confusing absolute return with riskadjusted return. Projecting a 15 percent return for a micronance equity fund may seem like a reasonable absolute return, but it is not close to What an appropriate riskadjusted return would be for ear lystage investments in some of the least developed markets in the world. They focus on returns from individual investments rather than returns on the entire portfolio. The extraordinary returns to the original shareholders in Compartamos do not prove that a portfolio of micronance equity generates commercial riskad j usted returns. They confuse projected returns with actual returns. Risk and return data are scarce in the impact investing world, and the projected returns of an investment manager rarely match ac tual returns. I particularly nd Brest and Born's notion ofinvestment impact helpful. They are correct in suggesting that for impact investment to have impact it has to be \"additive,\" and although it is easyto ar gue that concessionary investments are additive, it is much more difcult to do that with nonconcessionary investments. Is it ever possible for the impact investor to earn a market re turn? Are there ways in which being an impact investor gives a competitive advantage over mainstream investors that allow the impact investor to optimize nancial and social return? The authors identify a number of frictions that may impose barriers to what they describe as socially neutral investors but may provide some competitive advantage to socially motivated inves tors. Some of these frictionssuch as small deal size, limited exit, and governance issuesare true of any investment portfolio that focuses on smaller companies, particularly in emerging markets. The authors also describe a skepticism and inexibility that can create an unintended bias among mainstream investors. The following is a gross generalization, but I am going to make it in any case. If you go into any mainstream bank, investment manager, or private equity rm in Europe or the United States you nd the same people: hordes of MBAs from the same schools investing with people they know and like, in places they visit and in busi nesses they can relate to. This homogeneity among investors has unintended consequences. New business models that create social value through the people they employ, the products they produce, or the areas in which they locate tend to nd it difcult to attract capital. Because impact in vestors start from a different point of view, they go places, meet people, and see opportunities that the mainstream investment community misses. It may be possible, as David Chen notes, for them to \"see something that you don't see.\" I share the conclusion that it is critical for impact investors who are providing concessionary capital to provide clear measurable metrics that demonstrate and support the impact they are creat ing. Those, however, who seek to provide nonconcessionary capi tal also need to demonstrate evidence of impact, but they must in addition be able to articulate their investment impact, and that means a clear articulation of why normal commercial investors are missing the opportunities that they are pursuing. FallZOlE -ST/\\MORD SOClM INNOVAIlOK REVIEW 31 UP FOR DEBATE When Can Impact Investing Create Real Impact? Although it is possible for impact investors to achieve social impact along with market rate returns, its not eas')7 to do and doesn't happen nearly as often as many boosters would haveyou believe. BY PAUL BREST 8c KELLY BORN ILLUSTRATION BY BEN VVISEMAIV here has been an increasing realization that, along with philanthropy and government aid, private enterprise can contribute to solving social and environmental problems. At the same time, a growing number of investors are expressing a desire to \"do good while do ing well.\" These are impact investors, who seek opportunities for nancial investments that produce social or environmental ben ets. However, the rapid growth of the eld of impact investing has been accompanied by questions about how to assess impact, and concerns about potentially unrealistic expectations of simultane ously achieving social impact and marketrate returns. This article is addressed to impact investors who wish to know whether their investments will actually contribute to achieving their social or environmental (hereafter, simply \"social\") objec tives. We introduce three basic parameters of impact: enterprise impact, investment impact, and nonmonetary impact. Enterprise impact is the social value of the goods, services, or other benets provided by the investee enterprise. Investment impact is a par ticular investor's nancial contribution to the social value created by an enterprise. N onmonetary impact reects the various contri butions, besides dollars, that investors, fund managers, and others may make to the enterprise's social value. The most novel and intriguing question we consider is whether and when investors can expect both to receive riskadjusted marketrate 22 STMJFORD SOCl/L lNVOVAllON REVlEW - Fall ZOl3 WITH RESPONSES FROM Audrey Choi | 27 Sterling K. Speirn | 28 Alvaro Rodriguez Arregui 8: Michael Chu l 29 Nancy E. Pfund I30 Nick O'Donohoe l 31 I Responses from 10 other thought eaaers l Authors' comments on responses I Lively discussion with your peers l Longer version of Paul Brest and Kelly Born'sarticlc returns on their investments and to have real social impact: that is, can investors both make money and make a difference? That is the claim made bymany impact investment funds. One recent Ludxas serts that most of what it estimates to be a $4 billion impact invest ing market involves investments producing market rate returns.1 We posit that a particular investment has impact only if it increases the quantity or quality of the enterprises social outcomes beyond what would otherwise have occurred. Under this deni tion, it is readily apparent that grants or concessionary investments (investments that sacrice some nancial gain to achieve a social benet) can have impact: By hypothesis, an ordinary market inves tor, who seeks marketrate returns, would not provide the capital on as favorable terms, if at all. But if an impact investor is not willing to make a nancial sac rice, what can he contribute that the market wouldn't do anyway? We believe that in publicly traded large cap markets, the answer is nothing: Even quite large individual investments will not affect the equilibrium of these essentially perfect markets. The frictions or imperfections inherent in some smaller, private markets, how ever, may offer the possibility of achieving both market returns and social impact. For example, someone with distinctive knowledge about the risk and potential returns of a particular opportunity may make an investment that others would pass up. The question of investment impact is of obvious importance to investors who want to make a difference. Although we do not reject the possibility of earning marketrate nancial returns while achieving social impact, we are skeptical about how much of the impact investing market actually ts this description. Impact Investing Defined An impact investor seeks to produce benecial social outcomes that would not occurbut for his investment in a social enterprise. In international development and carbon markets, this is called \fUP FOR DEBATE additionality. With this core concept in mind, we dene the prac tice of impact investing capaciously, as actively placing capital in enterprises that generate social or environmental goods, services, or ancillary benets such as creating good jobs, with expected nancial returns ranging from the highly concessionary to above market.2 The adverb \"actively\" excludes negative investment screens. This is not a judgment about their value, but rather reects the general understanding that impact investing encompasses only afrmative investments. Within the eld of impact investing, we include concessionary investments, which sacrice some nancial returns to achieve social benets, and nonconcessionary invest ments, which expect riskadjusted market returns or better. Like philanthropists, impact investors invariably intend to achieve social goals. They are, by denition, socially motivated. Their goals maybe as specic as providing antimalariabed nets to residents of a region in Africa or as general as doing environmen tal good. In contrast, socially neutral investors are indifferent to the social consequences of their investments. Many endowments invest in a socially neutral manner, as do individuals who invest through money managers or funds whose only mandate is to maxi mize nancial returns. Whatever an investor's intention, the fundamental question is whether an investment actually has social impact. For example, so cially neutral investors, motivated only by prot, have contributed to the social impact of telecommunications companies in both the developed and developing world. Yet while social impact can be achieved unintentionally, this does not mean that intention is unim portant. In business, as in philanthropy and all other spheres of life, people are more likely to achieve results that they intentionally seek. Having impact implies causation, and therefore depends on the idea of the counterfactualon what would have happened if a particular investment or activity had not occurred. The en terprise itself has impact only if it produces social outcomes that An enterprise can have impact in several ways, two ofwhich are fundamentalzproolactimpactis the impact of the goods and services produced by the enterprise (such as providing antimalariabed nets or clean water); operational impact is the impact of the enterprise's management practices on its employees' health and economic se curity, its effect on jobs or other aspects of the wellbeing of the community in which it operates, or the environmental effects of its supply chain and operations. The theoretical framework that underlies the assessment of enterprise impact makes a distinction between outputs and out comes. An output is the product or service produced by an enter prise; the (ultimate) outcome is the effect of the output in improving people's lives. So the impact investor must answer two questions: First, to what extent will the intended output occur? Second, to what extent will the output contribute to the intended outcome (where the counterfactual is that the outcome would have oc curred in any event)? Consider an investor supporting an organization that manufac tures and distributes bed nets with the goal of reducing morbidity and mortality from malaria. The focus of the rst question is whether the bed nets were manufactured and distributed. It is answered by looking at the quantity and quality of the organization's outputs. The second question is concerned with whether the bed nets ac tually reduced malaria in the target population. For example, even if bed nets are often effective, and even if the ultimate outcome occurred in the target population, can the reduction in malaria be attributed to the enterprise? Perhaps the reduction was due to a simultaneous vaccination or mosquito eradication program. The question of outcomes, or social impact, is typically answered by usingthe same social science methods used in assessing outcomes in public policy and philanthropyfor example, randomized con trolled studies or econometric analysis. The Impact Reporting and Investment Standards (IRIS) and would not otherwise have occurred. And for an investment or Globallmpact Investment Rating System (GIIRS) provide standard nonmonetary activity to have impact, it must increase the quan tity or quality of the enterprise's social outcomes beyond what would otherwise have occurred. Enterprise Impact In this article, we explore the three parameters of impact: the im pact of the enterprise, investors' contribution to the enterprise's impact, and the contribution of nonmonetary activities to an en terprise's impact. Without successful outcomes from the social enterprise, no investment can have social impact. Therefore, the social impact of investors and other actors ultimately depends on that of the enterprises they support. Hewlett Foundation. 24 STANFORD SOCl/L INVOVAIION REVIEW - Fall ZOl3 PAUL B REST is emeritus professor at Stanford Law School, a lecturer at the Graduate School of Business, and a faculty co-directorofthe Stan- ford Center on Philanthropy and Civil Society. He was previously president ofthe William and Flora KELLY BORN is a fellow in charge of special proj- ects at the William and Flora Hewlett Foundation. Before joining the Hewlett Foundation shewas a strategy consultant with the Monitor Institute. ized metrics for assessing some common output criteria. But these focus more on an enterprise's operations than on its products. With rare exceptionsmost notably, the eld of micronancethere have been few efforts to evaluate the actual outcomes of market based social enterprises. The absence of data and analysis makes it difcult for impact investors to assess the social impact of the enterprises they invest in. Investment Impact As we noted above, to have investment impact requires that an in vestment increase the quantity or quality of the enterprise's social output beyond what would otherwise have occurred. Assuming that, at the time of an investment, the enterprise can productively absorb more capital, then an investment has impact if it provides more capital, or capital at lower cost, than the enterprise would otherwise get. Debra Schwartz, director of programrelated invest ments at the MacArthur Foundation, has alliteratively summarized the kinds of capital benets that impact investors can provide in terms of ve P's, to which we add a sixth, perspicacity: Price. Belowmarket investments Pledge. Loan guarantees Position. Subordinated debt or equity positions Patience. Longer terms before exit Purpose. Flexibility in adapting capital investments to the enterprise's needs Perspicacity. Discerning opportunities that ordinary investors don't see These capital benets enable the enterprise to experiment, scale up, or pursue social objectives to an extent that it otherwise could not. The rst ve are particularly relevant to investments that expect belowmarket returns. The sixth, perspicacity, may hold the key to achieving both market returns and social impact. Sociallymotivated investors fall into two categories: concession aryinvestors who are willing to make some nancial sacriceby taking greater risks or accepting lower returnsto achieve their social goals; and nonconcessionary investors who are not will ing to make any nancial sacrice to achieve their social goals. Most socalled \"doublebottomline\" impact investors are non concessionary. In the context of philanthropy, nonconcessionary socially motivated investments are often called missionrelated investments, and are distinguished from programrelated invest ments, which are generally concessionary. Concessionary Investments l The return sacriced by a con cessionary investment is, in effect, a charitable donation or grant. Assuming that the enterprise can productively deploy additional cap ital, a concessionary investment has investment impact virtually by denition, because it makes available capital to which an enterprise would not otherwise have access. Consider three general situations in which impact investors have made concessionary investments. Supporting nascent enterprises. The early stages of many social enterprises that aspire to become nancially sustainable depend on philanthropy and highly concessionary investments that involve higher risks than ordinary market investors would take. This was true of micronance and of other social enterprises that serve baseofpyramid (BOP) populations, which often depend on in novations in technology and marketing and require signicant investments before yielding any nancial returns. Subsidizingongoingenterprises. Some mature social enterprises require the ongoing support of investors who are willing to forgo a degree of nancial return for social benets. For example, in 1994 the US Department of the Treasury created Community Devel opment Financial Institutions (CDFIs) to \"provide economically depressed communities access to credit, equity, capital, and basic banking products.\" Subsequently, the Calvert Foundation began offering belowmarket Calvert Community Notes, which in turn are invested in CDFIaccredited community organizations that provide belowmarket loans to nonprot organizations and small businesses in underserved communities. Simultaneous layering of concessionary and nonconcessionary investments, with the former intended to encourage the latter. For example, the New York City Acquisition Fund is designed to promote the development of affordable housing by providing ex ible capital for developers. The city was joined by the MacArthur, Rockefeller, F. B. Heron, Robin Hood, Starr, and Ford foundations in providing subordinate debt and loan guarantees. More or less nonconcessionary investors include Bank of America, JP Morgan Chase, and HSBC. These are examples of the benecial effects of subsidies. But the fact that an investment is concessionary is no guarantee that it will create net positive social impact. Subsidies can also mask an enterprise's inefciencies and crowd out healthy competition. Subsidizing micronance and community development institutions has been both positive and harmful in different circumstances. In any event, the ideal outcome for most enterprises that initially rely on concessionary capital is that they eventually yield market returns and attract socially neutral investors. Here, impact inves tors have played their part in bringing the enterprise to market, the impact investing story is over, and the enterprise is now supported by customers and ordinary market investors. The modern history of micronance provides examples of this. The story begins with grants to the Grameen Bank and other mi cronance institutions (MFIs) to develop and prove the concept, followed by concessionary loans and equity investments to begin implementing it. Although even today many MF Is depend on sub sidized investments, an increasing number now attract market investors. For example, in 2007 the initial public offering of the highly protable Compartamos Banco was vastly oversubscribed, and some mainstream banks, such as Citigroup, now have a mi cronance business. This generally positive story has a dark side, however. As MFIs become more nancially attractive, they may adopt practices that compromise their social missions. NonConcessionary Investments | It's easy to see how below market investors can provide capitalbenets to an enterprise,but it is less clearhowandwhen investors expecting market returns (orbetter) have investment impact. Yet much of the impact investment space is occupied by funds that promise their investors both sociallyvaluable outputs and at least market returns. For example, Elevar Equity gen erates \"outstanding investment returns by delivering essential ser vices to disconnected communities underservedby global networks.\" We don't question these fund managers' assertions that their investments have strong nancial returns. The immediate ques tion is how their investments might have investment impact. Un der our criterion of additionality, the investment must increase the quantity or quality of the social or environmental outcome beyond what would otherwise have occurred. The counterfactual is that ordinary, socially neutral investors would have provided the same capital in any event. Under the additionality criterion, how can an impact investor expect market returns and still provide capital benets to the enterprise? After all, if it's a good investment, one would expect socially neutral investors to be in it as well. Most economists agree that it is virtually impossible for a so cially motivated investor to increase the benecial outputs of a publicly traded corporation by purchasing its stock. Especially ifas is generally the casestock is purchased from existing shareholders, any benet to the company is highly attenuated if it exists at all. Impact investing typically does not take place in large cap public markets, however, but rather in domains subject to market frictions. While some of these frictions impose barriers FallZOlE -ST/\\MORD SOClAl lNNOVATlOA REVIEW 25 UP FOR DEBATE to socially neutral investors, socially motivated impact investors may exploit them to reap both social benets and marketrate nancial returns. These frictions include: Imperfect information. Investors at large may not know about particular opportunitiesespecially enterprises in developing nations or in lowincome areas in developed nationslet alone have reliable information about their risks and expected returns. Skepticism about achieving both nancial returns and social impact. Investors at large may be unjustiably skeptical that enterpris es that are promoted as producing social or environmental val ue are likely to yield marketrate returns. Inexible institutional practices. Institutional investors may use heuristics that simplify decision making but that exclude po tential impact investments, which, for example, may require more exibility than the fund's practices permit. Small deal size. The typical impact investment is often smaller than similar private equity or venture capital investments, but the minimum threshold of due diligence and other transaction costs can render the investment nancially unattractive re gardless of its social merits. Limited exit strategies. In many developing economies, markets are insufciently developed to provide reliable options for in vestors to exit their investment in a reasonable time. Governance problems. Developing nations may have inadequate governance and legal regimes, creating uncertainties about property rights, contract enforcement, and bribery. Navigating such regimes may require ontheground expertise or personal connections that are not readily available to investors at large. We believe that nonconcessionary impact investors are espe cially likely to have investment impact in conditions of imperfect informationfor example, in social or environmental niche markets where impact investment fund managers or other intermediaries have special expertise or intelligence on the ground. Perfect markets are functionally omniscient, but the impact fund manager says (in the words of David Chen of Equilibrium Capital), \"I see something that you don't see.\" Socially motivated investors may be particularly interested in identifying these op portunities and thus may be able to have impact even at non concessionary rates. This is the most likely explanation for the asserted doublebottomline success of rms like Elevar Equity. Even here, one might ask whether investments that seem non concessionary on their face incorporate hidden concessions in the form of risk or extra and costly due diligence that ordinary investors would not undertake. Nonmonetary Impact Beyond just providing capital, fund managers as well as other actors can improve an enterprise's social outputs by providing a range of nonmonetary benets: Improving the enabling environment for social enterprises and investors. Governments and foundations can provide funding to improve the social, political, and regulatory environments in which social enterprises and their investors operate. For example, 26 STANFORD SOCl/L INVOVAIlON REVIEW - Fall 208 the Boulder Institute has developed scoring and rating models for MFIs, established benchmarking, introduced an open source management information system, and trained thousands of MFI practitioners. In addition to providing public goods of these sorts, awelldesigned set of investments in a sector has the potential to catalyze markets to a greater extent than the sum of random in vestments in the individual investee enterprises. Finding and promoting impact investment opportunities. Impact investment intermediaries are critically important in discovering investment opportunities and bringing them to the attention of investors, thus helping to overcome the information failures previ ously noted. For example, Agora Partnerships identies earlystage impact investment opportunities in Central American communi ties, focusing on small and growing businesses that are too large for microcredit and too small for traditional nancing. Its clients, such as the Draper Richards Kaplan Foundation, engage Agora to pursue impact investment opportunities in the region. Aggregating capital and providing other investmentservices. Fund managers and other intermediaries reduce transaction costs by creating economies of scale, and they may also provide technical assistance to impact investors. For example, Imprint Capital Ad visors helps foundations and family ofces identify domestic and global opportunities for impact investment. Imprint guided sev eral foundations to invest in Southern Bancorp, a US development bank that provides banking and nonprot services aimed at reduc ing poverty and unemployment in distressed rural communities. Providing technical and governance assistance to enterprises, and helping them build strategic relationships. Fund managers and other third parties provide nonmonetary benets, ranging from tech nical assistance for nascent enterprises to helping more mature enterprises develop relationships with customers, suppliers, and other partners. For example, Root Capital's Financial Advisory Services are designed to strengthen the business processes of social enterprises with high growth potential in Africa and Latin America. Training modules focus on business and administrative management, nancial planning, risk management, accounting, and loan applications. Gainingsocially neutral investors. One of the unfortunate charac teristics of imperfect impact investing markets is their inability to attract the large majority of socially neutral investors who demand market returns. Where such returns seem plausible, a respected in stitution can signal to other investors that a particular investment or an entire sector that others may have thought dubious is actually worthy of consideration. For example, the David 8c Lucile Packard Foundation made an initial $1 million equity investment, followed by a lowinterest $10 million loan, in EcoTrust, a sustainable for est management rm. The foundation's general counsel noted: \"Our main reason for investing in EcoTrust Forest in this way is to demonstrate that sustainable forest practices can generate a prot so that mainstream investors will become more interested in it.\" 3 Securing and protecting the enterprise's social mission. Over time an enterprise's management and directors may discover opportu nities to increase nancial returns at the expense of social impact. For example, the manufacturer of products or services designed for BOP clientele may nd it more protable to market to wealthier customers. The dangers are especially acute as the enterprise scales up and takes on new, socially neutral investors. There are a num ber of possible protections against such mission drift, including contractual arrangements; B Corps, and other corporate forms that require, or at least welcome, producing social benets that may compromise market returns; and the continual inuence of socially motivated investors. The Demand for Information About Impact Having addressed this article to impact investors who wish to know whether their investments will actually contribute to social or environmental impact, we conclude with a reality check on in vestors' making this inquiry and learning from it. A 2010 survey of philanthropists and impact investors suggests that the vast majority are not willing to make any effort to gain in formation about the actual social or environmental impact of their investments.4 Social impact is notoriously difcult to measure, and it could wellbe that manyinvestors are satised with the good public relations and warm glow of doing a benecent act. But we are opti mistic that there are impact investors with signicant resources who actually care whether their investments are making a difference. For those who do care, efforts to assess impact come at a cost greater or lesser depending on the degree of evaluative rigor. Estimating the expected nancial return from an investment is a difcult but familiar exercise. Estimating social return is intrin sically much harder because of the complexities of placing values on social and environmental outcomes and predicting what out comes an organization is likely to achieve. Estimating the value of nonmonetary contributions that directly benet an enterprise is a commonplace task that an organization engages in whenever it hires consultants. Estimating the value of nonmonetary contribu tions to an entire sector is a far more speculative task. In contrast to enterprise and nonmonetary impact, assessing a particular investment's additionality in order to determine its investment impact is a novel task that, so far as we know, has not previously been undertaken. In this article, we propose the ques tions that underlie this analysis. An investor who expects market returns must ask whether his nonconcessionary investment is likely to have investment impact, and if so, how much. An investor who is prepared to sacrice market returns should ask how much concession it's worth making for the social value produced by the organization. Although we have no a priori commitment to any particular depth of analysis, we believe that realizing the promise of impact investing depends on all three measures becoming cen tral to the marketplace. This article is based on a longer article by Brest and Born, \"Unpacking the Impact in Impact Investing,\" available at SS | R Online. Notes 1 http://www.paciccommunityventures.org/reportsand-publications/market forsociaLimpact-investing-by-private-equity-funds-stands-at-4billion-in-the- united-states/ 2 Our denition borrows liberally from the denition used in the report Investing for Impact: Case Studies Across Asset Classes, Bridges Ventures The Parthenon Group, and Global Impact Investing Network, p. 3. 3 Stephanie Strom \"To Advance Their Cause, Foundations Buy Stocks \" TheNew York Times, Nov. 24, 2011. 4 http://hopeconsulting.us/money-for-good,' AUDREY CHOI is managing director and head ofGlobal Sustainable Finance at Morgan Stanley. She previ- ously served in a variety of positions in President Bill Clinton's adminis- tration, including chief of staff ofthe Council of Economic Advisers. Audrey Choi aul Brest and Kelly Born's article provides useful rigor in helping a selfidentied \"impact investor\" answer the question, \"How can I be certain that my impact investment is creating an impact that other wise would not have occurred?\" This consideration is particularly relevant for philanthropic individuals or institutions who may be contemplating impact investing as an alternative use for the precious resource of dollars that would otherwise go to grants or concessionary programrelated investments. Many of us in the impact investing eld, however, nd more compelling a different question, \"How can we drive positive change to address the world's problems as broadly, as rapidly, and as effectively as possible?\" If that is the outcome we seek, then it matters much less whether a particular investment counts as an \"actual\" impact investment. It also matters less whether the positive impact created was the cen tral intent or an outcome or byproduct of the investment. What matters more is whether change happens and whether it reaches transformational scale. If those positive changes happen to benet from the tailwinds of market forces, and if the investments were made in the company of nonimpactminded investors who are primarily interested in nancial returns, then so be it. If it is good to fuel the growth of a company that creates critically needed jobs, reduces carbon emissions, or improves community resilience, then isn't it better if we can harness more capital to help that company grow faster and replicate more broadly? Grants, PRIs, and concessionary investments play a critical role in fueling social innovation. The goal of impact investing isn't to substitute for those vital grants or PRIs but rather to tap into the much larger pools of pensions, endowments, and other duciary and commercial capital that can complement and augment the grants and concessionarycapital. Our role as eldbuilders in impact investing, then, should be to create as many broad and inclusive onramps as possible for investors with many different appetites in order to attract as much capital as possible for investment in opportunities that drive, support, and accelerate positive change. For the growing number of mainstream investors beginning to contemplate impact investing as an additional tool in their portfo lios, the rst question should perhaps be \"How can my investment dollars be directed in ways that provide positive social impact as well as satisfy my economic requirements?\" To be sure, a decision to invest with impact may not have as dramatic a socialimpact multiplier effect as a highly intentional, impactrst investment. FellZOIE -ST/\\AFORD SOCIAL NNOVAIIOA REVIEW 27 UP FOR DEBATE But one cannot say that no positive benets accrue from decisions by mainstream investors to direct their funds away from invest ments that have negative or neutral social impact and toward ones that have positive impact. Brest and Born suggest that in marketrate opportunities im pact investors don't actually have much impact, because those businesses already have access to more than enough commercial capital. But economically sensible investments do not necessarily get ample funding automatically. If they did, there wouldbe no need for the venture capital industry, which specializes in identifying and funding busines ses that it believes have the capability to deliver outsized returns but that have been overlookedby traditional capi tal. By seeking out and seeding investments that have the ability to achieve both marketrate returns and high social impact, impact investors can introduce those enterprises to conventional capital and thereby broaden the scope of possible impact. As proponents of impact investing, we are best served when in vestorsimpact or otherwiseare clear about their goals, expecta tions, risk tolerances, return requirements, and desired impact out comes. In assessing howwell aparticular investment ts an inve stor's needs, \"actual impact\" as outlinedby Brest and Born is an important analytic toolas is the recognition that appropriate riskadjusted marketrate returns aren't necessarily at odds with impact, espe cially if they help deliver impact more quickly and more broadly. STERLING K. SPEIRN is presidentand CEO 0fthe W. K. Kellogg Foundation. He was previously president and CEO of Peninsula Community Foundation. l l I MW: lln i Sterling K. Speirn aul Brest and Kelly Born's article brings clear and rigorous analysis to a eld that is desperate to have the practice catch up with the rhetoric, and that un til now has surrounded a provocative idea with too much wishful and fuzzy thinking. In addition to developing avery helpful taxonomy and terminology, Brest and Born raise a critical question: What is the nature of the impact created by the invest ment itself, separate from the outputs or outcomes produced by the social enterprise that received the investment? s M. They argue that investment impactas distinguished from the enterprise impactexists only if the quantity or quality of the en terprise or investee's output is increased \"beyond what would oth erwise have occurred.\" From the perspective of an experienced im pact investorthe W. K. Kellogg Foundation's $100 million Mission Driven Investing Portfolio (MDI) now has a veyear track record across multiple asset classes and sectorsI nd this framework 28 STANFORD SOCl/L |N\\lOW\\IlON REVIEW - Fall 20l3 illustrative but in need of expansion if we are to fully describe all the returns and impacts that are generated in the relationships between impact investors and their investees. To begin, it's important to differentiate among investors, as Iwill argue that there is an investor impact that adds yet another dimension of additionality in anytransaction, depending on the unique interests of the investor. Brest and Born dene foundations or other investors who start with a philanthropic perspective to promote and stimulate positive social change as socially motivated investors, as distinct from socially neutral investors. And indeed, at the Kellogg Foundation we have found ourselves often in deals side by side with socially neu tral investors, realizing or hoping to achieve marketrate returns. The authors are right to be skeptical that much impact invest ing strictly dened can achieve both marketrate nancial returns and social impact returns, but the likelihood of this happening in creases if we take into account another potential return: what we at the Kellogg Foundation call the learning return. (There is also a corresponding learning return for socially neutral investors, who by specializingin an industry gain increasing expertise to optimize future nancial returns.) For foundations, which for the most part have made only charitable grants, becoming impact investors in commercial enterprises brings new and different information and insights into social problem solving that would not otherwise be available to them through charitable grantmaking alone. Brest and Born appreciate that value is added from the rela tionship between investor and investee (called nonmonetary im pact), but they see this as occurring in only one direction, from the investor to the investee. There is, however, the potential for a \"more than money\" return from the investee to the investor that can make socially motivated investors smarter and more effective in their core philanthropic endeavors, increasing social impact in both conventional charitable grantmaking and impact investing. Here are some examples from the Kellogg Foundation. With decades of work and experience in food systems and with long term eldbuilding efforts in farmtoschool, community food, and school food transformations, the foundation saw an opportunity to invest in ayoung company, Revolution Foods, that was dedicated to selling healthy, affordable, delicious food for schoolchildren. It has brought us wholly new perspectives on issues of public policy, school and community food systems, and family and child behaviors that we can use to inform our grantmaking and institutional efforts on the very same issues. Investing in a bank, Southern Bancorp, that does business in the Mississippi Delta region, one of the founda tion's priority places, creates a partnership and provides a unique perspective onthe challenges of economic andworkforce develop ment with which our program staff continually grapple. With our investment in Wireless Generation, our intense learning return on how to bring technology and big data to realtime assessments, coupled with customized instruction for K3 early grade literacy, was matched by our 26 percent return with an early buyout. And today, as more funders seek to promote and invest in prevention and wellness as opposed to disease treatment, our investment in SeeChange Health tells the same story in the health arena. Traditionally, foundations have supported pilot and model programs in the hope that they will be replicated and then funded more broadly by government. Now we see that when our eld building efforts are successful, they can create new demands and ultimately new markets for entrepreneurs to take advantage of. In this way, foundations can enlist private sector forces in scal ing up what works. Impact investments are not standalone transactions, but pivot points on the continuum of grants to commercial investments that enable socially motivated investors to continue learning and to stimulate continued advancement of their missions across sectors. For any given transaction, there might not be investment impact additionality as strictly dened by Brest and Born, but there can be substantial investor impacts that will increase mission efcacy over the long term. ALVARO RODRIGUEZ ARREGUI is man- aging partner at IGNIA. He is the former chairman and current vice- chairman of Compartamos Banco. MICHAEL CHU is managing director of IGNlA and senior lecturer of business administration at Harvard Business School. Hewas previously president and CEO ofACClON International. Alvaro Rodriguez Arregui 8: Michael Chu he article by Paul Brest and Kelly Born perpetuates the idea that nancial returns and social impact are a zerosum game and that you cannot maximize both. This perspective has done a tremendous disservice to the impact investing eld. If the world had adopted it two de cades ago, poverty would not have been reduced by 50 percent. Not all human and environmental challenges can be tackled with commercial approaches, and manyterms denote the noncom mercial initiatives that address these challenges, including philan thropy, nonprot, public sector, and corporate social responsibility. A new term is justiedonly if it is not old wine in anewbottle. That is why at IGNIA we believe that impact investing should be reserved for a commercial approach, lest we confuse more than we clarify. The authors ask, When can investors expect both to receive riskadjusted marketrate returns on their investments and have real social impact? The answer is, When an intervention of high social value is mounted on a sturdy business platform. We proved that this was possible with commercial micronance. At IGNIA, we seek to extend this approach to affordable housing, digital access for the daily needs of people at the base of the pyramid (BOP), ac cess to health care, highnutrition products, and other basic needs. If we succeed and achieve extraordinary nancial returns, this will attract a ock of market entrants. With their entrywe will create an industry, and only then can we guarantee achieving a lasting and large enough impact to move the needle. In this way nan cial returns can be the main driver for social impact. Accordingly, there is no question that intentionality is a key element of impact investing and the intention should create an industry. How else can we stand a chance of tackling the enormous challenges we face? Brest and Born's perspectivethat in order to achieve impact you need capital willing to accept concessionary returnsis based on the view that reaching clients depends on a single dimension: price. But the value proposition to a client is much more complex than price. For example, Mexico provides free public health care, but after factoring in travel time, waiting time, multiple visits to the doctor, and quality of care, people at the BOP would consider that the total transaction cost is actually large. Seeking a better value, people at the BOP are often willing to dig deep into their shallow pockets to opt for a commercial healthcare alternative. The market economy has taught us this lesson, but in the social impact world we refuse to accept it. Brest and Born's View that \"an ordinary market investor, who seeks marketrate returns, would not provide the capital on as favorable terms\" perpetuates two false views: rst, that invest ments with impact cannot achieve extraordinary returns, and second, that the impact world sets the bar too low and continues to fund mediocre business plans for which no source other than concessionary funding is possible. If the rst view were accurate, few of the great innovations that have improved the quality of life of humankind over the past 100 years would have ourished. The second leads to the view that impact investing is an industry de voted to funding the wellintentioned \"walking dead\" (to use the venture capital industry's term). By focusing on nancial returns, Brest and Born miss the point that what distinguishes impact investors from traditional inves tors is that they have a higher tolerance for risk. Brest and Born also call for more attention to measuring out comes. But we have spent too much time and too many resources discussing impact measurement and trying to measure outcomes. Is an individual who needs eyeglasses better off if she has access to them? If you are wearing a pair while reading this article, you know the answer. There are myriad basic products and services such as eyeglasses to which the majority of the world's population does not have access and which, if they did, would allow them to live signicantly improved lives. So let's move on and not over burden those initiatives focused on underserved communities with academic questions. They already face plenty of challenges trying to deliver what they promise. There is no question that there is a role for philanthropic capital in impact investing. Philanthropy, as in the biotech and the cleantech industries, can provide the very early stage R&D capital that carries such high risk that it would never attract any returnseeking investor. In this wellworn model, philanthropy, often through universities, helps give birth to new ideas and enables their development into working concepts, at which point the risk level is in the range where venture capital can enter and bet on building an effective business model. Instead of playing this role in impact investing and supporting disruptive business concepts on their hard road to viability (or not), FallZOB -ST/\\MORD SOCl/\\l lNNOVAIlOK REVIEW 29 Concept Definition Rate of return Financial rate of return: The rate of return is the income generated by an asset expressed as a percentage of the value of that asset. The rate of return may be measured ex ante (the return expected when the investment was made) or ex post (the return that was actually earned). Social rate of return: Includes benefits of investment in a social program calculated through an economic cost benefit analysis which includes avoided costs of government over the medium to long term. Example: When applied to education, the social internal rate of return refers to the costs and benefits to society of investment in education. This includes the opportunity cost of having people not participating in the production of output and the full cost of the provision of education rather than only the cost borne by the individual. The social benefit includes the increased productivity associated with the investment in education and a host of possible benefits, such as lower crime, better health, reduced population growth, more social cohesion, or more informed and effective citizens, which are calculated in economic terms as avoided costs. Source Financial rate of return: https:[[ statsoecdor lossar detail. asp?lD=5338 Social rate of return: https statsoecdor lossar detail. asp?|D=5426 Risk General: A measure of the possibility that the future may be surprisingly different from what is expected. Downside risk (in the financial context) refers to the potential for loss and upside risk refers to the potential for gain. Different types of examples in impact investment include political risk: the risk related to instability in a country; Currency risk: currency volatility and currencies that lack hedging mechanisms; Exit risk: difficulty of exiting an investment; operational risk; legal risk, client risk, environmental risk, reputational riskforagencies; credit risk. General: httg:[[www.nonprofitrisk. or librar lossar .shtml Examples: http:([www.investopedia. comiarticleslinvestingz0930l51 impact-investing-funds-what-are- risksasp Risk transfer Allocating each delivery/operating risk of an asset or service to the party best able to manage it. Risks can be transferred through contracts and the payment mechanism, e.g. cost escalation risk can be transferred through using a fixed price contract. KPMG Risk sharing A method of funding loss using external funds (such as insurance) or risk sharing with another organization. Examples of risk sharing include mutual aid agreements with other non profits, and sharing responsibility for a risk with others through a contractual agreement. Service provider In a SIB/DIE, the entity that is contracted to deliver a service/ product to target beneficiaries with specific terms and conditions for the intended outcome (or output) and form of delivery. http://www.nonprofitrisk.org/library/ 9mm http://wwwcodev.org/sites/default[ files/investind-in-social-outcomes- development-impact-bondspdf 10 KPMG is not responsrble for the reliability of content hosted on thirdparty links and information was current as of the publication of this document. Understanding impact investing 2018 KPMG International Cooperative ("KPMG International"), a Swrss entity. Member firms of the KPMG network of independcnt firms are affiliated with KPMG lnterna tional. KPMG International provides no client services No memberfirm has any authority to obligate or bind KPMG International or any other member firm vis-a-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rig ts reserved. NDPPS 76821l 2018 KPMG International Cooperative (\"KPMG International\"), a SWiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG interna tional. KPMG International provides no client services No member firm has any authority to obligate or bind KPMG International or any other member firm viseaevis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 7682M Concept Definition Source Social Impact Social Impact Bonds (8|le are performance based, pay for httpsz/lwww.rockefellerfoundation. Bond (SIB) success investment instruments intended to assist national, or our-work initiatives social- state and local governments fund social programs through impactbondsl a combination of government initiation, private investment, and non-profit implementation. Investors are only repaid if and when improved social outcomes are achieved. SlBs have the potential to open new funding sources for prevention- oriented or social service enhancement programs that deliver measurable social benefits, saving taxpayer dollars in the process. Socially Other terms for Social Impact Bonds. See SIB. relevant bondl Social benefit hond/ Pay for success bonds Sustainable Sustainable development is development that meets the http://www.iisd.org/topic/sustainable- development needs of the present generation without compromising development the ability of future generations to meet their own needs. It contains within it two key concepts: the concept of needs, in particular the essential needs of the world's poor, to which overriding priority should be given; and the idea of limita

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance