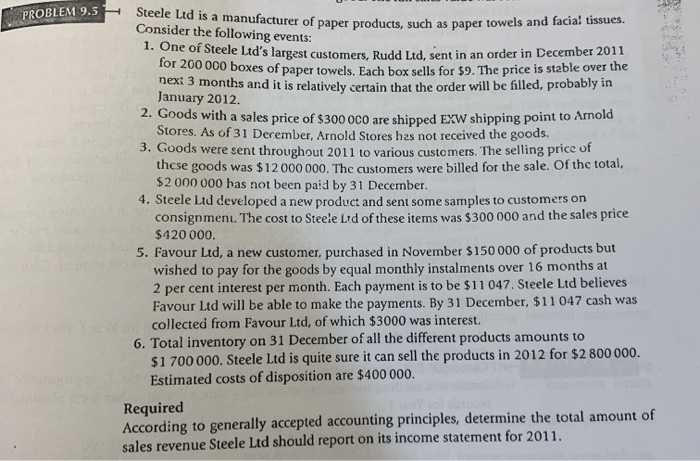

Steele Ltd is a manufacturer of paper products, such as paper towels and facia! tissues. PROBLEM 9.5 Consider the following events: 1. One of Steele Ltd's largest customers, Rudd Ltd, sent in an order in December 2011 for 200 000 boxes of paper towels. Each box sells for $9. The price is stable over the next 3 months and it is relatively certain that the order will be filled, probably in January 2012. 2. Goods with a sales price of $300 0CO are shipped EXW shipping point to Arnold Stores. As of 31 December, Arnold Stores has not received the goods. 3.Goods were sent throughout 2011 to various custemers. The selling price of these goods was $12 000 000. The customers were billed for the sale. Of the total, $2 000 000 has not been paid by 31 December. 4. Steele Ltd developed a new produc: and sent some samples to customers on consignment. The cost to Steele Ltd of these items was $300 000 and the sales price $420 000. 5. Favour Ltd, a new customer, purchased in November $150 000 of products but wished to pay for the goods by equal monthly instalments over 16 months at 2 per cent interest per month. Each payment is to be $11 047. Steele Ltd believes Favour Ltd will be able to make the payments. By 31 December, $11 047 cash was collected from Favour Ltd, of which $3000 was interest. 6. Total inventory on 31 December of all the different products amounts to $1700 000. Steele Ltd is quite sure it can sell the products in 2012 for $2 800 000. Estimated costs of disposition are $400 000. Required According to generally accepted accounting principles, determine the total amount of sales revenue Steele Ltd should report on its income statement for 2011. Steele Ltd is a manufacturer of paper products, such as paper towels and facia! tissues. PROBLEM 9.5 Consider the following events: 1. One of Steele Ltd's largest customers, Rudd Ltd, sent in an order in December 2011 for 200 000 boxes of paper towels. Each box sells for $9. The price is stable over the next 3 months and it is relatively certain that the order will be filled, probably in January 2012. 2. Goods with a sales price of $300 0CO are shipped EXW shipping point to Arnold Stores. As of 31 December, Arnold Stores has not received the goods. 3.Goods were sent throughout 2011 to various custemers. The selling price of these goods was $12 000 000. The customers were billed for the sale. Of the total, $2 000 000 has not been paid by 31 December. 4. Steele Ltd developed a new produc: and sent some samples to customers on consignment. The cost to Steele Ltd of these items was $300 000 and the sales price $420 000. 5. Favour Ltd, a new customer, purchased in November $150 000 of products but wished to pay for the goods by equal monthly instalments over 16 months at 2 per cent interest per month. Each payment is to be $11 047. Steele Ltd believes Favour Ltd will be able to make the payments. By 31 December, $11 047 cash was collected from Favour Ltd, of which $3000 was interest. 6. Total inventory on 31 December of all the different products amounts to $1700 000. Steele Ltd is quite sure it can sell the products in 2012 for $2 800 000. Estimated costs of disposition are $400 000. Required According to generally accepted accounting principles, determine the total amount of sales revenue Steele Ltd should report on its income statement for 2011